Treading carefully: A balancing act for 2023

Global Head of Portfolio Construction and Strategy Adam Hetts introduces the latest Trends and Opportunities report, which outlines key themes for the next stage of this market cycle and their nuanced implications across global asset classes.

5 minute read

Key takeaways:

- As we enter a new era characterized by structurally higher rates and fresh discounts across major global asset classes, investors will need to tread carefully.

- However, while we think volatility will continue in the year ahead, we also believe that volatility may present a silver lining for those who are bold enough to forge ahead.

- The portfolio solutions we highlight in this edition have the potential help navigate this new environment and address the ubiquitous asset allocation gaps and concentrations we see in investor portfolios.

In our mid-year 2022 instalment of Trends and Opportunities, titled “Shock Therapy,” on three profound market shocks that drove an extremely volatile year: slowing growth, inflation, and a historic interest rate reset. The report focused on providing “shock therapy” in the form of portfolio solutions tailored to this new investing paradigm. Now we enter a new era characterised by structurally higher interest rates and fresh discounts across major global asset classes. Investors will need to watch their step as they venture into this new territory.

As we enter a new era characterized by structurally higher rates and fresh discounts across major global asset classes, investors will need to tread carefully.

What does ‘Treading carefully’ mean to you?

Our title for this edition, “Treading carefully,” serves as a Rorschach test: do you read it as meaning investors will fight to stay afloat in murky waters in 2023, or do you think it implies that those who are bold enough to persevere through the volatility may be rewarded?

We believe wise investors recognise that both interpretations apply. In our view, 2022’s historic volatility has given rise to two dependable investment themes for the year ahead: 1) Volatility will continue, and 2) that volatility presents a silver lining for those who are bold enough to forge ahead. The new portfolio solutions we highlight in this edition were selected because they have the potential to help portfolios thrive by navigating those themes.

