Quick view: The implications of rising inflation

7 minute read

Jay Sivapalan, Head of Australian Fixed Interest at Janus Henderson, discusses what caused February’s bond market volatility and how the team are actively navigating the challenging conditions.

Over February the Australian bond market1 was down approximately 3.5%, suffering its biggest negative monthly return since 1983. In combination with its negative return in January, this episode essentially wipes 80% of the bond market’s 2020 returns. Meanwhile, the 10 Year Australian Government bond yield has almost tripled since the lows experienced in 2020.

While only the rates market has been affected so far, in our view this could extend into risk assets (such as equities, high yield and investment grade credit) if central banks don’t intervene in a coordinated fashion to avoid a ‘taper tantrum’ style sell-off.

The ingredients for a bond market sell-off have been brewing for some time, and while hard to predict the turning point, as active managers we must be poised to re-position our portfolios and identify investment opportunities.

The three forces responsible

1. Rising inflation expectations:

- There has been a meaningful lift in inflation expectations over the past quarter resulting from positive sentiment around the post COVID-19 recovery and reflation.

- This has been largely driven by vaccination programs getting underway and central banks’ and governments’ commitment to supporting economies back out of the crisis.

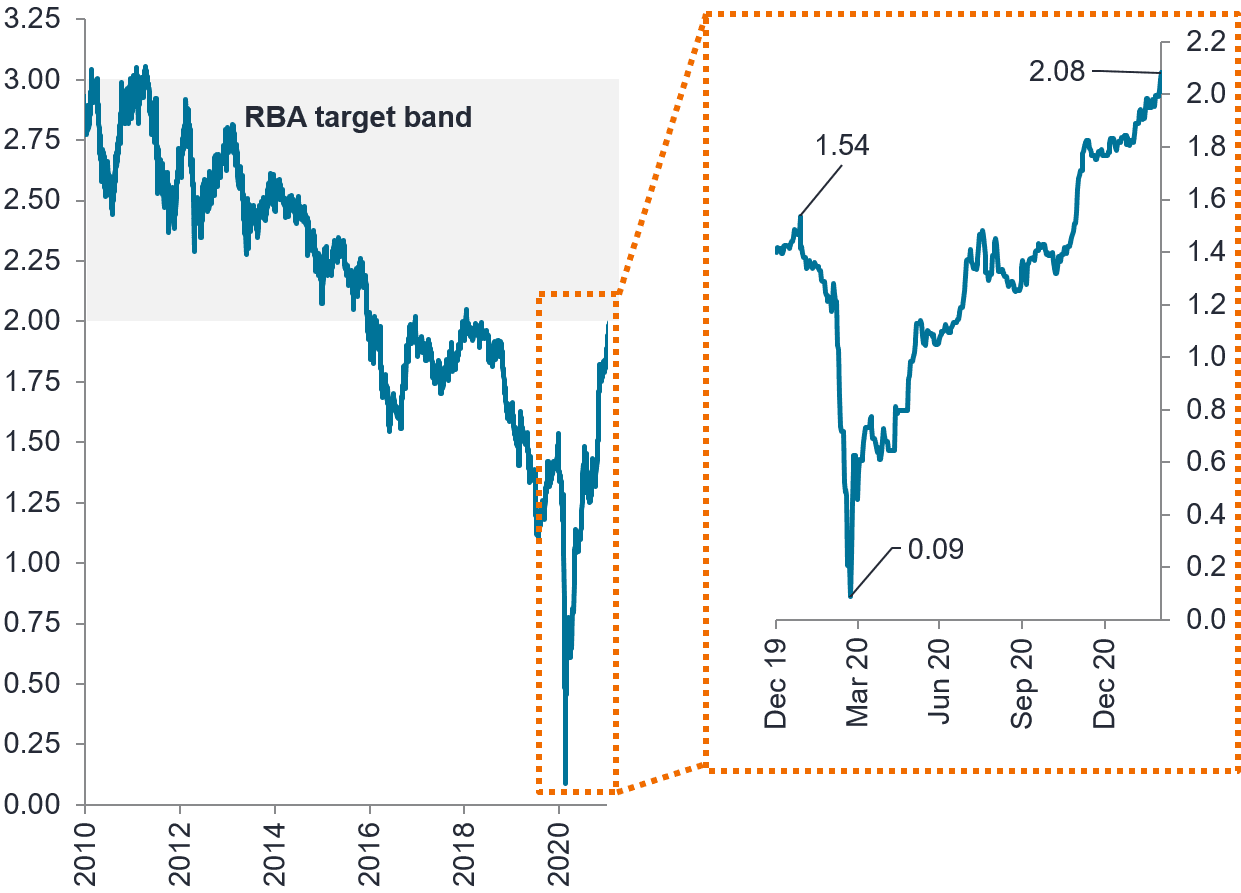

- The rapid turnaround is depicted by the 10-year breakeven inflation rate shown in Chart 1 below. Inflation expectations are many times higher than the low point experienced in March 2020 and have now crept up into the Reserve Bank of Australia’s (RBA) inflation rate target.

