Key takeaways:

- Shifting opportunity set creates selective potential upside. A challenging macro backdrop masks an evolving landscape, where changing capital allocation, sector dynamics and policy direction are creating new pockets of underappreciated opportunity.

- Policy-backed investment is driving selective opportunities. Energy security, defence, renewables, electrification and industrial materials have benefited from sustained political support and an improved capital spending cycle.

- AI and infrastructure highlight Europe’s underappreciated strengths. Rather than headline tech, Europe stands to gain through enabling technologies – power, grids, automation and materials – where efficiency and scale are increasingly rewarded.

European stock markets are navigating a more uncertain backdrop, but beneath the surface, we see powerful structural trends creating fresh opportunities for investors who are willing to look beyond the headlines.

At the time of writing in mid-May, news flow around the conflict in the Middle East remains highly volatile, making the market impact difficult to assess with any degree of accuracy. The eventual duration of the conflict will determine to what extent the generally positive economic signals observed early in the year on both sides of the Atlantic can reassert themselves, or whether a narrative of sustained higher oil prices, a return of inflation and supply chain disruptions will take over.

Meanwhile, central banks remain cautious across the bloc, with the European Central Bank (ECB) opting to keep monetary policy restrictive, holding rates steady while leaving the door open to further tightening.

The more constructive view

While the near-term macro picture may appear challenging, we believe it obscures a more constructive story for European equities. We are seeing the most significant reform plans in years, focused on electrification and grid modernisation, a more co-ordinated industrial policy, and efforts to mobilise the huge, untapped investment potential of EU household savings. Factors like securitisation market reform, a tougher stance on imports, progress in reducing compliance burdens, and a more open stance on technology development and bureaucracy-heavy areas like carbon emissions, are opening up avenues for investment.

While the near-term ‘macro’ picture may look uncomfortable, we think it is important to look through the potential cyclical softness, to focus instead on a set of powerful structural drivers that are reshaping the opportunity set for European equities:

1. Strategic competition for critical resources: From rare earths to energy, global supply is tight after years of underinvestment. Recent events have forced investors to think harder about the strategic value of energy, not just oil and gas, but where it comes from and how secure that supply is.

Companies linked to commodities, and the equipment needed to extract or process them, are entering what could be a long upswing. The prospects for a strong ‘catch-up’ investment cycle have ramifications for the whole supply chain, with significant potential for pricing power to reappear where capacity is tight. Both in terms of energy and mining firms and the areas upstream and downstream that are well placed to benefit from investment.

2. Areas of rising policy support: Renewables are a clear priority as the region seeks to reduce reliance on imported fossil fuels. A second energy shock within a handful of years has reinforced a political reality: Europe is heavily reliant on imported fossil fuels, and energy security is now tightly linked to economic security. The objective is not only decarbonisation; it is also reducing exposure to imported energy and improving stability in the cost base for households and industry.

Policy support is also broadening to selected industries that form the building blocks of the economy, such as industrial materials (steel, chemicals, etc) and manufacturing. In a world of more assertive trade policy and tighter supply chains, the idea of letting strategic capacity drift offshore is being challenged. More directly, we expect defence stocks to continue benefiting from renewed (and long-term) focus on the security needs of the bloc, reducing reliance on external providers.

The banking sector initially benefited from renewed policy focus following the Draghi report in late 2024, which catalysed a range of European Commission initiatives aimed at strengthening capital markets and financial integration. However, momentum has moderated more recently, with many proposals becoming subject to the complexities of the EU policy process, where alignment between institutions, regulators and stakeholders can be protracted. We continue to believe the direction of travel remains encouraging nonetheless.

Meanwhile, defence remains an area of structural support given the bloc’s evolving security priorities. However, while committed spending is likely to be delivered, there is an ongoing debate around the direction of investment – particularly the balance between traditional systems and newer asymmetric capabilities such as drones and long-range technologies.

3. A push for innovation: Europe’s structural economic challenge has often been framed as a lack of innovation. Investment in research has been sluggish, and too much spending has historically sat in ‘mid-tech’ industries that were yesterday’s growth engines but are now nearer to cash-cow status.

But the idea that ‘Europe lacks innovation’ is also an oversimplification. The opportunity is increasingly found in pockets of global leadership; businesses enabling the technologies that power modern economies. This includes advanced computing, industrial automation, electrification, and the infrastructure required to move power and data efficiently.

AI: The unavoidable theme reshaping market attention

AI (artificial intelligence) tools are rapidly reducing the need for large sales, general and administrative functions, prompting investors to pivot toward leaner operators: companies that can deliver output faster with fewer layers and lower overheads. The accelerating performance gap since the second half of 2025 suggests that markets are already reassessing which companies deserve premium valuations, rewarding those seen as capable of embedding AI into workflows, productivity, and operating leverage.

Exhibit 1: Markets are rewarding efficiency in the age of AI

Source: Societe Generale, Janus Henderson Investors, as at 20 April 2026. Note: SG&A=sales, general and administrative. Rebased to 100 on 31 December 2024. Universe of stocks analysed is within the S&P 500 Index. Past performance does not predict future returns.

