Anatomy of a short squeeze: causes, outcomes and lessons

13 minute read

David Elms, Head of Diversified Alternatives, considers the lessons that short squeezes can offer about the inherent danger of carrying excessive leverage or short positions during periods of heightened risk and illiquidity.

Key takeaways:

- Short squeezes have been an infrequent but impactful feature in financial markets over the last two centuries, from the New York and Harlem Railroad Company in 1864 to the nickel short squeeze of 2021.

- The Volkswagen short squeeze in 2008 – the ‘mother of all short squeezes’ – resulted in considerable controversy, drawing attention to both systemic and unexpected market risks.

- Experiencing a dislocation, such as a short squeeze, is a fact of life when you run portfolios for long enough. It highlights the importance of appropriate position sizing, diversification and having an exit strategy when things do not go to plan.

He who sells what isn’t his’n, must buy it back or go to pris’n.”

Daniel Drew, American financier

The announcement by Elliot Investment Management on 6 June 2022 that it is seeking US$456 million in damages1 from the LME (London Metal Exchange) has brought attention back to the debacle in the nickel market, which saw the market effectively cease trading for two weeks in March2. It highlighted a rare but dramatic market dislocation known as a short squeeze. While uncommon, short squeezes manifest over time in different markets, and while the impacts vary, the causes are similar. This article will look at three instances of short squeezes over the last 15 years, all of which we have experienced – in one way or another – as a team, and the lessons we have drawn from each.

Short squeezes have been an impactful feature in financial markets over the last two centuries, often occurring at times of broader market dislocation. One of the better known and early short squeezes involved the speculator Daniel Drew, who was active on Wall Street from 1840 to 1875, and Cornelius Vanderbilt, a stalwart of Wall Street and early investor in railroads (among other business). Drew shorted stock in the New York and Harlem Railroad Company in 1864, hoping to gain from a price fall, however he faced off against motivated, well-funded buyers, who were able to force the price up significantly. Drew was reported to have lost US$500,000 at the time.

What is a short squeeze?

A short squeeze is defined as a sudden, dislocated increase in the price of a commodity or security, resulting from an excess of short selling that needs to be unwound.

- Highly sensitive/leveraged short sellers who need to buy back stock as it rises

- An imbalance in liquidity at the time that the short position is being covered

- A catalyst that triggers the rise in price.

While losing money on both longs and shorts is painful, what makes short positions additionally risky is the fact that – other than in highly unusual situations – losses on longs are limited by the value of a share falling to zero, whereas losses on shorts are unlimited. If a long position underperforms, the problem shrinks, as the price falls and the position reduces in size. On the short side, as the price rises, the position gets larger and the problem also grows, dangerously so if the price rise is big or fast, as it is in a short squeeze. This, along with the technical complications of borrowing securities and managing margin calls, makes short selling a complicated undertaking, far from being just ‘longs with a negative holding’.

Anatomy of three short squeezes (and lessons learnt)

Over the past 15 years, the Diversified Alternatives Team has experienced multiple shock events in stock and commodity markets, including three well-documented short squeezes. We will look at each of these and the impact and learnings from these unusual but significant market events.

Short squeeze 1: Porsche Volkswagen:

‘The mother of all short squeezes’

Exhibit 1: When short interest exceeds available stockThe stock more than quadrupled in price in just four days

Source: Bloomberg. 1 September 2008 to 1 December 2009 in euros.

Past performance does not predict future returns.

Background

The history of German automakers Porsche and Volkswagen had been interlocked for many years, with Porsche owning a minority stake in Volkswagen. From there, Porsche accumulated additional stock in what was then a highly indebted Volkswagen over the course of 2008, with short sellers on the other side assuming that the rise in prices was not sustainable and that Volkswagen stock should trade lower.

At that point it was assumed that the global financial crisis (GFC), playing out at the time, would flow into a collapse in demand for automobiles. The catalyst for the short squeeze and imbalance occurred in October 2008, when Porsche announced on Sunday, October 26, 20083 that it had accumulated an economic interest of approximately 74% of the stock in Volkswagen. With a fixed shareholding of 20%, due to the ‘Volkswagen Act’ from the German state of Lower Saxony, this meant there was only a free float of 6% of stock available versus 12% short interest held by short sellers.