Chart 1: Australian 10-year breakeven inflation rate (%)

Source: Bloomberg, ABS, Australian 10-year breakeven inflation rate to 4 March 2021.

2. Rising cash rate expectations:

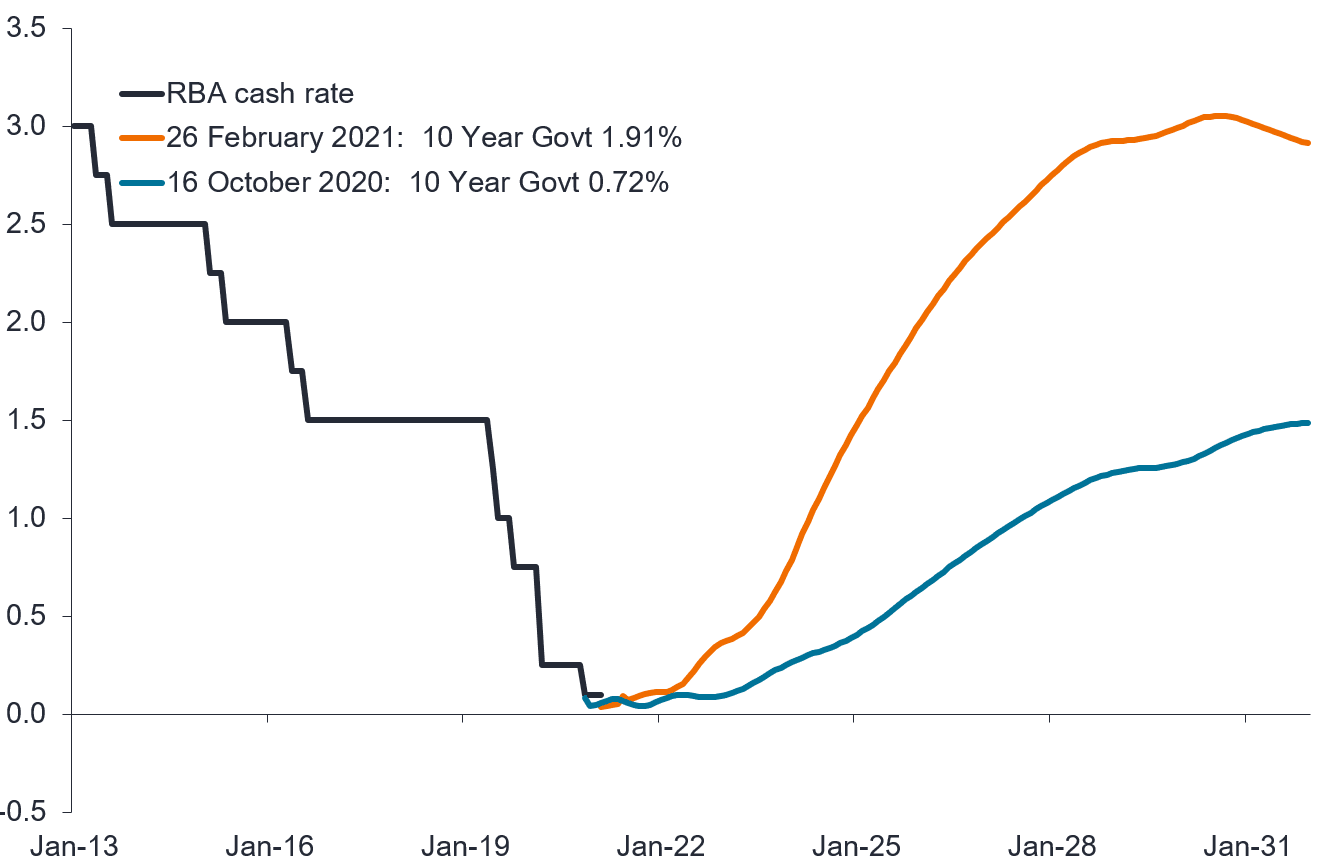

- In Australia, cash rate expectations suggest an RBA cash rate of 3% by late 2028. As at 26 February, with three- and 10-year Australian Government bond yields at 0.127% and 1.91% respectively, there is an embedded expectation that cash rates will rise very quickly, surpassing pre-COVID monetary policy settings into ‘tight’ cash rates.

