Quality is a virtue

Global Head of Portfolio Construction and Strategy Adam Hetts explains why, given the unique nature of this year’s sell-off and subsequent recovery, sector and style decisions should not be based on a traditional recovery playbook.

3 minute read

This article is part of the latest Trends and Opportunities report, which seeks to provide therapy for recent market shocks by offering long-term perspective and potential solutions.

The unique nature of this year’s sell-off is giving rise to an equally unique recovery environment.

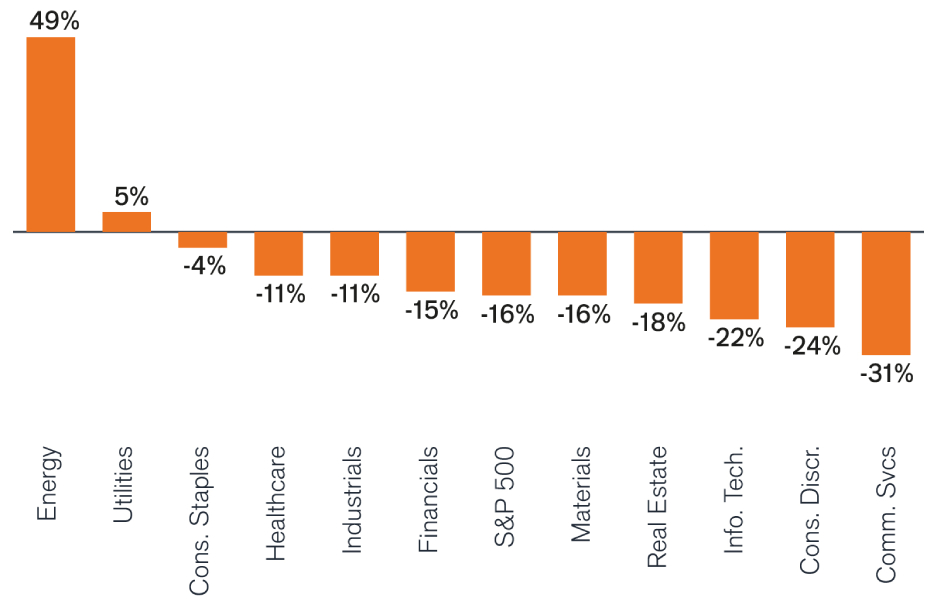

YTD Recap

- As widely expected, rising rates and inflation have taken the largest toll on growth (down -23.2% YTD), which has shown roughly twice the downside of value (-9.8%).

- At a sector level, that same pressure on growth shows in the underperformance of Communication Services (-31%) and Information Technology (-22%), and with Consumer Discretionary (-24%) also suffering due to its particular sensitivity to economic conditions.

- Even in the face of slowing growth, classically cyclical sectors have performed relatively well (e.g., Energy +49%, Industrials -11%, Financials -15%, Materials -16%).

U.S. Equity Style, Size, and Sector Returns

| Value | Core | Growth | |

|---|---|---|---|

|

Large

|

-9.8% | -16.9% | -23.2% |

|

Mid

|

-11.8% | -16.5% | -25.1% |

|

Small

|

-12.2% | -17.2% | -22.3% |

Source: Morningstar, YTD returns through 8/31/22; Style/size table based on Russell indices, sector chart based on GICS sectors of S&P 500 Index.

Outlook

- As multiple compression now gives way to a focus on earnings as the key determinant of stock performance, investors need to be mindful that not all earnings are created equal: the composition of earnings will carry significant forward-looking implications as companies battle global supply chains, financing costs, fickle consumer demand, and other headwinds.

- Earnings forecasts do not fully reflect company-level challenges ahead, and focus should turn to idiosyncratic risks and opportunities.

- With so much bad news priced into equities, there is proportionately more upside opportunity than downside risk remaining.

The Quality Equity MOAT: A framework to battle stagflation

| Key Risk | Defense | |

|---|---|---|

| Margins | Inflation | Wide margins, pricing power |

| Ownership | Slowing Growth | Nimble management to navigate a downturn |

| Advantages | Slowing Growth | Competitive advantages and durable growth opportunities |

| Tenacity | Rate Volatility | Low leverage and/or long-term financing |

PCS Perspective

- The unique nature of this year’s sell-off is giving rise to an equally unique recovery environment, marked by many fits and starts, where sector and style decisions shouldn’t be made according to a typical recovery playbook.

- Those typical playbooks depend on superficial categories – e.g., growth vs. value, cyclical vs. defensive – which are losing relevance for this unique recovery.

- Instead, think mechanically and map today’s biggest risks to the moving parts of individual companies: e.g., margins, leverage, competitive landscape, management strategy.

- To simplify this extremely complex task, our MOAT framework for quality equity investing identifies individual stocks which mitigate – and even capitalise on – today’s biggest risks so that investors can defend against stagflation and be prepared for the subsequent upside.

These are the views of the author at the time of publication and may differ from the views of other individuals/teams at Janus Henderson Investors. References made to individual securities do not constitute a recommendation to buy, sell or hold any security, investment strategy or market sector, and should not be assumed to be profitable. Janus Henderson Investors, its affiliated advisor, or its employees, may have a position in the securities mentioned.

Past performance does not predict future returns. The value of an investment and the income from it can fall as well as rise and you may not get back the amount originally invested.

The information in this article does not qualify as an investment recommendation.

Marketing Communication.

3 minute read