U.S. large caps: Capital investment and productivity appear set to drive growth in 2026

Portfolio Manager Jeremiah Buckley shares his 2026 outlook for U.S. large-cap equities, highlighting a path for continued economic and earnings growth through artificial intelligence (AI) infrastructure spending and productivity gains.

7 Minuten Lesezeit

Zentrale Erkenntnisse:

- The outlook for U.S. large-cap equities remains positive, supported by a broad capital investment cycle, productivity gains, and expectations for double-digit earnings growth.

- While market valuations are elevated, earnings growth is strong and the industry mix within major indices has shifted toward faster-growing sectors that typically command higher multiples.

- We believe companies with scale, strong balance sheets, and the ability to invest in productivity-enhancing technologies are positioned to lead as AI adoption broadens across the economy.

As we look toward 2026, we maintain an optimistic outlook for U.S. large-cap equities. This view is supported by a powerful capital investment cycle, a resilient consumer, and broadening productivity gains that have strengthened corporate earnings.

While this environment presents opportunities, navigating elevated concentration and valuations requires a selective, adaptive approach. Our focus remains on companies with scale, strong balance sheets, and the ability to invest in productivity-enhancing technologies.

Capital investment has driven productivity gains

The U.S. economy is benefiting from a historic capital expenditure boom. AI is a primary driver, with technology infrastructure spending now accounting for a meaningful portion of U.S. real GDP growth. Robust demand for cloud services and data center capacity shows no signs of slowing.

However, the capital expenditure story extends beyond technology. Recent tax policies allowing immediate depreciation of investments are fueling a broader spending cycle across the market. This widespread capital investment drives productivity gains, which could support future economic growth.

The shift toward greater efficiency has become increasingly evident. More companies are providing examples of AI applications delivering tangible productivity gains. The last two earnings seasons showcased impressive operating leverage, with companies posting strong revenue growth while controlling expenses. This suggests businesses are already seeing returns on their investments, boosting margins and earnings despite cost pressures.

