An Altered Investment Backdrop for U.S. Growth Equities

-

Jeremiah Buckley, CFA

Jeremiah Buckley, CFA

Portfolio Manager

Portfolio Manager Jeremiah Buckley explains how higher rates and persistent inflation will impact U.S. growth equities.

KEY TAKEAWAYS

- A sea change in monetary policy prompted by stubborn inflation has significantly altered a long-standing, benign investment backdrop for growth stocks.

- We think that we are now close to a peak in inflation and that interest rates can begin to stabilize. If so, we believe that multiple compression is largely behind us and equities can begin to perform in-line with earnings growth again.

- Elevated volatility can provide opportunity as some of the current macro headwinds abate and we return to a more stable period of economic growth.

KEY TAKEAWAYS

- A sea change in monetary policy prompted by stubborn inflation has significantly altered a long-standing, benign investment backdrop for growth stocks.

- We think that we are now close to a peak in inflation and that interest rates can begin to stabilize. If so, we believe that multiple compression is largely behind us and equities can begin to perform in-line with earnings growth again.

- Elevated volatility can provide opportunity as some of the current macro headwinds abate and we return to a more stable period of economic growth.

Investors began to digest the Federal Reserve’s (Fed) intentions to tighten monetary policy in November of last year, amid a market that had been climbing steadily since early in the pandemic. In the months since, we have seen persistently high inflation, and the central bank has now emphatically pivoted from extraordinarily supportive policy to aggressive tightening. Today, we are faced with a fundamentally changed environment ‒ higher rates and lingering inflation present a stark contrast to the low-rate, low-inflation environment of the previous decade ‒ forcing investors to reconsider equity growth prospects and valuations.

U.S. equity markets have sunk close to bear market territory, with the S&P 500® Index recently off nearly 18% from its record high on the first trading day of 2022 (as of 18 May 2022). Inflation readings this year have been higher and more durable than many expected. Until inflation moderates and interest rates can stabilize, volatility is likely to continue as the impacts to economic growth ‒ both short and long term ‒ remain uncertain.

The outlook for inflation

Some signals at both the macro and company levels lead us to believe we are close to a peak in inflation. Strong demand for goods ‒ supported by robust consumer balance sheets ‒ is moderating as growth pulled forward during the pandemic slows and government stimulus wanes. Higher financing costs due to rising rates and a shift back to spending on services, which has been limited due to the pandemic, are also pushing down demand for goods.

On the supply side, labor force participation, although slightly lower in April, has generally trended toward pre-pandemic levels, easing some pressure in an historically tight labor market.

Retailers have rebuilt inventory levels, leading to less product scarcity, which will likely cause some discounting and lower prices in some categories. The supply chain for semiconductors, which have been a problematic segment of the market, is slowly improving, and we expect more material improvement in 2023 as new capacity is added across the industry. We are also seeing transportation costs moderate as capacity catches up and demand levels off. Despite these positive developments, commodity prices continue to rise, a situation that has only been worsened by the war in Ukraine and that is not being offset by increased production elsewhere.

Near-term equity impacts

If our base case of peak inflation and more stable interest rates proves correct, we believe multiple compression is largely behind us and that equities can start to perform in line with earnings growth again. Given a volatile environment simultaneously impacted by the pandemic, shifting fiscal and monetary policy and geopolitical conflict, we recognize that it has been difficult for companies to plan effectively. However, we believe businesses can adjust and will seek to optimize their cost structures and investments to ultimately increase productivity and margins.

Long-term equity impacts

In the longer term, we believe that innovation will continue to spur earnings growth and lead to capital appreciation in equities. Products and services such as cloud computing and software that are driving productivity gains and tend to have a deflationary effect in the economy will create value for customers and the companies that provide them. As the need grows to process data for technologies such as artificial intelligence, semiconductor demand will remain high. Semiconductors will also be vital as they proliferate across the economy and in our daily lives ‒ in cars, machinery, devices and other applications. Continued innovation in the health care sector can likewise create value by improving patients’ lives and lowering the overall costs of the health care system. So, while a structurally higher interest rate environment will make it necessary to re-examine allocations, we believe that long-term investment themes will remain instrumental to growth in equities.

