Subscribe

Sign up for timely perspectives delivered to your inbox.

Portfolio Manager Jason England believes that by raising interest rates to 5.25%, the Federal Reserve (Fed) has bought itself time to assess the degree to which previous hikes have quelled persistent inflation.

In the game of chicken between the Federal Reserve (Fed) and the bond market that’s been going on since last year, the U.S. central bank won out by reaching its stated terminal rate of 5.25% for this tightening cycle. Still to be determined is how long the upper limit of the federal funds rate remains at this level. The Fed has been adamant that it’s premature to consider a rate cut – expecting the 5.25% level to stick through the end of 2023 – whereas the market divines that rates will slide to 4.50% by December.

Leading into the May meeting, many market participants were eager to categorize the well-telegraphed 25 basis point (bps) increase as a dovish hike. We don’t think that’s the case, as Fed Chairman Jerome Powell and other voting members rightly recognize the risks posed by inflation to consumers’ purchasing power and price stability across the economy. Consequently, we see this week’s decision as a modestly hawkish pause that will allow the Fed to gauge previous rate increases’ impact on further lowering inflation.

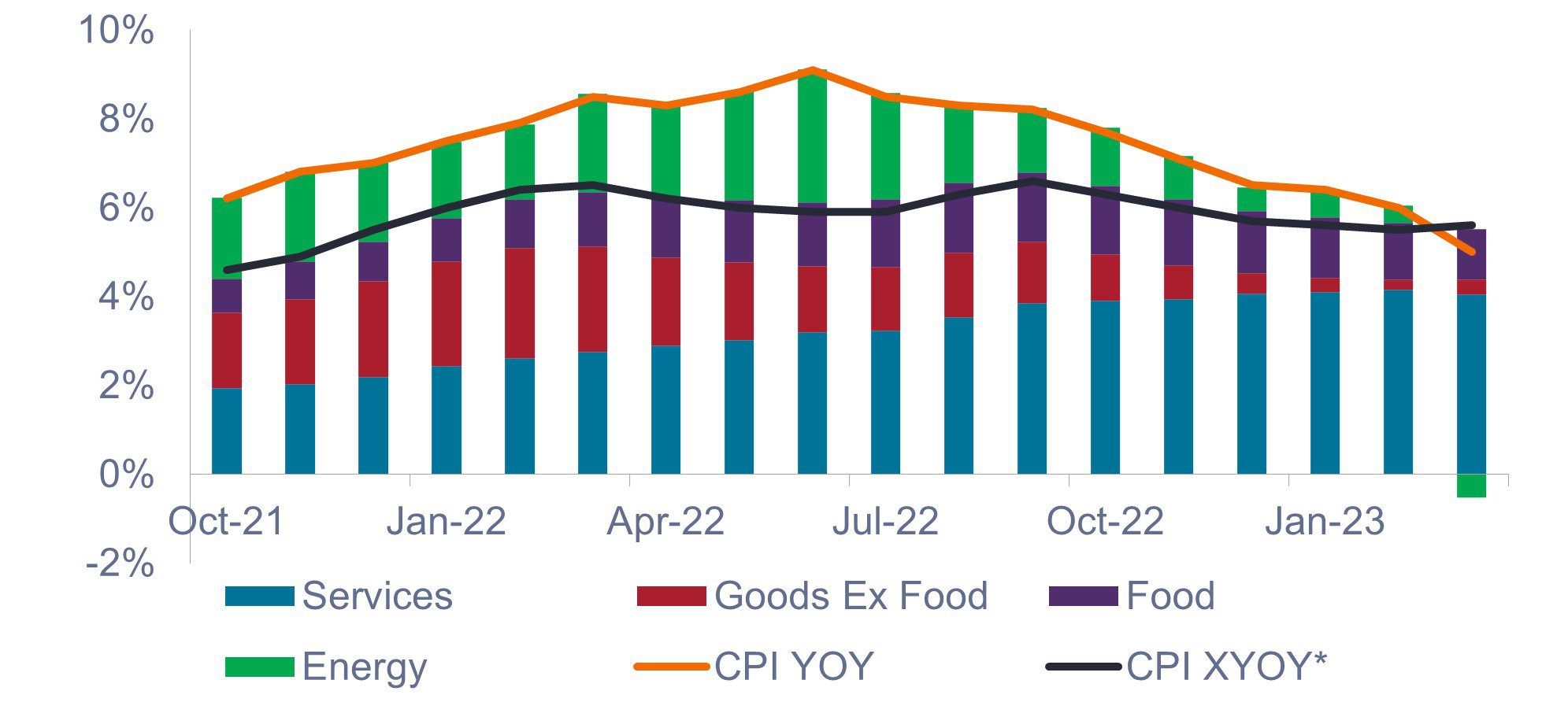

We’ve long stated that it would be much easier to lower inflation from its 9.1% peak to 5.0%, based on the U.S. Consumer Price Index, than it would be to get from 5.0% to the Fed’s 2.0% objective. For perspective, the Fed’s preferred measure of inflation – the Core Personal Consumption Expenditure Price Index – has fallen a more muted 5.4% to 4.6%. Standing in the way is the persistent nature of this bout of inflation, especially the stickiness of service-sector wages due to a historically tight labor market.

While both headline and core inflation have fallen, services – with their notoriously sticky wage component – have become a much larger component of overall price increases.

Source: Bloomberg, as of 3 May 2023. *CPI XYOY = CPI urban consumers, less food and energy (YoY% change).

