Reflation optimism at risk of near-term disappointment

Global industrial momentum appears to have peaked and is forecast to move lower into Q2. This poses a risk to reflation-positioned markets.

The global manufacturing PMI new orders index – a timely summary measure of economic momentum – declined for a second month in January. The January fall was cushioned by a jump higher in the US component, possibly reflecting optimism engendered by the Biden administration’s fiscal plans. New orders in the alternative ISM manufacturing survey eased last month.

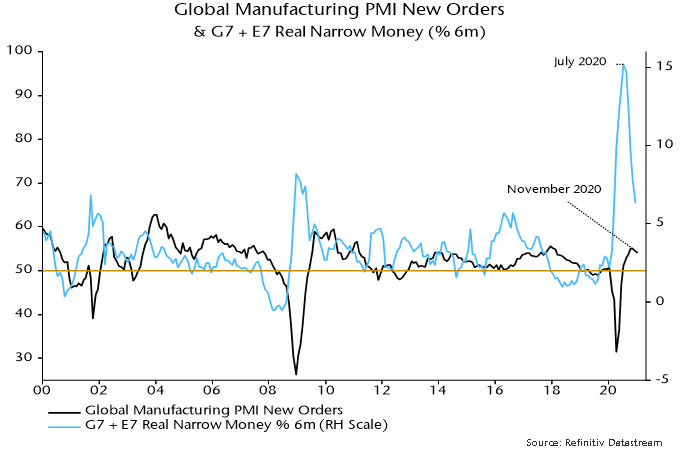

The forecast of a slowdown in industrial momentum is based on a decline in global (i.e. G7 plus E7) six-month real narrow money growth from a July 2020 peak. Full December monetary data confirm a further fall – see chart 1. Real money growth has led turning points in global manufacturing PMI new orders by 6-7 months on average historically, suggesting that the latter will move lower into mid-year. (Caveat: the lead time at the recent peak was four months, assuming that a November top in manufacturing PMI new orders is confirmed.)

Chart 1

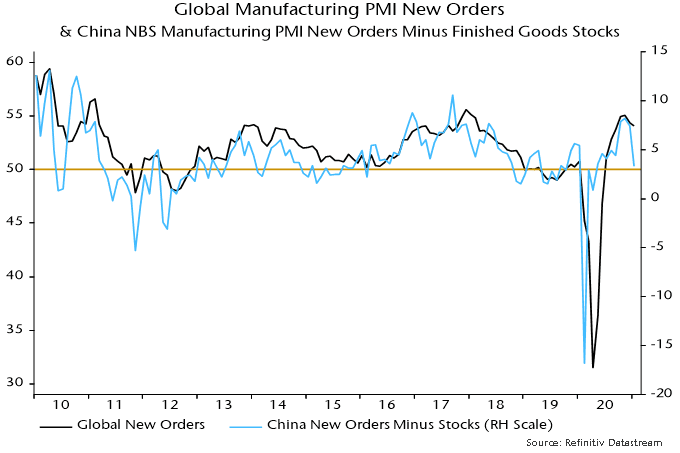

Monetary trends had suggested that China would lead an early 2021 economic slowdown. Chinese money growth picked up relatively modestly last year and slowed later on as the PBoC allowed money rates to rise sharply. Chinese manufacturing PMI new orders fell significantly in January in both the Markit survey (incorporated in the global PMI) and the NBS alternative. The surveys also reported a rise in in finished goods inventories. The differential between NBS new orders and inventories correlates with and often leads global manufacturing PMI new orders – chart 2.

Chart 2

The expectation here had been that the PBoC would recognise downside economic risks and engineer a reversal lower in money rates. This seemed to be playing out, with three-month SHIBOR falling through December and most of January. The PBoC, however, appears to have regarded the decline as excessive and restricted liquidity supply around month-end, causing very short-term rates to spike temporarily. This risks extending the monetary slowdown.

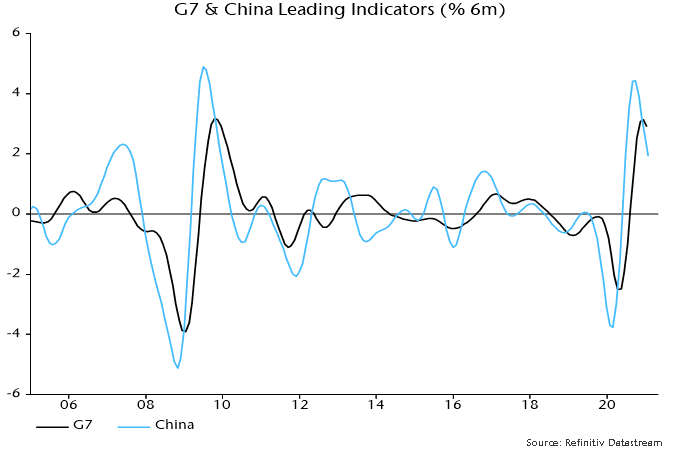

The OECD’s leading indicators support the suggestion that global economic momentum is peaking. The OECD altered the calculation method for its indicators at the start of the pandemic without making this explicit in official documentation. This caused a break in the data that clouds interpretation. Chart 3 shows six-month growth of the G7 indicator calculated on the “old” basis, as well as a Chinese indicator that attempts to replicate the components of the OECD’s US leading indicator. The G7 indicator seems to be confirming an earlier growth peak in the Chinese series.

