US profits boosted by one-offs

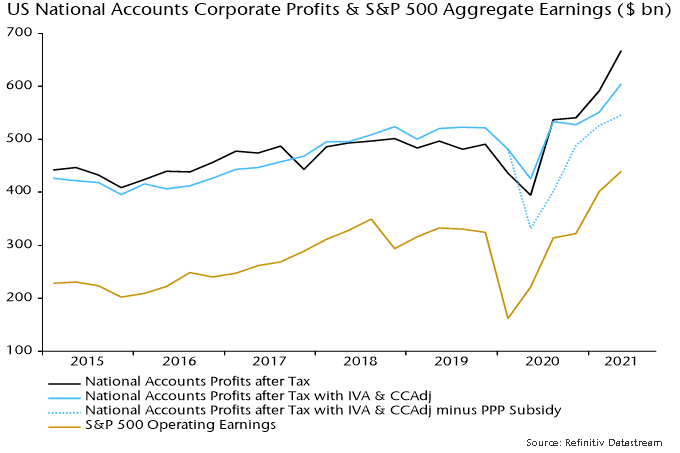

National accounts profits numbers for Q2 released last week mirror recent strength in company earnings reports. The concept closest to S&P 500 earnings – corporate profits after tax – rose by 13% in Q2 to stand 36% above its level in Q4 2019. The national accounts series covers all corporations but S&P 500 operating earnings also grew by 36% between Q4 2019 and Q2 this year – see chart.

The national accounts analysis additionally contains a measure of “economic profits”, i.e. excluding inventory gains and adjusted for the difference between reported and economic depreciation*. Reflecting commodity price strength, inventory profits have been significant in recent quarters, while overreporting of depreciation (to minimise tax bills) fell in 2020 and has remained at a lower level in H1 2021.

This economic profits measure, therefore, has performed less impressively than “headline” earnings, rising by 10% in Q2 to stand 16% above its Q4 2019 level.

This measure, however, still overstates underlying profits strength because it includes government subsidy payments to corporations under various pandemic response schemes, the most significant of which has been the now-closed Paycheck Protection Program. The subsidy payment to corporations under this scheme accounted for 10% of economic profits in Q2 but will fall to zero over coming quarters**.

Q2 profits were also supported by payments under the Employee Retention Tax Credit scheme and grants to air carriers, among other emergency measures.

Excluding only the PPP subsidy, growth of economic profits between Q4 2019 and Q2 this year falls to just 4%.

The level of headline national accounts profits was 22% higher than this adjusted economic profits measure in Q2. A reasonable base case assumption is that this overshoot will be eliminated by Q2 2022.

The consensus forecast is for S&P 500 operating earnings to rise by a modest-sounding 3% in the year to Q2 2022. For national accounts profits to grow at the same pace, underlying profits – i.e. excluding inventory gains, subsidies etc. – might have to increase by more than a quarter. Such strength is implausible, requiring the unlikely combination of rapid economic growth with no associated downward pressure on margins from a tightening labour market.

*Profits after tax with inventory valuation adjustment (IVA) and capital consumption adjustment (CCAdj).**The subsidy payment is recorded as occurring over the term of the loan, not when it is forgiven.

These are the views of the author at the time of publication and may differ from the views of other individuals/teams at Janus Henderson Investors. References made to individual securities do not constitute a recommendation to buy, sell or hold any security, investment strategy or market sector, and should not be assumed to be profitable. Janus Henderson Investors, its affiliated advisor, or its employees, may have a position in the securities mentioned.

Past performance does not predict future returns. The value of an investment and the income from it can fall as well as rise and you may not get back the amount originally invested.

The information in this article does not qualify as an investment recommendation.

Marketing Communication.