How do you fit a balanced fund into a balanced portfolio?

Senior Portfolio Strategists Sabrina Denis and Lara Castleton from the Portfolio Construction and Strategy team consider how balanced funds can be used to help build a portfolio that works effectively for investors - particularly pertinent at a time when both equity and fixed income markets have struggled to find their footing amid inflation and growth fears.

6 minute read

Market uncertainty has left many financial professionals unclear about where to turn. Both equity and fixed income markets have struggled to find their footing amidst inflation and growth fears, both of which have been worsened by continued insecurity around the war in Ukraine. Throughout recent consultations, we see a growing number of investors interested in discussing the role and intended use of balanced funds in investment portfolios.

In our recent PCS paper, Fear vs Optimism: Finding the Right Balance with Balanced Funds, we discussed why balanced funds are potentially a great tool to help investors manoeuvre through multiple economic cycles and difficult markets, although robust due diligence is necessary.

Investors who own balanced funds hold, on average, two different strategies in their portfolios, but in some cases a maximum of up to six. In portfolios with balanced funds, the average weight of the strategies is 18%.

Portfolio Construction and Strategy

When considering allocations to balanced funds, the most common question is “how do I use a balanced fund in a portfolio?”. Of course, the answer to this will depend upon the investor’s individual circumstances and objectives. But overall, we see balanced funds being used in three different ways:

1) As an entire portfolio

Using one, or several, balanced fund(s) to build a portfolio can work effectively for investors who aim to fully outsource their allocation process. Balanced funds can automatically rebalance and shift their allocation across multiple assets and/or regions to fit a pre-set risk model. Amongst investors we work with, we have seen this methodology work well for financial professionals who rely upon the resources of outside managers, or those who manage either too many accounts, or too few, where the thresholds required for a bespoke discretionary investment account are too great.

With over 27,300 strategies[1] categorised as “balanced”, financial professionals are not without options to create a portfolio to fit their clients’ needs. However, with that variety comes the need to truly understand the risks, exposures and intended goals for each solution. In our previous article, we have shown the significant dispersion in how different strategies allocate across regions, sectors and asset classes, highlighting the high need for detailed due diligence.

2. As a core allocation

Perhaps most commonly, investors utilise one or more balanced funds as the core component of their portfolio and strengthen this core allocation by adding high-conviction satellite or tactical positions, such as alternatives or specific regional or sector exposures.

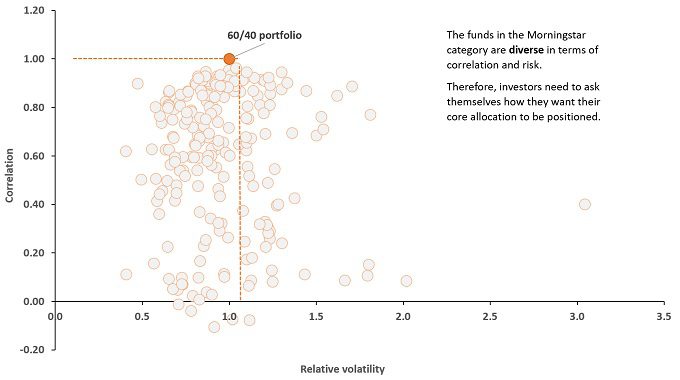

While balanced funds can provide a solid foundation for a core allocation, investors may be surprised to see that the correlations of solutions to a moderate blended 60/40 benchmark range from -0.1 to 0.9. Moreover, the volatility spread can be significant, ranging from half the average volatility to three times as much, using the Morningstar USD Moderate Allocation category as an example.

Due diligence is therefore critical, as investors looking to balanced funds as a core replacement might prefer a high correlation to a traditional 60/40 benchmark as an indicator that the balanced fund can indeed meet their objectives.

Exhibit: Due diligence is critical – many balanced funds are not core replacements

5-year correlation and relative volatility of funds in the Morningstar USD Moderate Allocation category versus a 60/40 blended-index portfolio

Source: Morningstar, Portfolio Construction and Strategy Team, as at May 2022. EAA Funds USD Moderate Allocation Morningstar category, relative to the 5-year correlation and relative volatility (annualised) of a blended benchmark of 60% FTSE All-World Index and 40% FTSE World Government Bond Index (WGBI), May 2017 to May 2022. Past performance does not predict future returns.

3) As a tactical overlay

Finally, investors will often introduce balanced funds to round out their core equity, bond, and alternative allocations. The role of the balanced fund(s) in these circumstances is to serve as an overlay to broader asset allocation decisions – hopefully serving to enhance portfolio returns without jeopardising the overall risk and return goals.

Within this role, it is more important to distinguish options that can truly be both flexible and complementary. Active portfolio management and a dynamic asset allocation approach is key when choosing balanced funds as a tactical overlay to potentially benefit from short-term market dislocations.

Exhibit 2: Flexibility is key to choosing balanced funds

Introducing balanced fund(s) in investors’ portfolios comes with several benefits, depending on its role:

- Simple, cost-effective diversification: with one single investment, investors can gain exposure across different asset classes, styles and markets. The cost constraints to otherwise accomplish this with individual investments can be quite significant.

