Key takeaways:

- Trilogue negotiations between the European Commission, European Parliament, and European Council on securitisation reform have seen policymakers converge on measures that could help revive issuance and unlock significant new lending capacity.

- Reforms that improve global market access, broaden investor demand, and align regulation more closely with underlying risk could support market growth. Conversely, disproportionate investor sanctions, restrictive due diligence requirements, and regulatory duplication will risk discouraging participation and limiting the effectiveness of the reforms.

- As trilogue negotiations progress, policymakers should focus on proportionate supervision, outcomes-based due diligence, meaningful market access to non-EU issuers, modernised UCITS concentration rules, and risk-sensitive capital treatment. Achieving the right balance will be critical to outcomes.

Europe’s securitisation market is at a turning point

Once central to the functioning of European credit markets, securitisation has never fully recovered from the Global Financial Crisis. While European securitisations proved more resilient than their US counterparts during the crisis, the regulatory response in Europe was nonetheless extensive. Over the past decade, layers of rules covering transparency, due diligence, risk retention and reporting have created one of the most prescriptive regulatory regimes in global capital markets. Although intended to restore confidence, this framework has also constrained market growth and participation. As a result, European securitised issuance has halved from pre-crisis levels, averaging just €250 billion per year – roughly one-seventh of the US market[1], where securitisation has continued to expand and remains a core source of credit funding.

That is now set to change. The European Commission proposed its Securitisation Regulation Review in June 2025[2]; the European Council agreed its position in December that year[3]; and the European Parliament’s Economic and Monetary Affairs (ECON) Committee finalised its stance in May 2026[4]. Trilogue negotiations between these parties are now underway – and the stakes are high. If revived to pre-crisis levels, Europe’s securitisation market could unlock €130-320 billion in new lending each year, amounting to more than €1 trillion over five years[5]. Thus, connecting long-term investors with real economy lending – mortgages, consumer credit, small and medium size enterprise (SME) finance – that is not otherwise readily accessible through public markets.

Janus Henderson welcomes this direction of travel. However, as a global asset manager and a longstanding, committed, and active investor in securitised credit, we believe the current proposals risk falling short of their objectives. While most issues reflect areas where the new securitisation framework could have been better calibrated, one element stands out as fundamentally different – both in scale and in consequence.

“If revived to pre-crisis levels, Europe’s securitisation market could unlock €130-320 billion in new lending each year…connecting long-term investors with real economy lending – mortgages, consumer credit, SME finance – that is not otherwise readily accessible through public markets.”

Investor sanctions – a critical design risk?

The proposed sanctions regime for institutional investors that fail to comply with mandatory due diligence requirements represents a key concern within the current package. Unlike other aspects of the reform, we believe the sanctions proposal introduces risks that could, if not carefully addressed, undermine the broader objectives of the reform.

We support the Council’s approach to remove such investor-specific sanctions under Article 32 entirely. Institutional investors are already subject to well-established enforcement regimes under AIFMD, UCITS, and Solvency II across all asset classes. The Council’s position avoids unnecessary duplication with these existing supervisory regimes while better supporting the overarching aim of rebuilding investor participation in EU securitisation markets. If investor sanctions are retained, we believe they should be proportionate and aligned with the way comparable EU rules are applied elsewhere.

While we welcome the Parliament’s efforts to reduce the level of sanctions from those originally proposed by the Commission, we remain concerned that the retention of investor sanctions at up to 50% of the value of the relevant securitisation position may not be proportionate.[6] A sanction of this scale would be difficult to justify on proportionality grounds and could single out securitisation for more punitive treatment compared to other asset classes, distorting asset allocation.

Introducing a parallel, securitisation-specific sanctions regime, particularly at the level envisaged by the Parliament, also risks deterring investor participation. In our view, this would materially increase downside risk relative to other asset classes, at precisely the moment policymakers are seeking to rebuild demand. It would also create regulatory duplication by layering a second enforcement framework onto existing regimes without adding meaningful supervisory value elsewhere in the capital markets.

This concern is not theoretical. The European Central Bank believes there are proportionality issues[7] with the current regime. This indicates a clear risk that the sanctions framework, if not adjusted, could negatively affect market functioning rather than simply requiring refinement.