Digging deeper into value vs. growth

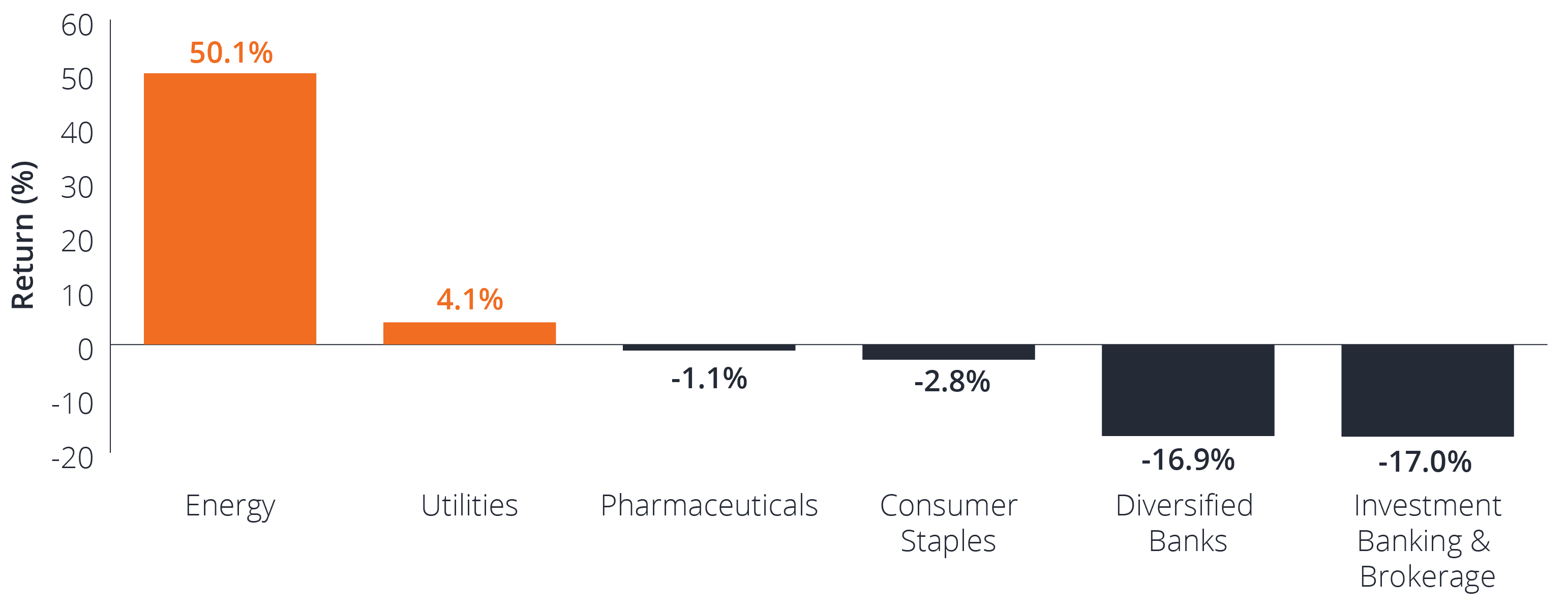

Rather than view the investment world from a broad value versus growth perspective, we prefer to drill down deeper into sectors, industries and companies to determine that outlook. Some of the sectors and industries that tend to be more heavily weighted in value indices include energy, banks, consumer staples, pharmaceuticals and utilities.

The energy sector has been the clear winner this year as prices of oil and natural gas have skyrocketed. On the other hand, while banks have been the worst-performing sector of this group, we have seen improvement in loan demand and believe the current interest rate environment should continue to bolster net interest margins. Capital market exposure has dragged down performance for many banks recently, but it is our belief that this will eventually stabilize.

Consumer staples and pharmaceuticals tend to perform well in uncertain and inflationary times like the present. However, these sectors have seen significant multiple expansion as investors have exited risky investments and bought into more defensive areas of the market. Rising commodity costs may eventually pressure these companies’ ability to continue raising prices as consumers will choose to trade down, and there continues to be concern about government-influenced price deflation in pharmaceuticals.

In the past, commodity industries were generally not attractive to us due to the low returns on capital these companies were earning. However, greater restrictions on supply growth and better capital discipline by company management have changed the outlook to some extent. While we don’t believe it is prudent to chase short-term supply chain disruptions, the long-term supply and demand environment may now be conducive to higher returns on capital.

Opportunity in volatility

While markets can be uncomfortable and confusing at times such as these, elevated volatility can also create opportunity. We are now seeing attractive entry points in high-quality companies generating cash flows with attractive long-term secular growth. In our view, this environment reinforces the importance of focusing on equities with robust balance sheets and consistent cash flows that can reinvest during uncertain periods. We think these companies can emerge in a position of strength and accelerate market share gains as some of the current macro headwinds abate and we return to a more stable period of economic growth.

STAY BALANCED DURING TURBULENT TIMES

Flexible. Resilient. Dynamic

Find out more