Exploiting the two-way traffic in high yield

Tom Ross, corporate credit portfolio manager, takes a drive in the auto sector to demonstrate how both upgrades and downgrades can be a source of returns.

5 minute read

Key takeaways:

- The crossover space between investment grade and high yield is often replete with pricing inefficiencies, providing fertile opportunities for investors prepared to conduct careful fundamental analysis.

- Identifying bond issuers that might be upgraded is a key part of successful credit investing but bonds that are downgraded into high yield can also offer opportunities due to technical market distortions.

In the first month of 2021 it was announced that Fiat Chrysler, the automaker, had been upgraded by S&P Global Ratings. The decision to move the rating from BB+ to BBB- meant the car maker now had two of the big three rating agencies rating it investment grade (Fitch also rates it BBB-), automatically qualifying it for investment grade status. As such, around €7 billion worth of Fiat Chrysler bonds will cross the divide.

This contrasts with last March when another big auto company – Ford – was downgraded from investment grade to high yield to become a so-called ‘fallen angel’. Back then, this caused US$36 billion worth of debt to move down into high yield.

Locating the stars

Investment grade rated companies are typically able to command lower yields from lenders so an obvious route to successful investing in high yield would be to identify ‘rising stars’ – those companies that are on a likely trajectory to achieving investment grade status. This would be a sound strategy: companies that move up through the ranks typically see their credit spreads narrow.

Yet there is a lot of truth in the old investment adage “it is better to travel than to arrive”. The factors that caused the upgrade of Fiat Chrysler had been circulating for some time, most notably the merger of the company with higher-rated rival auto group Peugeot to form a combined group called Stellantis. S&P noted that the benefits of economies of scale from this merger, improved geographic diversity and a stronger capital structure contributed to the upgrade decision. Holders of Fiat Chrysler bonds will have seen the prices of its bonds rise during late 2020 as investors in the market anticipated the ratings move.

Potential gains from further changes in credit rating may be less dramatic, simply because the distinction between an investment grade credit rating and a high yield credit rating is powerful in terms of index composition and its impact on the investor base. Passive investors and those with mandates that stipulate either investment grade or high yield can be forced to buy or sell whenever a bond crosses the divide.

The market is also made up of investors who might have different opinions on the outlook of a company. This can make the crossover space (the credit ratings area bordering the investment grade/high yield divide) somewhat nebulous in terms of valuations and it is not uncommon for some BBB rated companies to have higher yields than BB rated companies.

Taken together, these blurred lines of valuations, along with the technical impact of forced trading when bonds cross the divide, typically make the crossover space an area high in pricing inefficiencies and a fertile hunting ground for active managers.

When down is up

Returning to our opening story on automakers, the immediate assumption might be that it would have been a bad investment to hold Ford’s bonds after they were downgraded. Yet downgrades from investment grade to high yield can often be quite lucrative for active high yield investors. History has shown that on average credit spreads typically widen ahead of the downgrade and tighten after. The force behind this is often the strong technical impact of investment grade holders seeking to offload a bond they may no longer be permitted to hold after it is downgraded and high yield bond investors subsequently buying it.

This was in evidence with Ford. For example, Ford’s 7.45% 2031 USD bond sold off ahead of the date of the S&P downgrade (25 March 2020) and around the index rebalancing date at the end of March 2020 and then began to rise from early April (Figure 1).

Figure 1: Price of Ford Motor Co 7.45% 16/07/2031 USD

Source: Bloomberg, 31 December 2019 to 20 January 2021.Past performance is not a guide to future performance.

But you might add – weren’t there other factors driving the bond price that had nothing to do with the downgrade? After all, the Ford downgrade coincided with the market sell-off caused by the coronavirus crisis and the economic lockdowns; most corporate bonds fell in March and rallied as 2020 progressed.

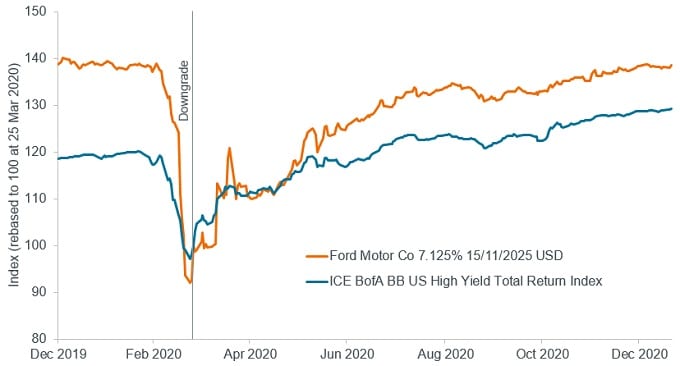

To make it a fairer comparison, let us plot a Ford bond against the US high yield market. To make it fairer still we will include just the BB rated bonds for the market (so we are not comparing with lower rated B and CCC bonds) and we will use a Ford bond that matures in 2025 so that it has a similar duration (interest rate sensitivity) to the BB rated market (around 4-4.5 years) so we help to cancel out any duration effect. In Figure 2 we have rebased the market, represented by the ICE BofA BB US High Yield Index, and the Ford bond to the date of the Ford downgrade. The chart demonstrates significant outperformance from the Ford bond since its downgrade.

Figure 2: Ford has outperformed the wider BB market since its downgrade

Source: Bloomberg, Ford Motor Co 7.125% 15/11/2025 USD Bond, ICE BofA BB US High Yield Total Return Index, in USD, 31 December 2019 to 20 January 2021.Past performance is not a guide to future performance.

Clearly, not every issuer downgraded into high yield will outperform following the downgrade. Some may see their bonds underperform if the credit fundamentals deteriorate. What this demonstrates however is that the high yield market is not as straightforward as it might appear.

Moreover, it can be advantageous for a credit analyst to cover the entire credit spectrum since this can help to maintain a continuous understanding of the fundamental drivers of a company regardless of its credit rating.

They say what goes up must come down but in the world of high yield bonds the reverse can be just as true.

Duration: A measure of a bond’s sensitivity to a change in interest rates, measured in terms of the weighted average of all the security/portfolio’s remaining cash flows (both coupons and principal). It is expressed as a number of years. The larger the figure, the more sensitive it is to a movement in interest rates.

These are the views of the author at the time of publication and may differ from the views of other individuals/teams at Janus Henderson Investors. References made to individual securities do not constitute a recommendation to buy, sell or hold any security, investment strategy or market sector, and should not be assumed to be profitable. Janus Henderson Investors, its affiliated advisor, or its employees, may have a position in the securities mentioned.

Past performance does not predict future returns. The value of an investment and the income from it can fall as well as rise and you may not get back the amount originally invested.

The information in this article does not qualify as an investment recommendation.

Marketing Communication.

5 minute read

Key takeaways:

- The crossover space between investment grade and high yield is often replete with pricing inefficiencies, providing fertile opportunities for investors prepared to conduct careful fundamental analysis.

- Identifying bond issuers that might be upgraded is a key part of successful credit investing but bonds that are downgraded into high yield can also offer opportunities due to technical market distortions.