- To illustrate the shift in cash rate expectations, the chart below depicts the market’s pricing of the future path of cash rates on 26 February 2021 (orange curve), which is nearly three times higher than the market pricing back in October 2020 (blue curve).

Chart 2: Australian implied OIS forward 1m cash rate (%)

Source: Janus Henderson Investors, Bloomberg, monthly to February 2021, spot 26 February 2021.

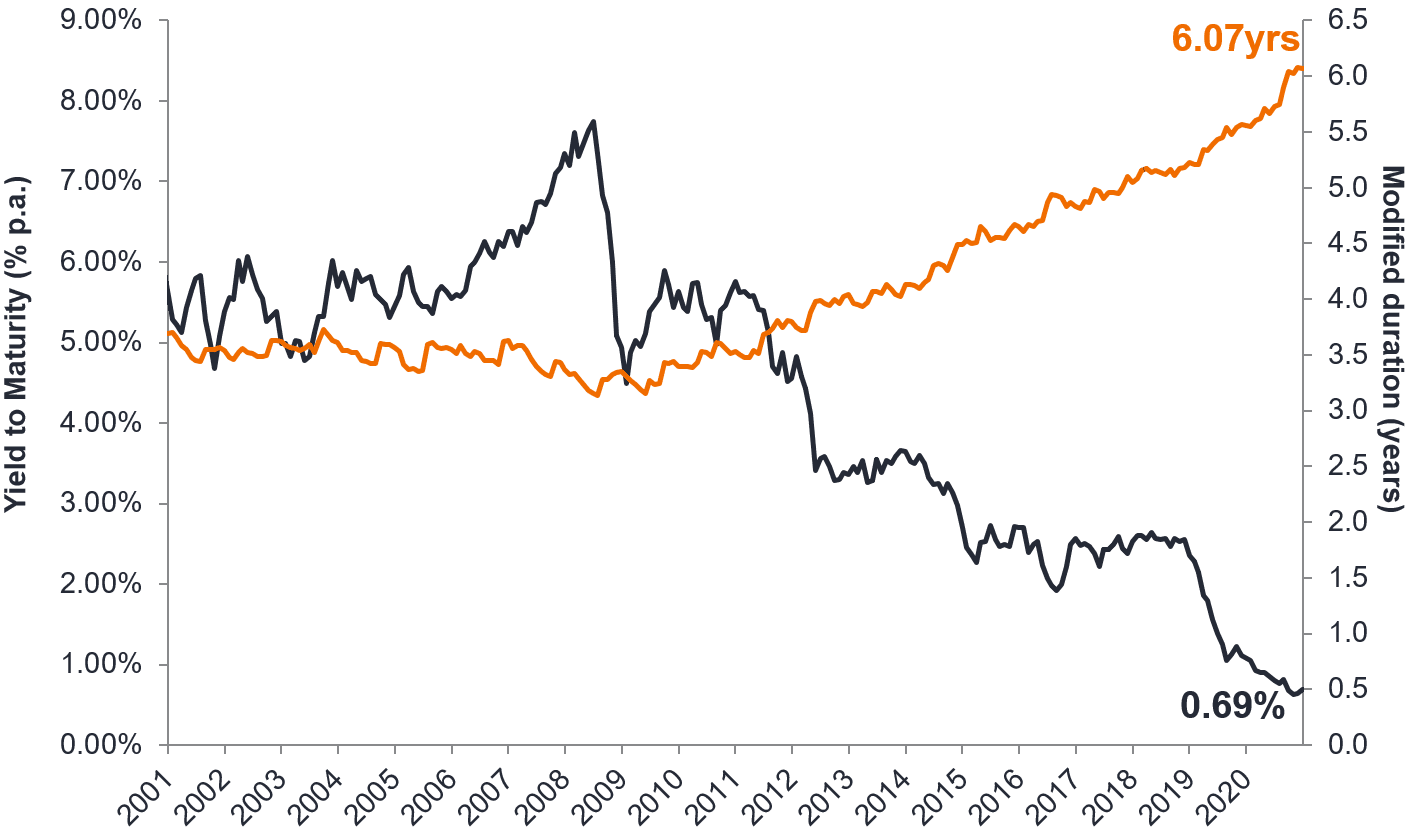

- Interest rate risk (or duration), which is the sensitivity of bond markets to movements in bond yields, is a key risk for fixed interest investors to manage. The pre-conditions for adverse outcomes from the bond market1 had been brewing for a while given it is featuring a potent combination of record high levels of duration and record low bond yields. In general terms, and for illustrative purposes only, the effect of six years of duration essentially means that, even a 1.0% rise in bond yields would result in a 6% decline in capital for index investors.