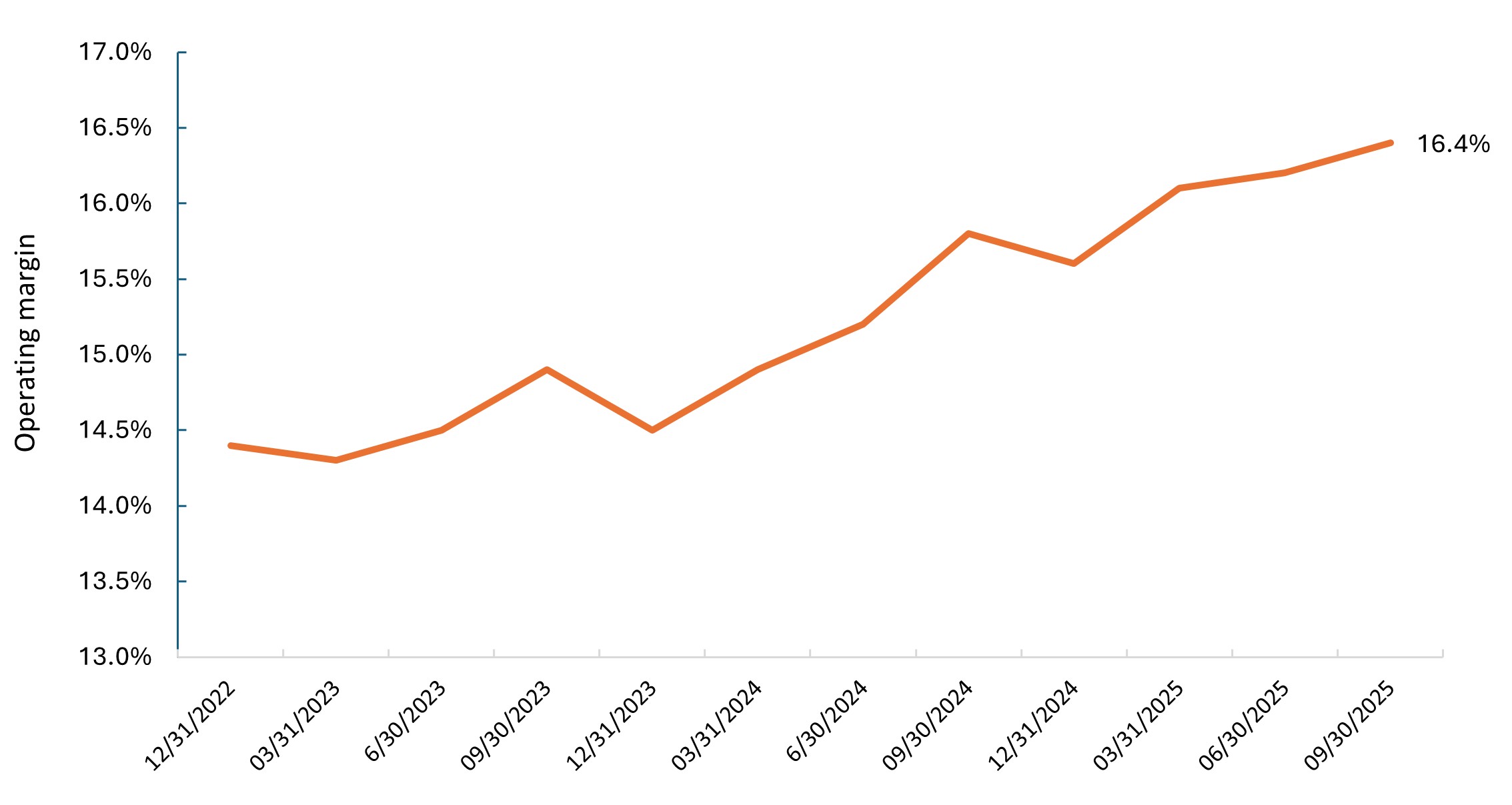

Exhibit 1: S&P 500® Index operating margin (ex-energy)

Outside the volatile Energy sector, the market has benefited from consistent margin improvements over the last two years. Gains have been led by sectors like Communication Services, Information Technology, and Financials where companies can best leverage technology to improve operations.

Source: Bloomberg Intelligence, as of 14 November 2025.

Consumer spending remains resilient

We continue to be optimistic about consumer spending even as labor force growth has softened. Wage growth of around 4.5% continues to outpace pre-pandemic levels, supporting spending. Consumer balance sheets are strong, with the ratio of debt service to disposable income within normal historical range and credit delinquencies remaining low.

However, we recognize consumer spending is always shifting and there will be segments of the economy that contract while others expand. When analyzing credit card data, overall spending is strong, but some segments are flat, such as those more impacted by inflation and moderating job growth. Today, we see that consumers tend to favor experiences over goods, and that there is strong demand for travel.

We see the potential for an additional boost in consumer spending in 2026 from recent tax reforms, which should lead to better refunds during tax season. While spending is strongest among upper-income households benefiting from housing and market gains, the overall picture remains positive.

Market concentration reflects earnings leadership

Market concentration in the U.S. is at a level we haven’t seen in recent history. But when we look at the earnings growth and sustainability of the companies with the largest market capitalization, it’s not surprising because they are leading the technology transformation.

Given AI infrastructure’s importance to the economy, we’re monitoring whether companies achieve appropriate returns, execute on their backlogs, and generate revenue that supports continued investment. Should the AI investment cycle plateau and earnings trajectories change, investors must be prepared to adjust.

While multiples have expanded in the AI infrastructure theme, demand has continued to surprise to the upside, so earnings growth supports the multiples for now, in our view. That said, being adaptive is the right positioning today. Considerable time must be spent assessing balance sheets, cash flow statements, and business sustainability metrics to ensure fundamentals justify market weights.

Putting valuations in context

We acknowledge that the market’s overall multiple is elevated. However, context is helpful. First, the market’s composition has fundamentally shifted. The fastest-growing, highest return on invested capital (ROIC) sectors within the major indices have significantly increased in weight.

Furthermore, strong earnings support current multiple levels. The market delivered more than 12% earnings growth in the second quarter, with similar expectations through 2026. Unlike the 2000 tech bubble, today’s valuation expansion has been matched by a widening profitability premium. We can still find plenty examples of high-quality companies in secular growth industries trading at or below historical multiples.

Where we see opportunity

Within the AI theme, our focus is on both enablers and adopters. Enablers include semiconductor, cloud, and software companies, as well as enterprise platforms developing AI and automation solutions. Adopters are companies across all sectors that have committed to this new technology and are investing aggressively.

Encouragingly, earnings strength has extended beyond AI and technology. Commercial aerospace, capital markets, medical technology, and travel have delivered impressive results. This breadth suggests corporate health is more widespread than some narratives suggest.

Within financial services, investment banking revenues have grown more than 50% based on increased mergers and acquisitions activity and initial public offerings. We think capital markets activity will be strong for the next couple of years as funding continues for the AI capital expenditure investment cycle, potentially benefiting investment banks, ratings agencies, and exchanges. Also, digital payment companies have continued to grow earnings at a 15% annual clip as consumer spending remains strong.

