Key takeaways:

- Artificial intelligence is a multi‑year infrastructure and capital formation supercycle that is reshaping both the economy and the foundations of sustainable investing.

- AI’s near‑term carbon intensity creates hard sustainability trade‑offs, but efficiency gains and productivity multipliers are likely to dominate over time.

- AI is challenging mental models around the quality of business fundamentals and the durability of returns for many digital and human capital dependent businesses.

AI: The most disruptive force – and the largest opportunity – we have ever encountered

The rise of artificial intelligence (AI) is simultaneously one of the most disruptive forces we have seen and one of the most compelling structural investment opportunities we have encountered. AI is not just changing individual business models; it is reshaping the economy itself and, in turn, the very framework through which we evaluate what constitutes a sustainable, durable business.

For investors, the core questions are deceptively simple: how large and how long will the AI investment cycle be, and what does it mean for businesses, society, the global economy and the environment? Our conviction is that this is not a fleeting technology cycle. AI represents a multi‑year, structural capital formation wave of unprecedented scale, and everything we have observed thus far in 2026 has reinforced that view.

The AI investment supercycle: Scale, duration and conviction

We’re only in year two of a ‘massive ten-year cycle’ of rapid AI advancements and infrastructure build-out.

– Lisa Su, CEO AMD at the Axios AI+ Summit

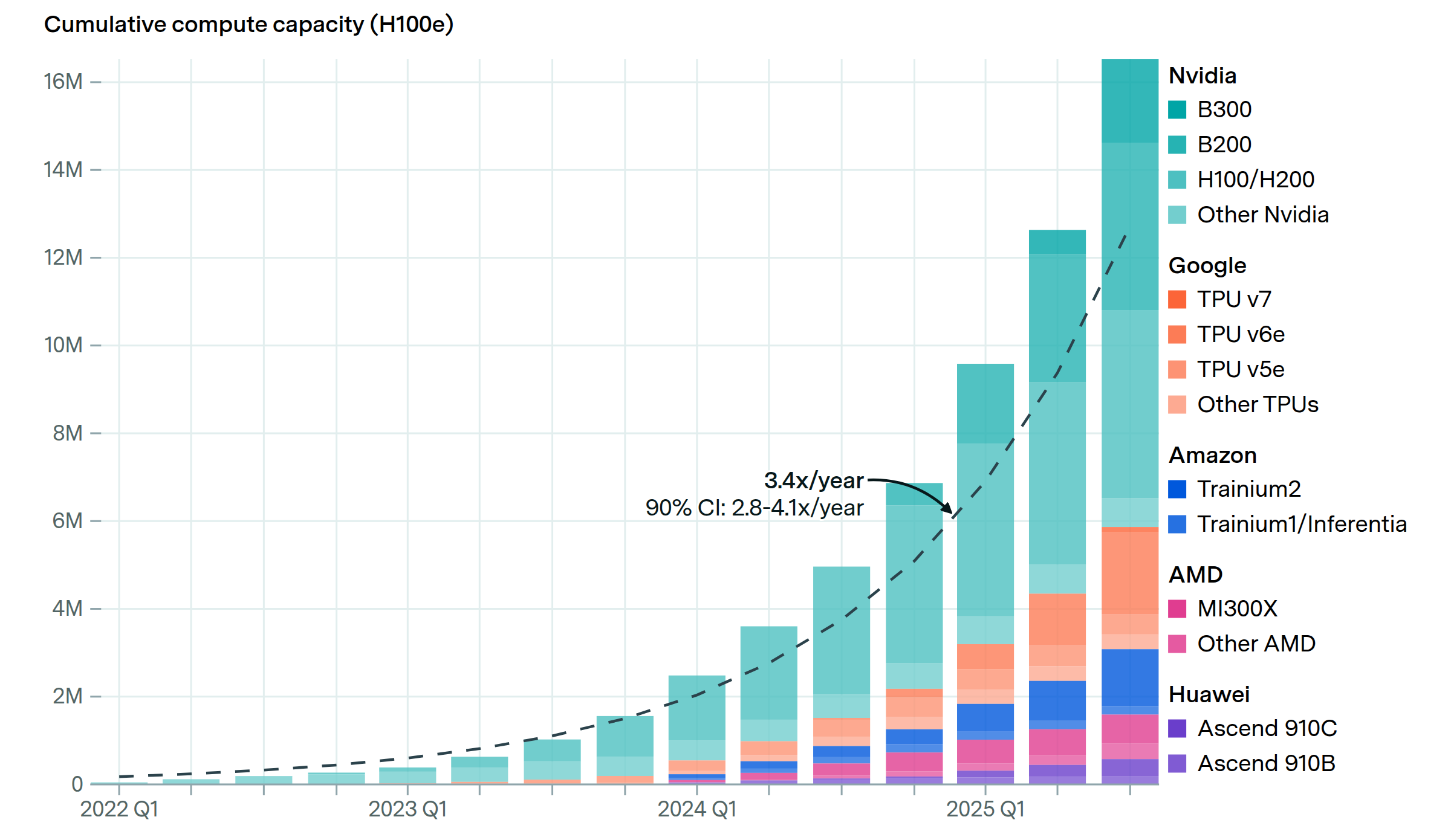

Recent industry dialogue has added to our conviction that the AI investment cycle is still in its early innings. At the Morgan Stanley TMT Conference (March), the message from across the AI ecosystem was strikingly consistent: expectations of a near‑term peak or fade in AI investment are misplaced. MS’s thematics team is projecting a 230% compound annual growth rate (CAGR) in compute capacity (Figure 1) between 2025 and 2030 (measured in teraflops) – with Alphabet’s internal forecasts running 3x higher.1