AI is not just changing how investors perceive businesses. The scalability demands of AI require a huge amount of physical infrastructure, materials and investment, across computing capacity, networking, power generation, grid investment, and the specialist construction and equipment that brings it all to life. These are areas where parts of the European market have meaningful exposure.

Why Europe can still offer a compelling mix

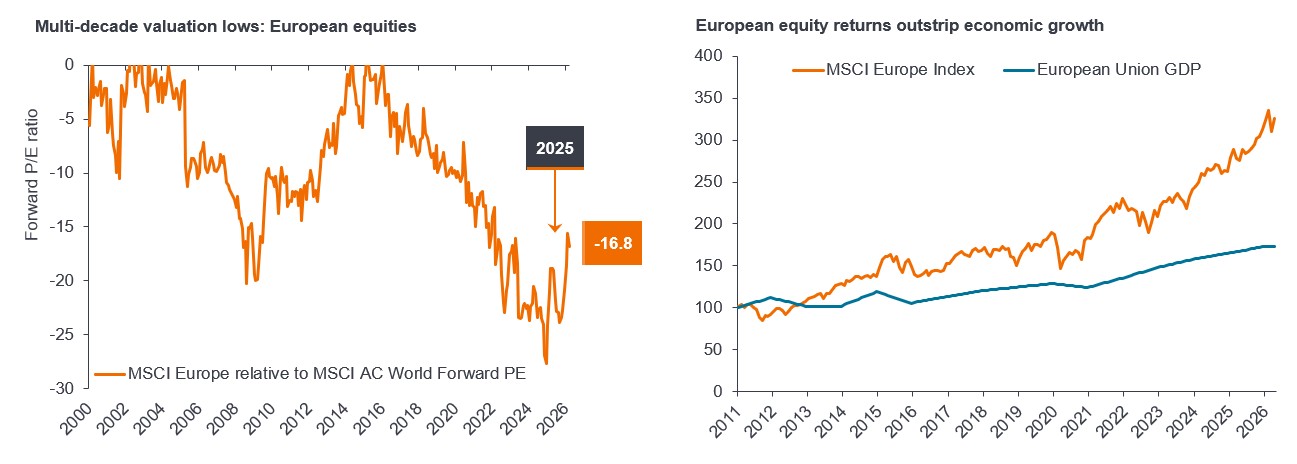

The argument in favour of European equities is one that combines exposure to global structural forces with factors related to domestic improvement as reforms and investment momentum continue. Globally positioned businesses that can compound growth through structural demand (even if European growth is uninspiring), with the potential for a domestic revival narrative, with incremental progress will compound the impact.

Exhibit 2: European equities ≠ European GDP

Source: (LHS) Bloomberg consensus forecasts, Janus Henderson Investors analysis, as at 31 March 2026 (European Equities at Multi-Decade Valuation Lows). Note there is no guarantee that past trends will continue, or forecasts will be realised. Source: (RHS) Bloomberg, Eurostat, Janus Henderson Investors analysis, as at 31 March 2026 (European Equity Returns Outstrip Economic Growth). Note: MSCI Europe EUR Net Total Return Index and European Union Gross Domestic Product (GDP) rebased to 100 on 01 January 2010. From 2026, European Union GDP is an estimate using ECB projections. Past performance does not predict future returns.

None of this removes the risks. Energy-driven inflation, higher-for-longer rates, or an escalation in geopolitical tensions are all sources of potential uncertainty. But the argument for Europe is more about recognising where structural change is happening, where capital spending cycles are showing momentum, and where policy is shifting to support innovation. Europe’s opportunity set may be more resilient, and more diverse, than the headlines suggest.

Asset-backed securities (ABS): A financial security that is backed (or collateralised) with existing assets (such as loans, credit card debts, or leases), usually ones that generate income or cash flow over time.

Central bank: An institution responsible for managing a country or region’s currency, money supply and interest rates, typically with the aim of maintaining price stability and supporting economic growth.

Commodities: Raw materials or primary agricultural products that can be bought and sold, such as oil, gas, metals or foodstuffs. Commodities are often used as inputs in the production of other goods and services.

Equities: Shares representing ownership in a company. Equity investors participate in a company’s profits and losses and may receive dividends as well as capital growth if the share price rises.

Inflation: The rate at which the general level of prices for goods and services rises over time, reducing the purchasing power of money.

Interest rates: The cost of borrowing money or the return earned on savings, usually expressed as a percentage. Interest rates are a key tool used by central banks to influence economic activity and inflation.

Forward PE: A popular ratio used to value a company’s shares compared to other stocks or a benchmark index. It is calculated by dividing the current share price by its future earnings (usually for the following 12 months) per share.

The MSCI All Country World Index (ACWI) is a global equity index that measures the performance of both developed and emerging markets. MSCI Europe EUR Net Total Return Index captures large and mid-cap representation across developed markets countries in Europe. European Union Gross Domestic Product Index is a non-tradeable, time series tracking the level or growth of economic output for the European Union.

Valuation: A measure of how much a company, asset, or market is worth, often assessed using metrics such as price-to-earnings ratios, cash flows, or asset values. Valuations help investors judge whether an investment appears expensive or cheap.