European smaller companies: fertile ground for active stock pickers

European equities managers Ollie Beckett and Rory Stokes present the case for European smaller companies and explain why the asset class offers bountiful opportunity for active stock pickers.

6 minute read

Key takeaways:

- European small caps have historically outperformed their large cap counterparts most of the time, generally benefiting from stronger balance sheets and higher earnings.

- The sector experiences a large amount of M&A and IPO activity and is relatively under-researched by analysts, providing fertile ground for active stock pickers.

- We believe the next decade will be shaped by sustainability and Europe is a global leader in the sustainability space.

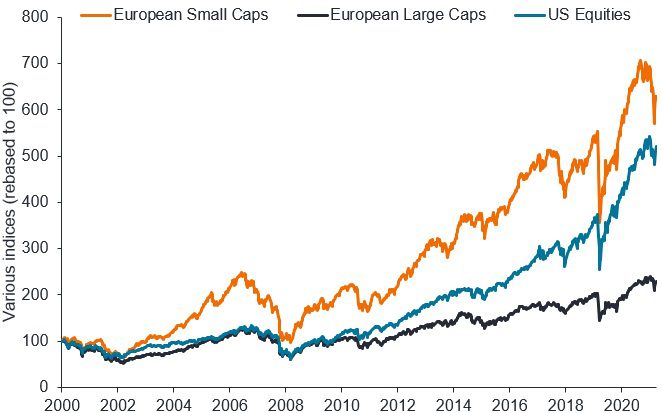

Smaller companies have outpaced large companies

Smaller companies have the potential for higher growth, and with more opportunity for future growth than their larger counterparts. By their very nature, small caps are commonly younger companies, generally early in their development, with room to expand geographically or into adjacent markets, and often operating in faster-growing nascent industries.

In comparison, large cap peers often operate in mature industries and have already expanded their operations globally. These large cap stocks can become reliant on charging higher prices, reducing their costs or taking market share. Some may point to US equities, particularly mega-cap US technology stocks, as an outlier to this trend with their historic ‘winner takes all’ business models. But even here we are seeing saturation difficulties and greater regulatory scrutiny, in addition to a recent anti-growth market stance. In our view, it is less likely for an average large-cap stock to double its revenues from its position when compared to a smaller company.

Figure 1: small caps outperform most of the time

Source: Refinitiv DataStream, Janus Henderson Investors Analysis, in Local currency, as at 31 March 2022. Indices used: European Small Caps = MSCI Europe Small Cap Index, European Large Caps = MSCI Europe Large Cap Index, US Equities = S&P 500 Index. Rebased to 100.

Past performance does not predict future returns.

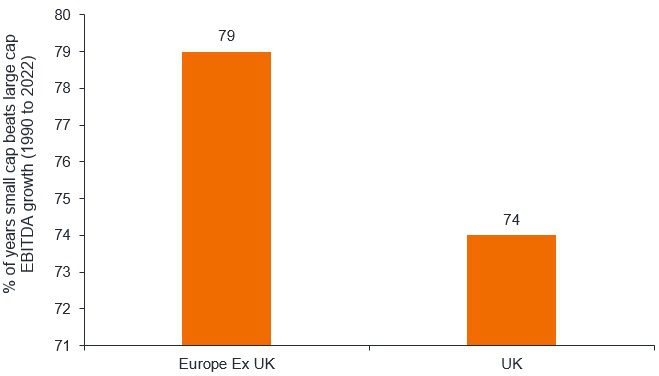

Strong balance sheets and higher earnings provide a solid foundation

Smaller companies are often more reliant on economic growth than large cap stocks. However, strong balance sheets can help these types of companies to survive and even emerge stronger from economic downturns, such as that caused by the COVID-19 pandemic. Data shows that a larger proportion of European smaller companies have more cash and are relatively more attractive valuation-wise when compared to their large cap counterparts. Smaller companies have also historically generated greater growth in earnings than large caps, which has been a driver behind higher performance – figure 2. While this does not suggest that small caps will continue in the same trajectory, this point reinforces the strength of small cap balance sheets.

Figure 2: performance driven by higher earnings growth

Source: JPMorgan research, Janus Henderson Investors Analysis, as at 31 March 2022.EBITDA = Earnings before Interest Tax Depreciation and Amortisation.

Past performance does not predict future returns.