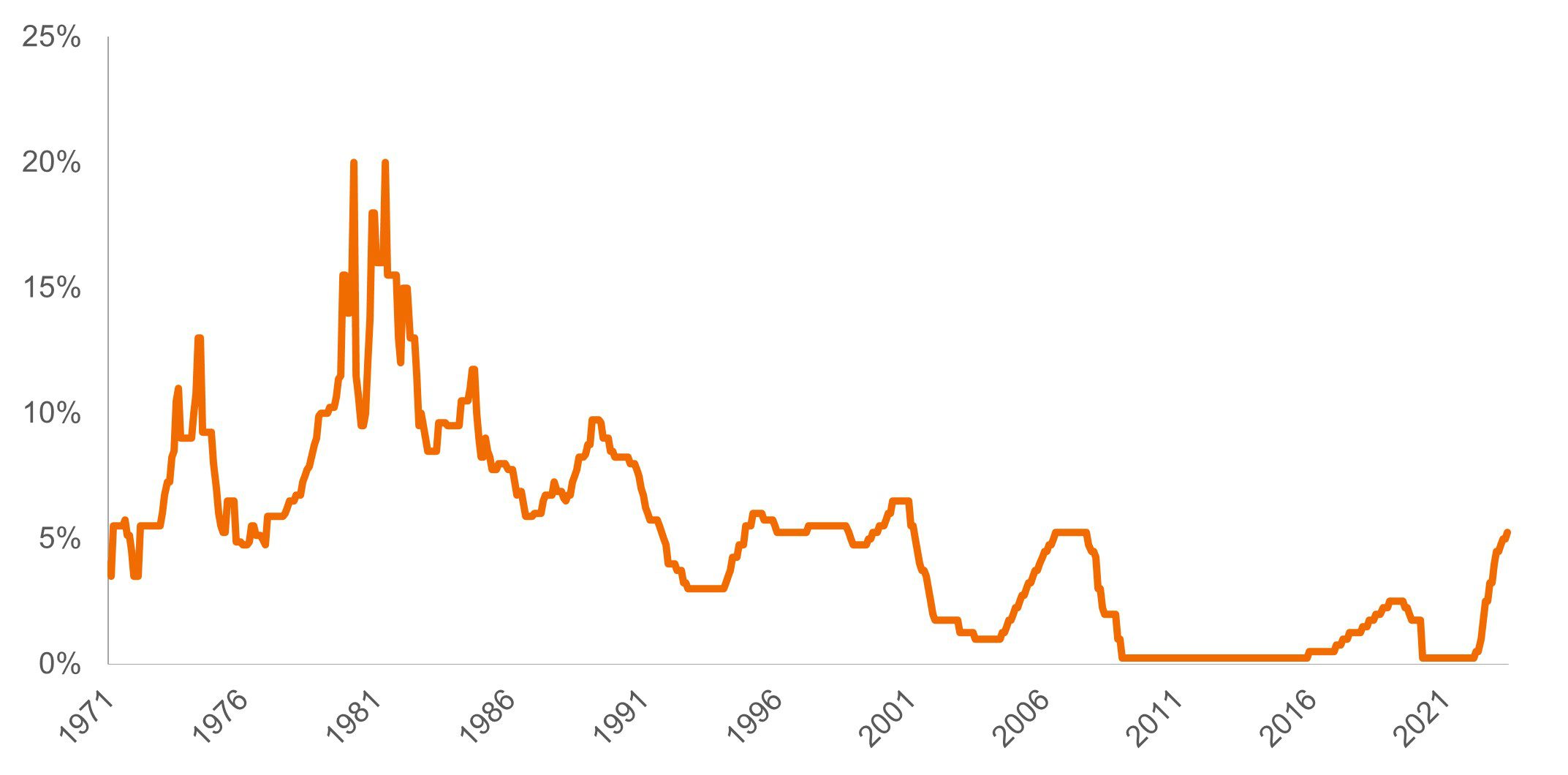

Many have suggested that with several leading indicators – namely an inverted U.S. Treasuries yield curve – already signaling weakness, the Fed may stick to its tendency of transitioning to rate cuts in relatively short order. Probabilities based on futures markets imply a cut by as soon as July. We don’t think that will be the case, however. Historically, quicker pivots have occurred when the central bank prematurely turned dovish, such as during the 1970s and early 1980s. This only allowed inflation to become more imbedded, setting the stage for policy having to ultimately become even more restrictive.

The Fed has historically pivoted relatively quickly once having reached its cycle terminal rate, but we doubt that will be the case this time.

Source: Bloomberg, as of 3 May 2023.

Admittedly, both inflation and employment are lagging indicators, and once they roll over, the economy is already on a decidedly downward path. At the risk of deploying an overused market cliché, we believe this time may be different given the persistence and pervasiveness of inflation globally and the perplexing dearth of U.S. workers.

Some progress is being made on both these fronts: U.S. job openings are down 20% from their peak, and while still in expansion territory, the employment component of the U.S. Services Purchasing Managers Index has dipped toward contraction territory over the past few months. Yet, with more work likely necessary to keep inflation heading lower, we believe the Fed is more apt to take a potentially extended pause – and even surprise markets with another 25 bps hike later in the year should the data merit it – rather than implement a poorly timed pivot.

Chairman Powell again addressed the failure of several U.S. banks, stating that the country’s banking system remains healthy and well capitalized. While an unwelcome development, skittishness among the banking community may play into to Fed’s hands. We believe that the tightening credit standards that are likely the result of the banking tumult could translate to the equivalent of roughly an additional 25 bps rate increase.