Due diligence and global market access – improvement but incomplete

The due diligence regime[8] under the new Securitisation Regulation remains format-driven rather than substance-driven. EU investors are required to obtain disclosures in EU-specific templates, even for third-country (issued outside the EU) securitisations, even though most of these non-EU issuers provide equivalent information using their own established formats. Due diligence is one of the requirements that a securitisation must satisfy to be eligible for investment by EU institutional investors.

Another is compliance with the SECR risk retention rules, which require the originator, sponsor or original lender to retain an ongoing material net economic interest of at least 5% in the securitisation[9], ensuring alignment of interests between issuers and investors through a “skin in the game” requirement.

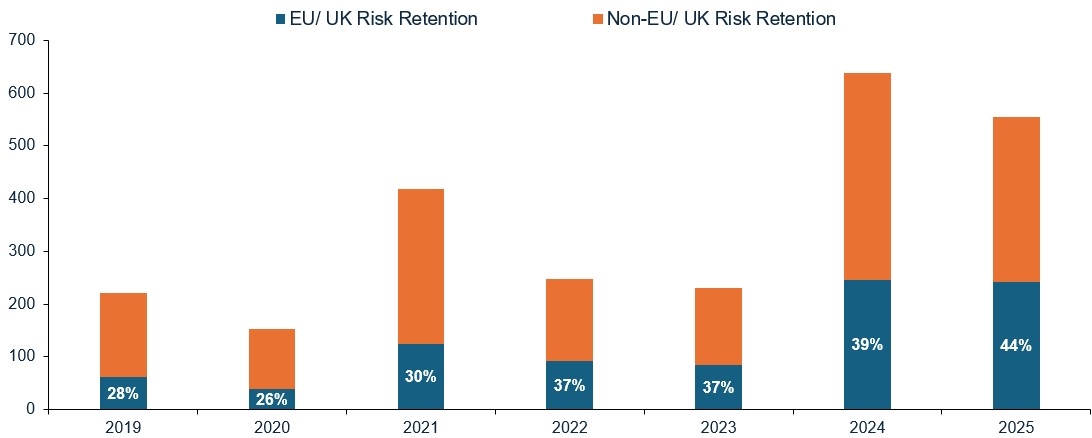

EU investors have an accessible €1 trillion global securitised opportunity set of eligible investments, where eligible issuance is growing, as shown by the chart below. Nevertheless, they are still effectively unable to access trillions of debt[10], reducing diversification potential which is a key advantage of securitised investments. No other major jurisdiction – the US, UK, Canada or Australia – imposes comparable restrictions.

EU/ UK risk retention eligible issuance is increasing

Source: Janus Henderson Investors as at 30 September 2025.

Note: Not all US issuance that is EU/UK risk retention eligible is fully EU/ UK Securitisation Regulation compliant as other articles of the regulation often not met.

Both the Council and Parliament have rightly recognised this barrier and removed the EU template requirement for non-EU issuers. However, the Council’s replacement, an “in substance” test, still requires investors to verify that the same due diligence disclosure package[11] is available. Therefore, in our view, this remains too prescriptive to meaningfully improve global market access for European securitised investors. The Parliament position goes even further, requiring EU investors to verify that third-country disclosures are “substantively equivalent” to EU transparency standards[12]. This is a more workable formulation, but without detailed technical standards to define what “substantively equivalent” means in practice, it risks shifting the compliance burden, and associated legal risk, onto EU investors.

We urge co-legislators to adopt a genuinely outcomes-based approach to due diligence, focused on investor safeguards and market integrity, rather than prescribing the format or source of disclosure. This is consistent with the direction recommended by the European Supervisory Authorities’ joint report released in March last year[13] and the approach already implemented in the UK[14].

UCITS demand – a missed opportunity

UCITS funds remain an under-utilised source of securitisation demand, largely due to the 10% single-issuer concentration limit, a rule that predates modern securitisation and is not aligned with an inherently diversified asset class. We welcome the Council’s proposal to raise this limit from 10% to 50% for a single public securitisation, which could unlock €100-150bn in immediate demand and €20bn-€30bn in annual demand thereafter[15]. This level of ambition, in our view, should be preserved through trilogue.

Definitions and capital treatment – scope for refinement

We welcome the Council’s decision to remove the Commission’s proposed expansion of the definition of “public” securitisation. While the Parliament has also sought to refine the Commission’s approach, its proposed inclusion of actively managed transactions within the public securitisation framework risks capturing transactions that are private in nature and not intended for broad market distribution.