We’re also finding attractive opportunities in industrials focused on automation and electrification. In addition, the need for power and cooling technology for data centers presents compelling opportunities.

Innovation and scale support market leadership

We believe the current environment underscores the advantages of scale, innovation, and access to capital that define leading U.S. large-cap companies. Transformation driven by AI is expensive, requiring strong balance sheets and market leadership to fund the necessary investments and harness the data for effective applications. We believe companies lacking scale or investment capabilities risk falling behind and losing market share.

Overall, we believe environment for U.S. large-cap equities remains positive heading into 2026. Innovation leadership and entrepreneurial culture extend beyond technology into important areas like healthcare devices and diagnostics as well as biotechnology. The U.S. also has a flexible labor force that can be retrained for more productive roles and opportunities as some jobs are replaced by AI. The combination of capital investment, productivity gains, a resilient consumer, and broadening earnings growth provides a durable foundation for continued market leadership.

WICHTIGE INFORMATIONEN

Aktiv verwaltete Portfolios erzielen möglicherweise nicht die beabsichtigten Ergebnisse. Keine Anlagestrategie kann einen Gewinn garantieren oder das Verlustrisiko eliminieren.

Unternehmen, die sich auf künstliche Intelligenz („KI“) konzentrieren, einschließlich derjenigen, die KI-Technologien entwickeln oder nutzen, könnten mit einer schnellen Produktveralterung, intensivem Wettbewerb und verstärkter behördlicher Kontrolle konfrontiert sein. Diese Unternehmen sind häufig stark auf geistiges Eigentum angewiesen, investieren erheblich in Forschung und Entwicklung und sind auf die Aufrechterhaltung und Steigerung der Verbrauchernachfrage angewiesen. Ihre Wertpapiere können volatiler sein als die von Unternehmen, die etabliertere Technologien anbieten, und sie können von Risiken betroffen sein, die mit der Nutzung von KI im Geschäftsbetrieb verbunden sind, darunter rechtliche Haftung oder Reputationsschäden.

Beteiligungspapiere unterliegen Risiken, einschließlich des Marktrisikos. Die Renditen schwanken in Abhängigkeit von Emittenten sowie von politischen und wirtschaftlichen Entwicklungen.

Die Finanzbranche kann erheblich von umfangreichen staatlichen Regulierungen betroffen sein, die aufgrund der zunehmend verschwimmenden Grenzen zwischen den Dienstleistungssegmenten einem relativ schnellen Wandel unterworfen sind und erheblich von der Verfügbarkeit und den Kosten von Kapitalmitteln, Änderungen der Zinssätze, der Ausfallrate von Unternehmens- und Verbraucherschulden und dem Preiswettbewerb beeinflusst werden.

Wachstumsaktien sind mit einem höheren Risiko von Verlusten oder Kursschwankungen verbunden und können ihr wahrgenommenes Wachstumspotenzial möglicherweise nicht realisieren.

Der Gesundheitssektor unterliegt der staatlichen Regulierung und den Erstattungssätzen sowie der staatlichen Zulassung von Produkten und Dienstleistungen. Das kann sich erheblich auf Preise und Verfügbarkeit auswirken, und durch schnelle Veralterung von Medikamenten und den Ablauf von Patenten erheblich beeinflusst werden.

Das Kurs-Gewinn-Verhältnis (KGV) misst den Aktienkurs im Vergleich zum Gewinn je Aktie für einen oder mehrere Portfoliotitel.

Die Kapitalrendite (Return On Invested Capital, ROIC) ist ein Maß dafür, wie effektiv ein Unternehmen das in seine Geschäftstätigkeit investierte Geld einsetzt.

DerS&P 500® Index spiegelt die Performance der US Large-cap-Aktien wider und entspricht der Performance des US-Aktienmarktes allgemein.

Die Volatilität ist das Tempo und Ausmaß von Auf- und Abbewegungen der Preise von Portfolios, Wertpapieren oder Indizes. Wenn der Kurs mit großen Schwankungen auf und ab schwankt, weist er eine hohe Volatilität auf. Wenn sich der Kurs langsamer und in geringerem Maße bewegt, weist er eine geringere Volatilität auf. Je höher die Volatilität, desto höher das Risiko der Anlage.

7 Minuten Lesezeit

Zentrale Erkenntnisse:

- The outlook for U.S. large-cap equities remains positive, supported by a broad capital investment cycle, productivity gains, and expectations for double-digit earnings growth.