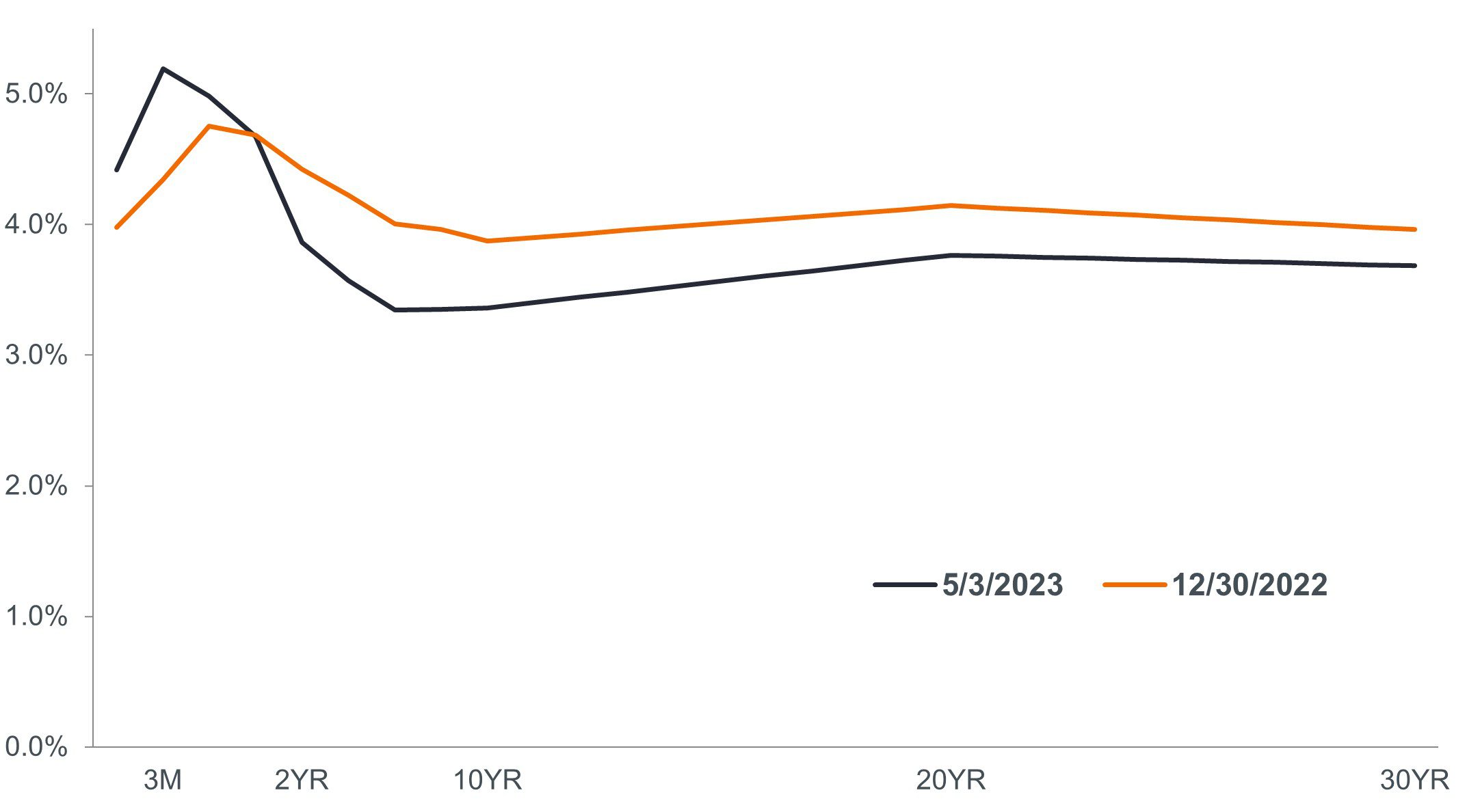

With the end of this tightening cycle likely on the horizon, bond investors can begin thinking about shifting toward an opportunistic stance within the global market. While inflation is a global phenomenon driven in part by ascendant forces such as deglobalization and tight labor markets, we are starting to see divergence in the policy paths of different regions. The U.S., for instance, was forceful – albeit late – in its response. This is evident in yields on all but the shortest of maturities having fallen in 2023.

The fall in yield across all but the shortest of maturities indicates that the Fed is likely nearing the end of its hiking cycle, while other jurisdictions may experience additional upward pressure, especially along the front end.

Source: Bloomberg, as of 3 May 2023.

Australia, meanwhile, caught the market somewhat off guard with its recent rate increase, but its policy rate remains well below that of the U.S. And the European Central Bank was late to the game and has been playing catch-up since mid-2022 in an attempt to drive down headline inflation of 7.0%. The upshot is bond investors now have the ability to not only capture levels of income not available only a year ago, but also position themselves to participate in the capital appreciation that can diversify against riskier assets in times of stress. Indeed, this is how U.S. bonds performed during the volatile stretch caused by banking sector tumult.