On capital treatment, the disparity is stark: US insurers allocate approximately 25% of their balance sheets to securitisations compared with just 1.6% for European insurers[16]. This gap appears to be driven by Solvency II capital charges rather than underlying risk. Maintaining the Commission’s ambition on capital reform through trilogue will therefore be important.

It is also notable that the UK’s direction of travel differs, with the Financial Conduct Authority and Prudential Regulation Authority moving towards an outcomes-based framework that seeks to safeguard investors without prescribing rigid processes. The EU need not replicate this model, but the contrast underscores the importance of ensuring Europe’s approach remains internationally competitive.

Looking ahead

With trilogue negotiations now underway under the Irish Presidency, the coming months represent a genuine opportunity. If revitalised to pre-crisis levels, European securitisation could generate over a trillion in additional private financing over five years[5]. This is capital that Europe needs to support its green transition, digital infrastructure, and broader economic resilience, while helping channel long-term investor capital into lending to households and businesses. Realising that potential will require reforms that address demand as well as supply. In our view, this means:

- Addressing sanctions risk – avoiding a duplicative and disproportionate regime that could deter investor participation.

- Principles-based due diligence – amending due diligence requirements to focus on the substance of information, enabling access to global securitised markets.

- Meaningful third-country access – treating non-EU instruments on a comparable basis to EU-originated securitisations where robust standards are met.

- Modernised UCITS rules – removing or significantly increasing the 10% issuer limit for securitisations.

- Clear public-private definitions – ensuring genuinely private transactions are not captured by a public disclosure framework.

- Risk-sensitive capital treatment – aligning Capital Requirement Regulations or CRR (applicable to banks and investment firms) and Solvency II (affecting insurers) charges more closely with observed default performance.

Our teams at Janus Henderson remain committed to constructive engagement with policymakers as these negotiations progress. A well-calibrated framework, particularly one that avoids unintended consequences in critical areas such as sanctions, can unlock significant economic value for Europe while maintaining strong standards for investors in securitisation. The opportunity is clear; it is now a question of calibration and ambition driving action.

Footnotes

[1] Source: Bloomberg, Citigroup, Dealogic, Deutsche Bank, JP Morgan, Bank of America, NatWest Markets, Thomson Reuters, UniCredit, AFME & SIFMA, as at the end of Q4 2025, 21 January 2026.

[2] Source: European Commission, Proposal for a Regulation amending Regulation (EU) 2017/2402 and Regulation (EU) No 575/2013, COM(2025) 826 final, 17 June 2025.

[3] Source: Council of the European Union, General Approach on the Securitisation Regulation Review, 19 December 2025.

[4] Source: European Parliament, ECON Committee vote on the Securitisation Regulation Review, 5–6 May 2026; endorsed at plenary, 21 May 2026.[5] Source: European Capital Markets Institute, April 2026.

[6] Source: European Parliament, report on the proposal for a regulation of the European Parliament and of the Council amending Regulation (EU) 2017/2402 of the European Parliament and of the Council of 12 December 2017, 8 May 2026.

[7] Source: ECB’s November 2025 Opinion, 11 November 2025.

[8] As denoted in Article 5 under the new Securitisation Regulation or SECR framework.

[9] As denoted in Article 6 under the new Securitisation Regulation or SECR framework.

[10] Source: Janus Henderson Investors estimates using data from AFME and SIGMA, as at Q1 2025.

[11]Source: European Council, 19 December 2025. Under Article 7(1), which includes transaction documents, collateral data, investor reports and material event notifications.

[12] Source: European Parliament, 30 April 2026.

[13] Source: EBA, ESMA and EIOPA, Joint Committee Report on the Functioning of the Securitisation Regulation (Article 44), 31 March 2025.

[14] Source: FCA, Consultation Paper CP26/6, ‘Rules for Reforming the UK Securitisation Framework’, 17 February 2026; PRA, Consultation Paper CP2/26, 17 February 2026.

[15] Source: Structured Finance Association (SFA), Position Paper on EU Securitisation Reform, January 2026.

[16] Source: AFME, US NAIC Capital Markets Bureau Special Reports and EIOPA Insurance Statistics, 2023.