Will US fiscal stimulus drive another jump in money measures?

Last year’s US (and global) broad money surge is expected, on the “monetarist” view, to be reflected in a significant inflation rise over 2021-22. US broad money* growth, however, has normalised recently: six-month expansion has retreated from 41% at an annualised rate in July to 4.3% in January. Stabilisation at the current pace would suggest an eventual return of low inflation.

A key driver of the broad money slowdown has been a narrowing of the federal budget deficit after its H1 2020 blowout. The six-month rolling shortfall declined from $2.42 trn to $1.06 trn between July and January. Monetary deficit financing – net lending to the federal government by the Fed, commercial banks and money funds – has fallen accordingly.

President Biden’s stimulus package will drive another deficit surge and a reasonable base case scenario is that this will be associated with a rebound in monetary financing and broad money growth, with unfavourable implications for medium-term inflation prospects.

This monetary scenario, however, is not guaranteed.

Monetary financing by the Fed will rise substantially as the recent pace of Treasury purchases is maintained and the Treasury runs down its deposit balance at the Fed to finance the stimulus package and comply with the 2019 Bipartisan Budget Act. This could, however, be offset by reduced purchases, or even sales, by commercial banks and money funds, reflecting Treasury plans to reduce bill supply and a constraint on banks’ balance sheet expansion from the supplementary leverage ratio (SLR), assuming that this is not relaxed. The recent rise in Treasury yields could attract buying from “real money” domestic investors and foreigners, implying an increase in non-monetary financing of the deficit.

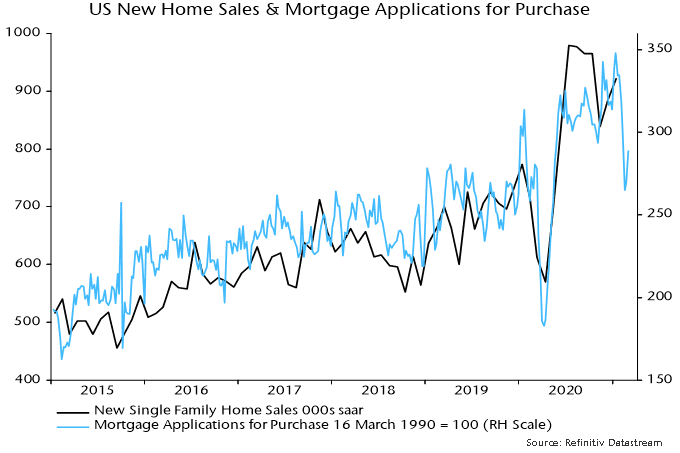

Higher yields could also dampen money growth via their impact on private sector credit demand. The jump in mortgage rates has already been reflected in a fall in mortgage applications for house purchase – chart 1. Growth of commercial banks’ lending book will continue to be dragged down by forgiveness of Payment Protection Program (PPP) loans: of the $521 bn of advances in 2020, only $169 bn had been forgiven as of 4 March.

Chart 1

The upshot is that broad money reacceleration is likely but not certain and there is no alternative to monitoring the incoming monetary data to judge whether another inflationary boost is in the pipeline.

It is, therefore, unfortunate that the Fed recently ended publication of weekly monetary data while pushing back the release of monthly figures to the fourth Tuesday of each month.

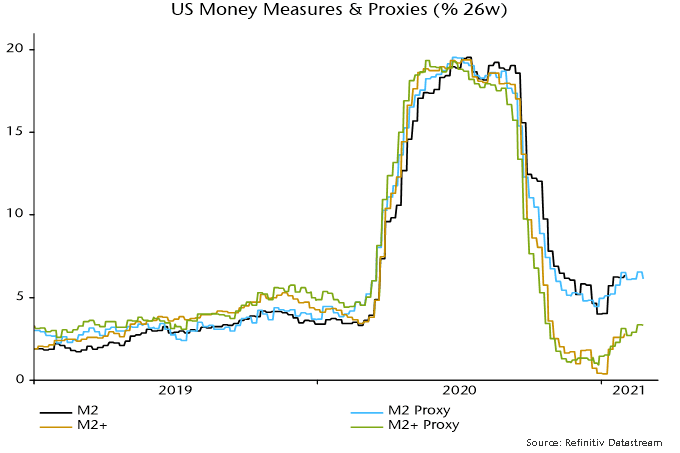

Timely monitoring of monetary trends, however, is still possible using alternative sources of weekly data for currency in circulation, commercial bank deposits and money funds. Chart 2 shows 26-week growth rates (not annualised) of broad money* and M2 up to the final week of Fed data (ending 1 February) along with growth of proxy measures calculated from the alternative sources. Broad money growth remains modest but has firmed since year-end ahead of the expected fiscal package boost. The extent of any further pick-up will be key for assessing medium-term inflation danger.

Chart 2

*”Broad money” refers to “M2+”, calculated as M2 plus large time deposits at commercial banks and institutional money funds.

These are the views of the author at the time of publication and may differ from the views of other individuals/teams at Janus Henderson Investors. References made to individual securities do not constitute a recommendation to buy, sell or hold any security, investment strategy or market sector, and should not be assumed to be profitable. Janus Henderson Investors, its affiliated advisor, or its employees, may have a position in the securities mentioned.

Past performance does not predict future returns. The value of an investment and the income from it can fall as well as rise and you may not get back the amount originally invested.

The information in this article does not qualify as an investment recommendation.

Marketing Communication.