Chart 3

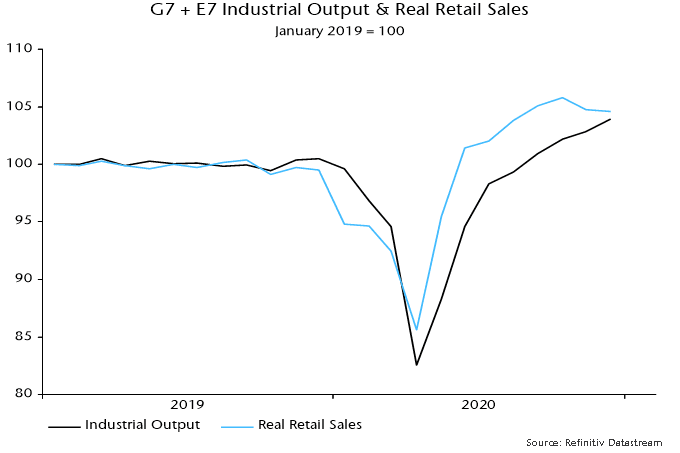

The V-shaped recovery in global industrial output during H2 2020 partly reflected a diversion of consumer spending from services to goods. G7 plus E7 real retail sales, however, fell back in late 2020 – chart 4.

Chart 4

Many forecasters argue that strong industrial output growth will be sustained by a rebound in stockbuilding as firms replenish depleted inventories. The view here has been that the stockbuilding cycle bottomed in Q2 2020 and is unlikely to peak before early 2022. Cycle upswings, however, typically play out in an a-b-c pattern and the initial upthrust (a) may already be complete, suggesting a near-term pause (b) before strength resumes later in the year (c).

The central case here is a modest near-term economic slowdown, with global manufacturing PMI new orders remaining above 50, followed by a reacceleration in H2 2021. This reflects a view that key investment cycles (stockbuilding / business investment / housing) are fundamentally supportive, as well as incorporating the consensus assumption of economic reopening from Q2.

A H2 reacceleration scenario, however, requires an early stabilisation and recovery in global six-month real narrow money growth. A Chinese pick-up had seemed the most likely driver of this but, as noted, appears to have been deferred. US money numbers could be boosted as new stimulus checks are sent out but this is unlikely before late March.

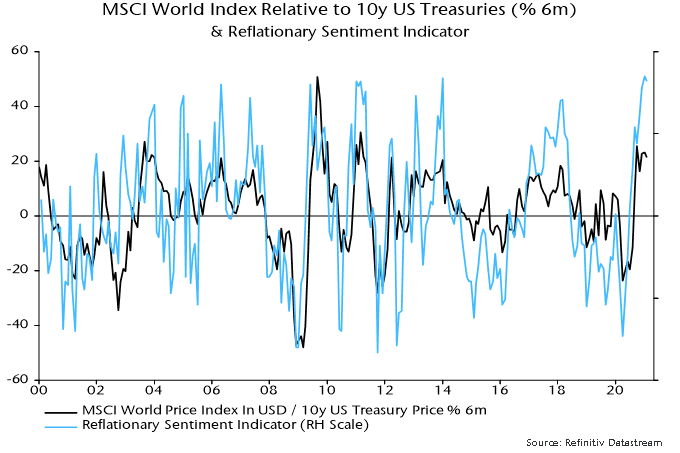

The risk of markets reacting negatively to disappointing near-term economic data is heightened by a strong reflationary bias in current investor positioning. Chart 5 shows a reflationary sentiment indicator derived by combining bullish sentiment data (from Consensus Inc) for various markets that have correlated with global economic momentum historically. An extreme low in the indicator in late March 2020 marked the bottom in equity markets – could the current extreme high mark a short-term top?

Chart 5

These are the views of the author at the time of publication and may differ from the views of other individuals/teams at Janus Henderson Investors. References made to individual securities do not constitute a recommendation to buy, sell or hold any security, investment strategy or market sector, and should not be assumed to be profitable. Janus Henderson Investors, its affiliated advisor, or its employees, may have a position in the securities mentioned.

Past performance does not predict future returns. The value of an investment and the income from it can fall as well as rise and you may not get back the amount originally invested.

The information in this article does not qualify as an investment recommendation.

Marketing Communication.