Equity

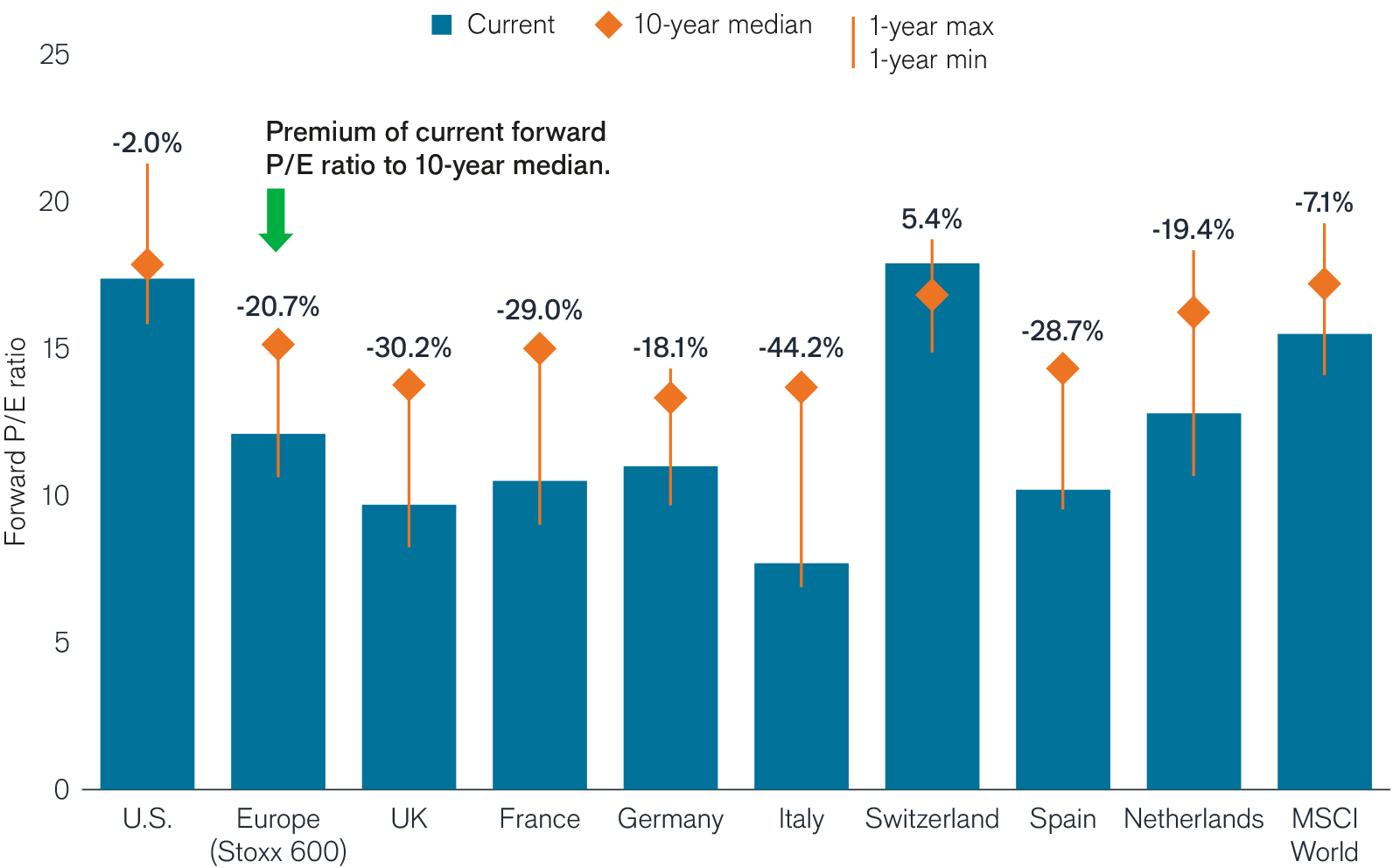

One of 2022’s many mindbenders was that ‘duration’ became a major risk for equities – not just fixed income. The historic magnitude and speed of rate increases was the primary driver of losses for the S&P 500® Index in 2022, with the silver lining being that the S&P 500 entered 2023 with a P/E of 17.5x – in line with its historical average. The focus for U.S. large-cap investors now shifts from the “P” to the “E”: finding resilient earnings amid an economic slowdown. Meanwhile, U.S. small- and mid-cap stocks historically outperform large-caps during the early stages of recoveries.

Looking further afield, unlike U.S. stocks, ex-U.S. developed market equities carry a valuation discount, potentially offering a better ‘margin of safety’ to help absorb some earnings weakness. Couple this discount with their more cyclical, higher-yielding characteristics, and ex-U.S. equities present strong upside potential (Exhibit 1).

Exhibit 1: Global P/E Ratios

Source: Bloomberg, as at 31 December 2022.

Past performance is no guarantee of future results.

Looking across all global equity sectors, healthcare was the second-best performer in 2022, trailing only the energy sector. While we are looking to healthcare as a whole for its resiliency, we also see biotech as an important subsector that is offering attractive discounts as it potentially recovers from a severe drawdown.

