with high dividends")

Subscribe

Sign up for timely perspectives delivered to your inbox.

Global Head of Portfolio Construction and Strategy Adam Hetts explains why, given the unique nature of this year’s sell-off and subsequent recovery, sector and style decisions should not be based on a traditional recovery playbook.

This article is part of the latest Trends and Opportunities report, which seeks to provide therapy for recent market shocks by offering long-term perspective and potential solutions.

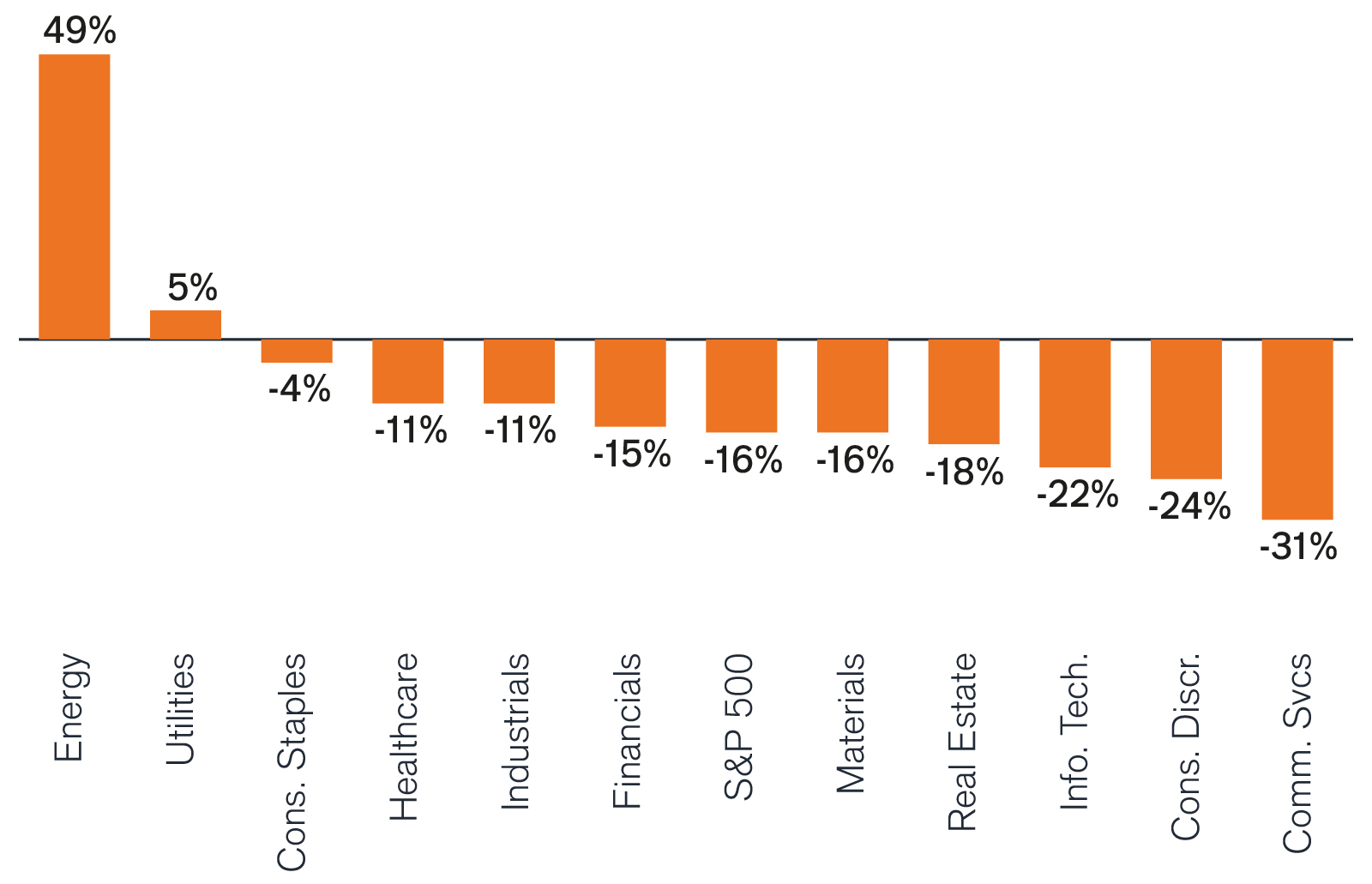

The unique nature of this year’s sell-off is giving rise to an equally unique recovery environment.

| Value | Core | Growth | |

|---|---|---|---|

|

Large

|

-9.8% | -16.9% | -23.2% |

|

Mid

|

-11.8% | -16.5% | -25.1% |

|

Small

|

-12.2% | -17.2% | -22.3% |

Source: Morningstar, YTD returns through 8/31/22; Style/size table based on Russell indices, sector chart based on GICS sectors of S&P 500 Index.

| Key Risk | Defense | |

|---|---|---|

| Margins | Inflation | Wide margins, pricing power |

| Ownership | Slowing Growth | Nimble management to navigate a downturn |

| Advantages | Slowing Growth | Competitive advantages and durable growth opportunities |

| Tenacity | Rate Volatility | Low leverage and/or long-term financing |

This article is part of the latest Trends and Opportunities report, which seeks to provide therapy for recent market shocks by offering long-term perspective and potential solutions.

The unique nature of this year’s sell-off is giving rise to an equally unique recovery environment.

| Value | Core | Growth | |

|---|---|---|---|

|

Large

|

-9.8% | -16.9% | -23.2% |

|

Mid

|

-11.8% | -16.5% | -25.1% |

|

Small

|

-12.2% | -17.2% | -22.3% |

Source: Morningstar, YTD returns through 8/31/22; Style/size table based on Russell indices, sector chart based on GICS sectors of S&P 500 Index.

| Key Risk | Defense | |

|---|---|---|

| Margins | Inflation | Wide margins, pricing power |

| Ownership | Slowing Growth | Nimble management to navigate a downturn |

| Advantages | Slowing Growth | Competitive advantages and durable growth opportunities |

| Tenacity | Rate Volatility | Low leverage and/or long-term financing |

Sign up for timely perspectives delivered to your inbox.