The announcement from Porsche resulted in short sellers seeking to buy back stock. However, with an imbalance between the free float (6%) and short interest (12%), there was not enough stock available to close short positions. The ensuing short squeeze saw the price of Volkswagen stock rise by 450%, from around €200 to just over €900 between 24 October and 28 October – for a (very) brief period making Volkswagen the most valuable stock in the world.

Once short sellers had effectively covered their positions, the stock collapsed over the following month, falling back below €300. The chaos caused by this short squeeze saw many hedge funds either closed or severely impacted. It contributed to personal tragedy as well, with German industrialist Adolf Merckle taking his life in early 2009 amid the fallout from the GFC, a year after suffering substantial losses on the short side of Volkswagen.

The Volkswagen short squeeze resulted in considerable controversy, with legal action by impacted short sellers against Porsche ongoing at the time of writing, nearly 14 years after the event. The controversy narrowly centred around whether Porsche’s actions constituted market manipulation. More widely, it raised questions about German market oversight and governance, the attitude of the German regulators to short sellers, and German companies themselves. Failure to learn from the lessons of Volkswagen arguably contributed to the rise and fall – amidst allegations of fraud and embezzlement – of German payments processor Wirecard more than a decade later in our view.

Learnings

Post-event analysis identified potential improvements to our investment process at both the micro level (managing the risk of short positions in individual names) and at the macro level (ie. how to build a portfolio that was more robust to a highly challenging environment like the GFC, which made the Volkswagen short squeeze possible). Specifically on the micro side, the takeaways related to the quicker identification and response to potential squeezes, as well as management of position sizing, and the mechanics (eg. borrowing stock) of maintaining a short.

Short squeeze 2: GameStop

Exhibit 2: A uniquely perfect setup for a short squeeze?Shares in GameStop rose by over 2000% in three weeks

Source: Bloomberg, 3 November 2020 to 26 February 2021, in US dollars.

Past performance does not predict future returns.

Background

In January 2021, shares in US video game retailer GameStop (market ticker: GME) were hit by a short squeeze, with the stock price rising from approximately US$17 to over US$300 between 5 January and 27 January. Incredibly, the short interest in the stock equated to approximately 140% of the free float, creating a highly unstable situation with obvious risk if short sellers began to cover. While Volkswagen and GameStop shared the perception of being a compelling short on valuation grounds, GameStop had obvious concerns on the viability of its core retail business as the gaming market transitioned to streaming and COVID damaged many bricks-and-mortar retail businesses.

Michael Burry from ‘The Big Short’ film arguably paved the way for the GameStop frenzy when he purchased a stake in 2019, based on a view that the stock was ripe for a shareholder-friendly buyback. At the start of 2021, a campaign of targeted retail buying via the WallStreetBets Reddit forum, additional buying from various hedge fund managers, and short covering, saw the stock price go vertical. Following the short squeeze, short positions held by hedge funds subsequently lost billions of dollars of client capital.

“There really can’t be another GME.”

Michael Burry, hedge fund manager

Learnings

Trading through this period emphasised the importance of being able to dynamically adjust positioning, reinforcing the benefit of experience and agility, and supporting the argument for running a dedicated strategy that seeks to offset losses in dislocated environments. Later in 2021, as the GameStop situation calmed and become more stable, there was an opportunity for investors to take advantage of still inflated valuations, short selling GameStop as a part of a basket of ‘meme stocks’, benefitting as retail speculation abated and valuations normalised.