- While market valuations are elevated, earnings growth is strong and the industry mix within major indices has shifted toward faster-growing sectors that typically command higher multiples.

- We believe companies with scale, strong balance sheets, and the ability to invest in productivity-enhancing technologies are positioned to lead as AI adoption broadens across the economy.

Markteinblicke

As we look toward 2026, we maintain an optimistic outlook for U.S. large-cap equities. This view is supported by a powerful capital investment cycle, a resilient consumer, and broadening productivity gains that have strengthened corporate earnings.

While this environment presents opportunities, navigating elevated concentration and valuations requires a selective, adaptive approach. Our focus remains on companies with scale, strong balance sheets, and the ability to invest in productivity-enhancing technologies.

Capital investment has driven productivity gains

The U.S. economy is benefiting from a historic capital expenditure boom. AI is a primary driver, with technology infrastructure spending now accounting for a meaningful portion of U.S. real GDP growth. Robust demand for cloud services and data center capacity shows no signs of slowing.

However, the capital expenditure story extends beyond technology. Recent tax policies allowing immediate depreciation of investments are fueling a broader spending cycle across the market. This widespread capital investment drives productivity gains, which could support future economic growth.

The shift toward greater efficiency has become increasingly evident. More companies are providing examples of AI applications delivering tangible productivity gains. The last two earnings seasons showcased impressive operating leverage, with companies posting strong revenue growth while controlling expenses. This suggests businesses are already seeing returns on their investments, boosting margins and earnings despite cost pressures.

Exhibit 1: S&P 500® Index operating margin (ex-energy)

Outside the volatile Energy sector, the market has benefited from consistent margin improvements over the last two years. Gains have been led by sectors like Communication Services, Information Technology, and Financials where companies can best leverage technology to improve operations.

Source: Bloomberg Intelligence, as of 14 November 2025.

Consumer spending remains resilient

We continue to be optimistic about consumer spending even as labor force growth has softened. Wage growth of around 4.5% continues to outpace pre-pandemic levels, supporting spending. Consumer balance sheets are strong, with the ratio of debt service to disposable income within normal historical range and credit delinquencies remaining low.

However, we recognize consumer spending is always shifting and there will be segments of the economy that contract while others expand. When analyzing credit card data, overall spending is strong, but some segments are flat, such as those more impacted by inflation and moderating job growth. Today, we see that consumers tend to favor experiences over goods, and that there is strong demand for travel.

We see the potential for an additional boost in consumer spending in 2026 from recent tax reforms, which should lead to better refunds during tax season. While spending is strongest among upper-income households benefiting from housing and market gains, the overall picture remains positive.

Market concentration reflects earnings leadership

Market concentration in the U.S. is at a level we haven’t seen in recent history. But when we look at the earnings growth and sustainability of the companies with the largest market capitalization, it’s not surprising because they are leading the technology transformation.

Given AI infrastructure’s importance to the economy, we’re monitoring whether companies achieve appropriate returns, execute on their backlogs, and generate revenue that supports continued investment. Should the AI investment cycle plateau and earnings trajectories change, investors must be prepared to adjust.

While multiples have expanded in the AI infrastructure theme, demand has continued to surprise to the upside, so earnings growth supports the multiples for now, in our view. That said, being adaptive is the right positioning today. Considerable time must be spent assessing balance sheets, cash flow statements, and business sustainability metrics to ensure fundamentals justify market weights.

Putting valuations in context

We acknowledge that the market’s overall multiple is elevated. However, context is helpful. First, the market’s composition has fundamentally shifted. The fastest-growing, highest return on invested capital (ROIC) sectors within the major indices have significantly increased in weight.

Furthermore, strong earnings support current multiple levels. The market delivered more than 12% earnings growth in the second quarter, with similar expectations through 2026. Unlike the 2000 tech bubble, today’s valuation expansion has been matched by a widening profitability premium. We can still find plenty examples of high-quality companies in secular growth industries trading at or below historical multiples.

Where we see opportunity

Within the AI theme, our focus is on both enablers and adopters. Enablers include semiconductor, cloud, and software companies, as well as enterprise platforms developing AI and automation solutions. Adopters are companies across all sectors that have committed to this new technology and are investing aggressively.

Encouragingly, earnings strength has extended beyond AI and technology. Commercial aerospace, capital markets, medical technology, and travel have delivered impressive results. This breadth suggests corporate health is more widespread than some narratives suggest.