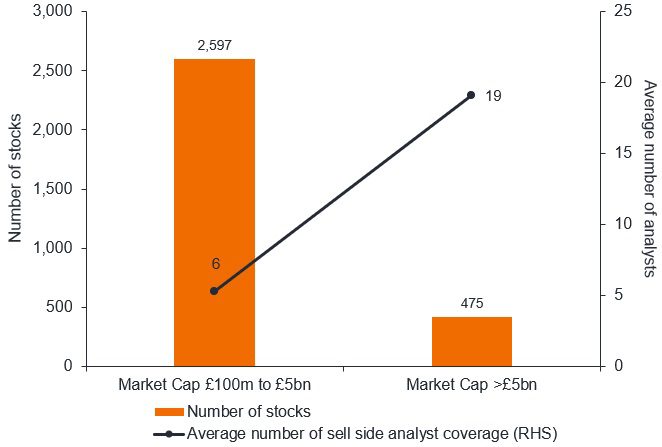

Huge universe of companies largely ignored by sell side research

The European small cap universe offers a much larger pool of less well covered stocks compared to its large cap counterpart. A large majority of these companies are ignored or uncovered by sell side research, leaving the door open for discerning investors to unearth the next gem.

Figure 3: larger universe, less well covered, more mispriced securities

Source: Bloomberg, Janus Henderson Investors Analysis, as at 31 March 2022.

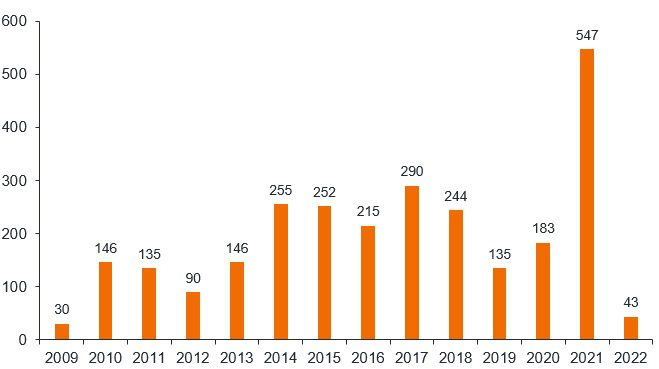

IPO and M&A activity serve as a structural tailwind

In addition to its large universe, western Europe sees a large number of initial public offerings (IPOs) each year, providing a constant stream of new investment opportunities for small cap managers – figure 4. Alongside this is a greater focus on merger and acquisition (M&A) activity, where smaller companies are consistently targeted. This is an important consideration since M&A transactions generally involve a valuation premium being attached to a stock’s undisturbed share price in order to entice existing shareholders. Data shows that around 91% of all M&A transactions from 2008 to 2021 have involved a small cap stock being acquired in Europe.

Figure 4: new companies coming to market

Source: Bloomberg, Janus Henderson Investors Analysis, as at 31 March 2022. Average market cap €780m.

Past performance does not predict future returns.

Are smaller companies meaningfully riskier?

The small cap universe bears several compositional differences compared to large caps. Technology, for one, is significantly less represented within smaller companies. Following a fantastic decade of highly valued tech, we consider this as simply a lower concentration of risk within small caps. Smaller companies are also more likely to be insider owned, i.e. family/cornerstone investor-owned and run. This generally means there is more care taken in how capital is deployed and there is less likelihood of, for example, reckless acquisitions focused on short-term earnings revisions.

European smaller companies – why now?

- Inflation

When compared with large-cap companies, financials, materials and real estate are better represented. This could prove advantageous as these sectors traditionally benefit from rising interest rate environments. Take real estate for example, where an inflationary environment has tended to translate into greater demand and higher occupancy rates. Real estate owners can hike rents in inflationary periods, and many lease contracts featuring rents indexed to grow annually with inflation.

- Valuations

European small caps are at their lowest valuations in the past decade, which makes them attractively valued relative to history. However, we must be aware that further downgrades may come.

Source: Bloomberg, Janus Henderson Investors Analysis, as of 14 June 2022. Forward price-to-earnings (P/E) is a ratio used to value a company’s shares, compared to other stocks or a benchmark index. It is calculated by diving the current share price by its forecasted earnings per share. The MSCI Europe Small Cap Index captures small cap representation across the 15 Developed Markets (DM) countries in Europe*. With 1,050 constituents, the index covers approximately 14% of the free float-adjusted market capitalization in the European equity universe.

Past performance is not a guide to future returns.

- Europe’s green agenda

While the past 10 years have been defined by the pace of mega cap technology, we believe the next decade will be shaped by investment into sustainability. Europe is already a global leader in this space and continues to assert its dominance through the European Union’s many initiatives, totalling more than €1.8 trillion.1 The most recent is the European Recovery Fund, which has put sustainability at the core of efforts to repair the economic and social damage caused by the COVID-19 pandemic. We believe that European companies, many of which already consider sustainability matters, may potentially benefit from the global push towards sustainable practices.