Lastly, bond investors need to recognize that the days of chasing yield are over. A higher cost of capital has put many companies that are dependent upon cheap financing on the back foot. Tightening credit standards will only exacerbate this trend. We are especially cautious of lower-quality companies and those exposed to a high degree of economic cyclicality. Instead, we believe that the resetting of yields has made corporate issuers with proven management teams and the ability to consistently generate cash flow throughout the cycle an attractive destination on a risk-adjusted basis.

Basis point (bp) equals 1/100 of a percentage point. 1 bp = 0.01%, 100 bps = 1%.

Consumer Price Index (CPI) is an unmanaged index representing the rate of inflation of the U.S. consumer prices as determined by the U.S. Department of Labor Statistics.

Core Personal Consumption Expenditure Price Index is a measure of prices that people living in the United States pay for goods and services, excluding food and energy.

Purchasing Managers’ Index (PMI) is an index of the prevailing direction of economic trends in the manufacturing and service sectors, based on a survey of private sector companies.

A yield curve plots the yields (interest rate) of bonds with equal credit quality but differing maturity dates. Typically bonds with longer maturities have higher yields.

An inverted yield curve occurs when short-term yields are higher than long-term yields.

IMPORTANT INFORMATION

Diversification neither assures a profit nor eliminates the risk of experiencing investment losses.

Sign up for timely perspectives delivered to your inbox.