Within financial services, investment banking revenues have grown more than 50% based on increased mergers and acquisitions activity and initial public offerings. We think capital markets activity will be strong for the next couple of years as funding continues for the AI capital expenditure investment cycle, potentially benefiting investment banks, ratings agencies, and exchanges. Also, digital payment companies have continued to grow earnings at a 15% annual clip as consumer spending remains strong.

We’re also finding attractive opportunities in industrials focused on automation and electrification. In addition, the need for power and cooling technology for data centers presents compelling opportunities.

Innovation and scale support market leadership

We believe the current environment underscores the advantages of scale, innovation, and access to capital that define leading U.S. large-cap companies. Transformation driven by AI is expensive, requiring strong balance sheets and market leadership to fund the necessary investments and harness the data for effective applications. We believe companies lacking scale or investment capabilities risk falling behind and losing market share.

Overall, we believe environment for U.S. large-cap equities remains positive heading into 2026. Innovation leadership and entrepreneurial culture extend beyond technology into important areas like healthcare devices and diagnostics as well as biotechnology. The U.S. also has a flexible labor force that can be retrained for more productive roles and opportunities as some jobs are replaced by AI. The combination of capital investment, productivity gains, a resilient consumer, and broadening earnings growth provides a durable foundation for continued market leadership.

WICHTIGE INFORMATIONEN

Aktiv verwaltete Portfolios erzielen möglicherweise nicht die beabsichtigten Ergebnisse. Keine Anlagestrategie kann einen Gewinn garantieren oder das Verlustrisiko eliminieren.

Unternehmen, die sich auf künstliche Intelligenz („KI“) konzentrieren, einschließlich derjenigen, die KI-Technologien entwickeln oder nutzen, könnten mit einer schnellen Produktveralterung, intensivem Wettbewerb und verstärkter behördlicher Kontrolle konfrontiert sein. Diese Unternehmen sind häufig stark auf geistiges Eigentum angewiesen, investieren erheblich in Forschung und Entwicklung und sind auf die Aufrechterhaltung und Steigerung der Verbrauchernachfrage angewiesen. Ihre Wertpapiere können volatiler sein als die von Unternehmen, die etabliertere Technologien anbieten, und sie können von Risiken betroffen sein, die mit der Nutzung von KI im Geschäftsbetrieb verbunden sind, darunter rechtliche Haftung oder Reputationsschäden.

Beteiligungspapiere unterliegen Risiken, einschließlich des Marktrisikos. Die Renditen schwanken in Abhängigkeit von Emittenten sowie von politischen und wirtschaftlichen Entwicklungen.

Die Finanzbranche kann erheblich von umfangreichen staatlichen Regulierungen betroffen sein, die aufgrund der zunehmend verschwimmenden Grenzen zwischen den Dienstleistungssegmenten einem relativ schnellen Wandel unterworfen sind und erheblich von der Verfügbarkeit und den Kosten von Kapitalmitteln, Änderungen der Zinssätze, der Ausfallrate von Unternehmens- und Verbraucherschulden und dem Preiswettbewerb beeinflusst werden.

Wachstumsaktien sind mit einem höheren Risiko von Verlusten oder Kursschwankungen verbunden und können ihr wahrgenommenes Wachstumspotenzial möglicherweise nicht realisieren.

Der Gesundheitssektor unterliegt der staatlichen Regulierung und den Erstattungssätzen sowie der staatlichen Zulassung von Produkten und Dienstleistungen. Das kann sich erheblich auf Preise und Verfügbarkeit auswirken, und durch schnelle Veralterung von Medikamenten und den Ablauf von Patenten erheblich beeinflusst werden.

Das Kurs-Gewinn-Verhältnis (KGV) misst den Aktienkurs im Vergleich zum Gewinn je Aktie für einen oder mehrere Portfoliotitel.

Die Kapitalrendite (Return On Invested Capital, ROIC) ist ein Maß dafür, wie effektiv ein Unternehmen das in seine Geschäftstätigkeit investierte Geld einsetzt.

DerS&P 500® Index spiegelt die Performance der US Large-cap-Aktien wider und entspricht der Performance des US-Aktienmarktes allgemein.

Die Volatilität ist das Tempo und Ausmaß von Auf- und Abbewegungen der Preise von Portfolios, Wertpapieren oder Indizes. Wenn der Kurs mit großen Schwankungen auf und ab schwankt, weist er eine hohe Volatilität auf. Wenn sich der Kurs langsamer und in geringerem Maße bewegt, weist er eine geringere Volatilität auf. Je höher die Volatilität, desto höher das Risiko der Anlage.