Short squeeze 3: nickel

Background

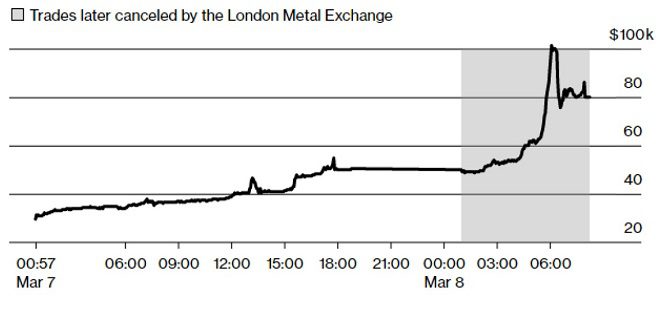

The most recent short squeeze was the nickel market in March 20225. Leading into the event various physical producers, including Tsingshan Holding Group6, were positioned with significant shorts, either on an uncovered basis or held against production. The catalyst for the short squeeze was the Russian invasion of Ukraine. With Russia a major producer of high-grade nickel, the prospect of supply disruptions saw prices start to climb rapidly, leading to the LME issuing margin calls in the order of US$7 billion, placing several companies and brokers in significant financial distress. The attempt to cover short positions during an invasion by a major nickel producing country saw prices surge from around US$30,000 per tonne to over US$100,000 on 8 March (Exhibit 3), with the number of short positions being covered overwhelming the number of market participants going short.

Exhibit 3: The price of nickel doubled in just a few minutes

Source: Bloomberg. Nickel price per (metric) tonne.

Past performance does not predict future returns.

While prior short squeezes had clear winners and losers, this short squeeze was fundamentally different. The LME first halted trading on 8 March after significant volatility in the first hour of trading, and then more significantly reversed all trades done prior to the exchange being closed on that date. The net effect was to delete losses for those that were short, and profits for participants that were long – a quite unprecedented intervention.

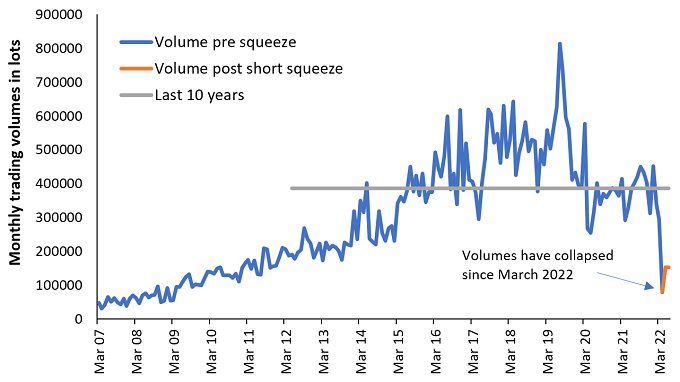

The LME’s actions led to a significant backlash from market participants, including the commencement of legal proceedings reviews by regulators, and the withdrawal of speculators and other market participants. The LME has been penalised in a very direct manner, with a collapse in market volumes and market participation, as Exhibit 4 shows.

Exhibit 4: LME nickel (three month) monthly market volumeLME market volumes collapsed after it intervened to reverse executed trades

Source: Bloomberg, 30 March 2007 to 30 June 2022. Monthly trading volume for LME Nickel; (3 month rolling forward).

Past performance does not predict future returns.

Learnings

How the LME deals with the fallout from its decision to cancel legitimate trades and cease trading in nickel for two weeks, without a mechanism for reasonable price discovery during significant geopolitical tension, is a monumental task. One risk for LME is that it opens up an opportunity for a rival to offer an alternative venue for trading. As for other market participants, we seek to transact in the most liquid and well-governed exchanges and markets to reduce and mitigate counterparty risk.

Conclusion

The recent short squeeze in the LME nickel market has reminded us of how fickle markets can be, the inherent danger of carrying excessive leverage or short positions during periods of heightened risk aversion and illiquidity, and the unemotional mechanism in clearing these imbalances.

It also highlighted something much more fundamental. Excess returns are only achieved by taking on some form of risk that other market participants wish to either transfer or mitigate. While an age-old issue, it nonetheless provides further evidence of the importance of appropriate position sizing, diversification, being nimble and having an exit strategy when things do not go to plan. Experiencing a dislocation, such as a short squeeze, is a fact of life if you are running portfolios for long enough. Experiencing losses (Volkswagen), participating in the opportunities short squeezes create (GameStop) and being on the right side of a short squeeze (nickel) all contribute to a pool of experience and knowledge that in our view helps to prepare the team, and better adapt our investment process, for whatever the future holds.