- One-stop efficient solution: A core allocation to one or more balanced funds frees up significant time for investors to focus on areas of a portfolio that may have larger alpha potential, such as alternatives, concentrated sectors, etc.

- Consistency: investors can be left feeling more confident in their core asset allocation, knowing that it is designed to adjust and navigate through various market conditions.

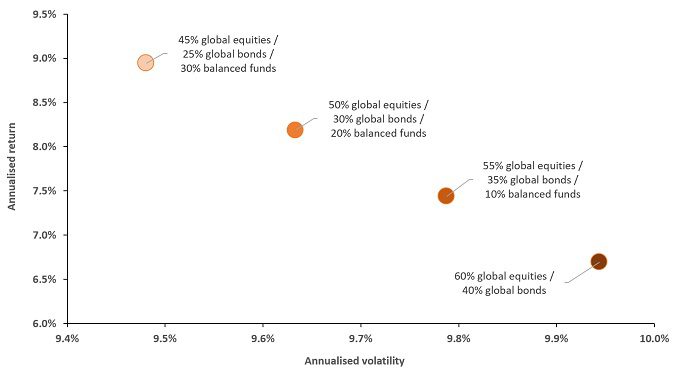

Exhibit 3: A balanced allocation can potentially improve a portfolio’s risk/return profile

Combining an outperforming balanced fund with an index-following passive 60/40 portfolio can reduce overall portfolio risks while potentially improving returns

Source: Morningstar, Portfolio Construction and Strategy Team, as at May 2022. EAA Funds USD Moderate Allocation Morningstar category. 5-Year returns and standard deviation, monthly returns, May 2017 – April 2022. MSCI ACWI All Cap USD and Bloomberg Global Agg TR Hdg USD. Balanced fund returns in this scenario represent the average return for funds in the top 5o percentile of the Morningstar category. Past performance does not predict future returns.

It is worth keeping in mind that, while balanced funds offer various potential advantages, their use can make an overall portfolio less straightforward to assess, in terms of exposure and potential risk. This conundrum, coupled with the range of solutions available in the market, highlights the importance of thorough research and due diligence. Please reach out to our team for a dedicated consultation to ensure the use of balanced fund(s) is helping you to achieve your intended goals.

About the Portfolio Construction and Strategy team

The PCS team performs customised analyses on investment portfolios, providing differentiated, data-driven diagnostics. From a diverse universe of thousands of models emerge trends, themes and potential opportunities in portfolio construction that the team believes could be interesting and beneficial to any investor.

[1] Morningstar Global Category of allocation funds, oldest share class only, as at May 2022.

These are the views of the author at the time of publication and may differ from the views of other individuals/teams at Janus Henderson Investors. References made to individual securities do not constitute a recommendation to buy, sell or hold any security, investment strategy or market sector, and should not be assumed to be profitable. Janus Henderson Investors, its affiliated advisor, or its employees, may have a position in the securities mentioned.

Past performance does not predict future returns. The value of an investment and the income from it can fall as well as rise and you may not get back the amount originally invested.

The information in this article does not qualify as an investment recommendation.

Marketing Communication.

Important information

Please read the following important information regarding funds related to this article.

- Shares/Units can lose value rapidly, and typically involve higher risks than bonds or money market instruments. The value of your investment may fall as a result.

- An issuer of a bond (or money market instrument) may become unable or unwilling to pay interest or repay capital to the Fund. If this happens or the market perceives this may happen, the value of the bond will fall.

- When interest rates rise (or fall), the prices of different securities will be affected differently. In particular, bond values generally fall when interest rates rise (or are expected to rise). This risk is typically greater the longer the maturity of a bond investment.

- The Fund invests in high yield (non-investment grade) bonds and while these generally offer higher rates of interest than investment grade bonds, they are more speculative and more sensitive to adverse changes in market conditions.

- If a Fund has a high exposure to a particular country or geographical region it carries a higher level of risk than a Fund which is more broadly diversified.

- The Fund may use derivatives to help achieve its investment objective. This can result in leverage (higher levels of debt), which can magnify an investment outcome. Gains or losses to the Fund may therefore be greater than the cost of the derivative. Derivatives also introduce other risks, in particular, that a derivative counterparty may not meet its contractual obligations.

- When the Fund, or a share/unit class, seeks to mitigate exchange rate movements of a currency relative to the base currency (hedge), the hedging strategy itself may positively or negatively impact the value of the Fund due to differences in short-term interest rates between the currencies.

- Securities within the Fund could become hard to value or to sell at a desired time and price, especially in extreme market conditions when asset prices may be falling, increasing the risk of investment losses.

- Some or all of the ongoing charges may be taken from capital, which may erode capital or reduce potential for capital growth.

- The Fund could lose money if a counterparty with which the Fund trades becomes unwilling or unable to meet its obligations, or as a result of failure or delay in operational processes or the failure of a third party provider.

- In addition to income, this share class may distribute realised and unrealised capital gains and original capital invested. Fees, charges and expenses are also deducted from capital. Both factors may result in capital erosion and reduced potential for capital growth. Investors should also note that distributions of this nature may be treated (and taxable) as income depending on local tax legislation.

Specific risks

6 minute read

Related insights