Fixed income

Fixed Income

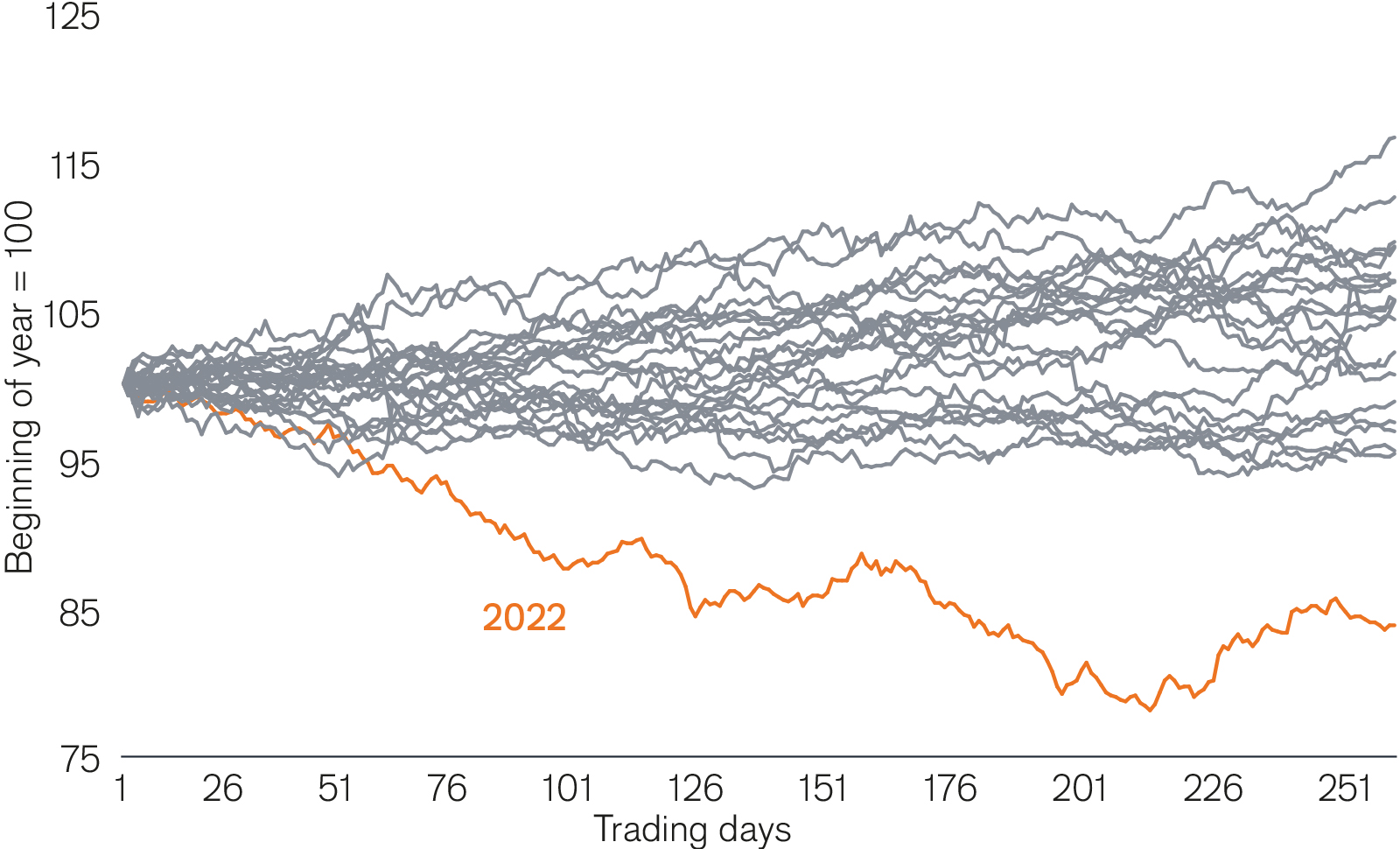

The aforementioned ‘magnitude and speed of rate increases’ is a euphemism for what actually happened in fixed income last year: 2022 was the asset class’s worst year in a generation (Exhibit 2).

Exhibit 2: Annual trajectory of Global Aggregate Index since 1999

Source: Bloomberg, as at 31 December 2022.

Note: Quarterly returns based on Bloomberg Global Aggregate Index.

Past performance is not a guarantee of future performance.

Fortunately, “bonds are math,” as they say, and this historic sell-off creates obvious silver linings. The reset in rates has created a level of yield cushion not seen in many years that may help buffer bond returns during any further rate increases, while the disproportionate increase in shorter-term rates caused short-duration yields to exceed those of intermediate-duration bonds.

Forward returns in corporate credit markets are beneficiaries of both the reset in rates and a moderate amount of spread widening in 2022. If the potential global slowdown in 2023 serves to widen spreads, the high starting yields in corporates may help cushion losses.

Moving forward

Treading carefully requires a delicate balance of defense and offense. The Portfolio Construction and Strategy Team is focused on providing portfolio solutions to help navigate this new environment and address the ubiquitous asset allocation gaps and concentrations we see in investor portfolios through our consultations with financial professionals.

Continue reading our Trends and Opportunities report for more details on these portfolio solutions.

Bloomberg Global Aggregate Bond Index is a broad-based measure of the global investment grade fixed-rate debt markets.

Credit Spread is the difference in yield between securities with similar maturity but different credit quality. Widening spreads generally indicate deteriorating creditworthiness of corporate borrowers, and narrowing indicate improving.

Duration measures a bond price’s sensitivity to changes in interest rates. The longer a bond’s duration, the higher its sensitivity to changes in interest rates and vice versa.

Price-to-Earnings (P/E) Ratio measures share price compared to earnings per share for a stock or stocks in a portfolio.

S&P 500® Index reflects U.S. large-cap equity performance and represents broad U.S. equity market performance.

STOXX® Europe 600 Index represents large, mid and small capitalization companies across 17 countries in the European region.

Yield cushion, defined as a security’s yield divided by duration, is a common approach that looks at bond yields as a cushion protecting bond investors from the potential negative effects of duration risk. The yield cushion potentially helps mitigate losses from falling bond prices if yields were to rise.

Volatility measures risk using the dispersion of returns for a given investment.

IMPORTANT INFORMATION

Equity securities are subject to risks including market risk. Returns will fluctuate in response to issuer, political and economic developments.

Fixed income securities are subject to interest rate, inflation, credit and default risk. The bond market is volatile. As interest rates rise, bond prices usually fall, and vice versa. The return of principal is not guaranteed, and prices may decline if an issuer fails to make timely payments or its credit strength weakens.

Foreign securities are subject to additional risks including currency fluctuations, political and economic uncertainty, increased volatility, lower liquidity and differing financial and information reporting standards, all of which are magnified in emerging markets.

MSCI World Index℠ reflects the equity market performance of global developed markets.

Smaller capitalization securities may be less stable and more susceptible to adverse developments, and may be more volatile and less liquid than larger capitalization securities.

These are the views of the author at the time of publication and may differ from the views of other individuals/teams at Janus Henderson Investors. References made to individual securities do not constitute a recommendation to buy, sell or hold any security, investment strategy or market sector, and should not be assumed to be profitable. Janus Henderson Investors, its affiliated advisor, or its employees, may have a position in the securities mentioned.

Past performance does not predict future returns. The value of an investment and the income from it can fall as well as rise and you may not get back the amount originally invested.

The information in this article does not qualify as an investment recommendation.

Marketing Communication.

5 minute read

Key takeaways:

- As we enter a new era characterized by structurally higher rates and fresh discounts across major global asset classes, investors will need to tread carefully.

- However, while we think volatility will continue in the year ahead, we also believe that volatility may present a silver lining for those who are bold enough to forge ahead.

- The portfolio solutions we highlight in this edition have the potential help navigate this new environment and address the ubiquitous asset allocation gaps and concentrations we see in investor portfolios.