1. This short squeeze was covered in more detail by Matt Levine (Bloomberg): https://www.bloomberg.com/opinion/articles/2021-01-25/the-game-never-stops?sref=3pgYYCsj

2. A more detailed article on the nickel short squeeze from Jack Farchy, Alfred Cang, and Mark Burton (Bloomberg): https://www.bloomberg.com/news/articles/2022-03-14/inside-nickel-s-short-squeeze-how-price-surges-halted-lme-trading

3. https://www.reuters.com/world/china/chinese-tycoons-big-short-nickel-trips-up-tsingshans-miracle-growth-2022-03-13/

4. Porsche’s press release which led to the short squeeze: https://www.porsche-se.com/en/news/press-releases/details/news/detail/News/porsche-heads-for-domination-agreement-1

5. https://www.bloomberg.com/news/articles/2022-06-06/london-metal-exchange-sued-for-456-million-by-elliott#xj4y7vzkg

6. https://www.reuters.com/business/lme-suspends-nickel-trading-day-after-prices-see-record-run-2022-03-08/https://www.reuters.com/business/lme-suspends-nickel-trading-day-after-prices-see-record-run-2022-03-08/ Glossary Expand Short squeeze: Where unusual conditions trigger a rapid rise in price for a stock or other security that an unusual number of investors have shorted (taken a short position).

Short position (shorting): Fund managers use this technique to borrow then sell what they believe are overvalued assets, with the intention of buying them back for less when the price falls. The position profits if the security falls in value.

‘Long’ investing: The purchase of a stock with the purpose of benefitting from the potential growth in its value over time (plus dividends).

Borrowing securities: Securities lending is the practice of temporarily loaning assets to other investors, for a fee.

Margin call: A demand for additional capital or securities to bring a margin account up to the minimum maintenance margin when it runs low on funds, usually indicating a fall in the value of investments held.

Free float: Refers to the number of outstanding shares in a company, available to be publicly traded.

Buyback: A repurchase of outstanding shares by a company to reduce the amount in circulation, thereby increasing the value of remaining shares.

Market counterparty: In this example, a regulated market providing liquidity, or the ability to buy or sell assets, quote bid or offer prices. The LME has Qualifying Central Counter Party (QCCP) status.

Leverage: The use of borrowed money to invest, in the expectation that future profits will exceed the cost of borrowing.

Diversification: A way of spreading risk by mixing different types of assets/asset classes in a portfolio. It is based on the assumption that the prices of the different assets will behave differently in a given scenario. Assets with low correlation should provide the most diversification.

Hedge fund: An investment vehicle that traditionally focused on hedging risk by simultaneously buying and shorting assets in a long-short equity strategy. The term has evolved to cover actively managed investment strategies that may use higher risk or less common investment choices to try and deliver attractive returns.

Alternative Perspectives

Our views on the market themes to watch.

This information is issued by Janus Henderson Investors (Australia) Institutional Funds Management Limited (AFSL 444266, ABN 16 165 119 531). The information herein shall not in any way constitute advice or an invitation to invest. It is solely for information purposes and subject to change without notice. This information does not purport to be a comprehensive statement or description of any markets or securities referred to within. Any references to individual securities do not constitute a securities recommendation. Past performance is not indicative of future performance. The value of an investment and the income from it can fall as well as rise and you may not get back the amount originally invested.

Whilst Janus Henderson Investors (Australia) Institutional Funds Management Limited believe that the information is correct at the date of this document, no warranty or representation is given to this effect and no responsibility can be accepted by Janus Henderson Investors (Australia) Institutional Funds Management Limited to any end users for any action taken on the basis of this information. All opinions and estimates in this information are subject to change without notice and are the views of the author at the time of publication. Janus Henderson Investors (Australia) Institutional Funds Management Limited is not under any obligation to update this information to the extent that it is or becomes out of date or incorrect.