Chart 3: Yield to maturity and modified duration on the Bloomberg AusBond 0+ Yr Index

Source: Janus Henderson Investors, as at 31 December 2020. Index: Bloomberg Ausbond Composite 0+ Yr Index. Note: Past performance is not a reliable indicator of future performance.

3. Question marks over central bank commitment:

- Despite the asset purchase programs and dovish rhetoric from central banks, markets are pricing in an earlier return to the RBA tightening monetary policy than the 2024 conditional commitment they’ve made.

- Markets are now challenging the central banks on whether they will stay the course with forward guidance and yield curve control (YCC) measures over the next three years.

How we are navigating the turmoil

Effectively navigating the more volatile rising rate environment at the key turning points will be vital given the magnitude of interest rate risk (duration). Ultimately, as yields rise, we believe it is worth taking some duration risk to capture higher yields, especially if markets overshoot.

Higher bond yields when cash rates are anchored at close to zero present very steep yield curves and the opportunity for investors to participate in both the yield and roll-down effect that adds to performance.

Today a 10-year risk free government bond, if nothing happens in markets over the next year, can deliver a return that’s at least twice that of a five-year major bank floating rate corporate bond2. These are exactly the type of opportunities active managers wait for even if some volatility in the near-term needs to be tolerated. One will only know after the fact whether the strategy went too early or too late.

The team have also been focusing on capital preservation strategies to protect against a breakout in inflation expectations.

Below is an overview of our investment strategy:

| Rates: |

|---|

| Duration: |

|

| Inflation protection: |

|

| Spread sectors3: Having participated in the meaningful rally of spread sectors, we feel prudent to take some profit while valuations are at peak levels in the post-COVID market rally. |

|---|

| Semi-government debt: |

|

| Credit protection: |

|

| Investment grade credit: |

|

| High yield: |

|

We are intentionally still exposed to credit markets, but the above provides some room for risk taking should markets become unstable.

This year is shaping up to be one where active interest rate strategies, including taking advantage of higher yields, may overshadow excess returns from spread sectors. Accordingly, our strategies will emphasise this from time to time as prevailing market conditions offer investment opportunities. While we expect some volatility and drawdown, near-term volatility presents an opportunity for active managers. Ultimately, higher bond yields restore the defensive characteristics and create better value for the asset class.

1. Australian Bond Market as measured by the Bloomberg AusBond Composite 0+ Yr Index.

2. Based on no change to the current bond yield of 1.91% for 10-year Australian Government bonds and the estimated yield of an Australian five-year major bank floating rate notes of 0.45% (as at 26 February 2020).

3. The above are the Portfolio Managers’ views and should not be construed as advice. Sector holdings are subject to change without notice. ![]() Don’t miss the

Don’t miss the

latest insights from

Janus Henderson

on LinkedIn. Follow

This information is issued by Janus Henderson Investors (Australia) Institutional Funds Management Limited (AFSL 444266, ABN 16 165 119 531). The information herein shall not in any way constitute advice or an invitation to invest. It is solely for information purposes and subject to change without notice. This information does not purport to be a comprehensive statement or description of any markets or securities referred to within. Any references to individual securities do not constitute a securities recommendation. Past performance is not indicative of future performance. The value of an investment and the income from it can fall as well as rise and you may not get back the amount originally invested.

Whilst Janus Henderson Investors (Australia) Institutional Funds Management Limited believe that the information is correct at the date of this document, no warranty or representation is given to this effect and no responsibility can be accepted by Janus Henderson Investors (Australia) Institutional Funds Management Limited to any end users for any action taken on the basis of this information. All opinions and estimates in this information are subject to change without notice and are the views of the author at the time of publication. Janus Henderson Investors (Australia) Institutional Funds Management Limited is not under any obligation to update this information to the extent that it is or becomes out of date or incorrect.