The universe of smaller companies within Europe offers a highly diverse and vibrant mix of growing businesses. With strong balance sheets, solid earnings and less well-covered companies prone to being mispriced, we believe that European smaller companies can provide a significant opportunity for active stock pickers. In addition, the macro backdrop of inflationary pressures and the rising importance of environmental and social factors could stand to benefit the asset class.

1 European Commission, The EU’s NextGenerationEU (NGEU) stimulus package as at November 2020.

Balance sheet – A financial statement that summarises a company’s assets, liabilities and shareholders’ equity at a particular point in time. Each segment gives investors an idea as to what the company owns and owes, as well as the amount invested by shareholders. It is called a balance sheet because of the accounting equation: assets = liabilities + shareholders’ equity.

Environmental, Social and Governance (ESG) – ESG investing considers factors beyond traditional financial analysis. This may limit available investments and cause performance and exposures to differ from, and potentially be more concentrated in certain areas than the broader market.

Growth investing – Growth investors search for companies they believe have strong growth potential. Their earnings are expected to grow at an above-average rate compared to the rest of the market, and therefore there is an expectation that their share prices will increase in value. An anti-growth stance takes the view that growth stocks will not outperform in a certain environment.

Inflation – The rate at which the prices of goods and services are rising in an economy. The CPI and RPI are two common measures.

Initial public offering (IPO) – Initial public offering; when shares in a private company are offered to the public for the first time.

Market cap – Market capitalisation, or market cap is a measure of a company’s size. It is calculated by multiplying the number of shares in issue by the current price of the shares. Large cap stocks tend to be easily bought or sold in the market (highly liquid).

Valuation premium – an excess in the price of the fair value of company or stock based on how much additional value an investor believes the company/stock to be worth. In this case, a valuation premium is added to make a stock more appealing to shareholders of M&A targets.

Smaller company article

These are the views of the author at the time of publication and may differ from the views of other individuals/teams at Janus Henderson Investors. References made to individual securities do not constitute a recommendation to buy, sell or hold any security, investment strategy or market sector, and should not be assumed to be profitable. Janus Henderson Investors, its affiliated advisor, or its employees, may have a position in the securities mentioned.

Past performance does not predict future returns. The value of an investment and the income from it can fall as well as rise and you may not get back the amount originally invested.

The information in this article does not qualify as an investment recommendation.

Marketing Communication.

Important information

Please read the following important information regarding funds related to this article.

- Shares/Units can lose value rapidly, and typically involve higher risks than bonds or money market instruments. The value of your investment may fall as a result.

- Shares of small and mid-size companies can be more volatile than shares of larger companies, and at times it may be difficult to value or to sell shares at desired times and prices, increasing the risk of losses.

- If a Fund has a high exposure to a particular country or geographical region it carries a higher level of risk than a Fund which is more broadly diversified.

- The Fund may use derivatives with the aim of reducing risk or managing the portfolio more efficiently. However this introduces other risks, in particular, that a derivative counterparty may not meet its contractual obligations.

- If the Fund holds assets in currencies other than the base currency of the Fund, or you invest in a share/unit class of a different currency to the Fund (unless hedged, i.e. mitigated by taking an offsetting position in a related security), the value of your investment may be impacted by changes in exchange rates.

- When the Fund, or a share/unit class, seeks to mitigate exchange rate movements of a currency relative to the base currency (hedge), the hedging strategy itself may positively or negatively impact the value of the Fund due to differences in short-term interest rates between the currencies.

- Securities within the Fund could become hard to value or to sell at a desired time and price, especially in extreme market conditions when asset prices may be falling, increasing the risk of investment losses.

- The Fund may incur a higher level of transaction costs as a result of investing in less actively traded or less developed markets compared to a fund that invests in more active/developed markets.

- The Fund could lose money if a counterparty with which the Fund trades becomes unwilling or unable to meet its obligations, or as a result of failure or delay in operational processes or the failure of a third party provider.

Specific risks

6 minute read

Key takeaways:

- European small caps have historically outperformed their large cap counterparts most of the time, generally benefiting from stronger balance sheets and higher earnings.

- The sector experiences a large amount of M&A and IPO activity and is relatively under-researched by analysts, providing fertile ground for active stock pickers.

- We believe the next decade will be shaped by sustainability and Europe is a global leader in the sustainability space.