Figure 1: Global AI computing capacity is doubling every 7 months

Source: Josh You et al. (2026), “Global AI computing capacity is doubling every 7 months”. Published online at epoch.ai. Retrieved from ‘https://epoch.ai/data-insights/ai-chip-production’ [online resource]. Accessed 29 Apr 2026. References made to individual securities do not constitute a recommendation to buy, sell or hold any security, investment strategy or market sector, and should not be assumed to be profitable. Janus Henderson Investors, its affiliated advisor, or its employees, may have a position in the securities mentioned. There is no guarantee that past trends will continue, or forecasts will be realised. Past performance does not predict future returns.

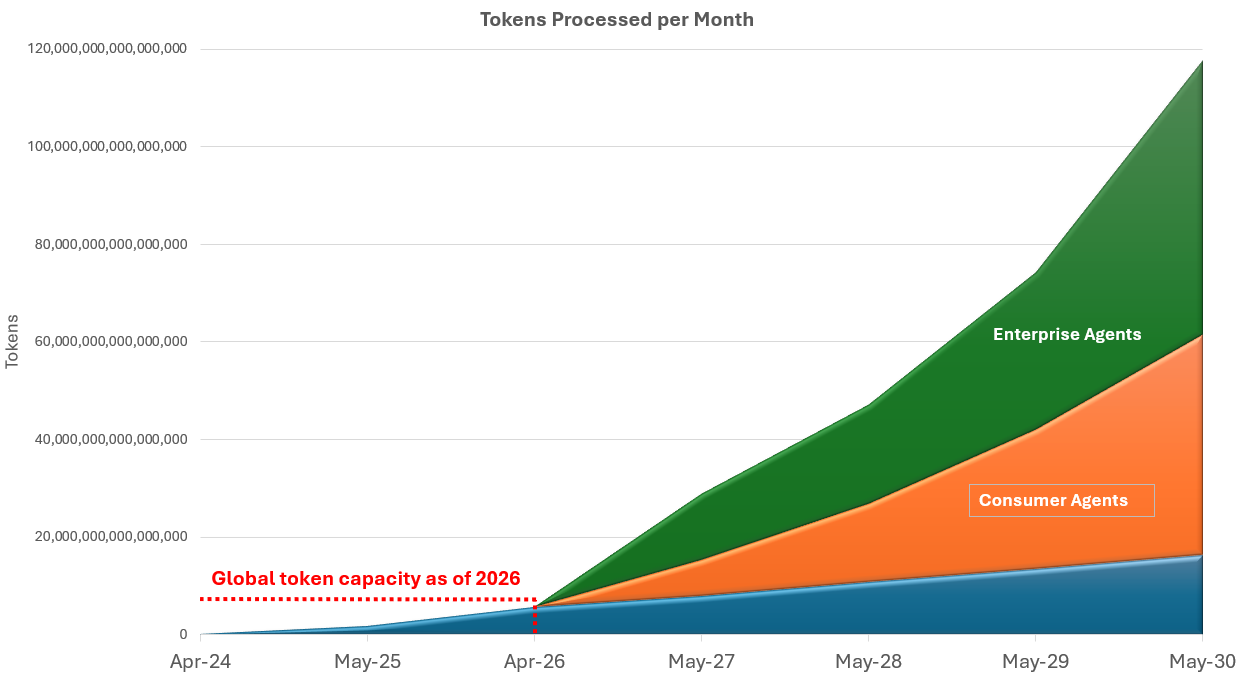

Real‑world usage data is even more telling. Weekly token consumption across the AI ecosystem has increased more than 3,800% over the past year2, and corporate willingness to pay is clear, as evidenced by Anthropic’s rapidly growing revenues which have increased from under US$10 billion at the end of 2025 to over US$30bn by early April 2026.3 Further, agentic AI is driving a significant increase in token consumption of 24x or 120 quadrillion tokens per month by 2030 (Figure 3).4 Research by Goldman Sachs suggests that enterprise agents will be the largest token multiplier, lifting token consumption 55x by 2040, while consumer agents will broaden usage away from episodic chats to utility beyond traditional search, driving 12x token consumption by 2030.5

Put simply, this cycle has duration. Further, physical constraints – power availability, grid capacity, manufacturing lead times and supply‑chain bottlenecks – are not dampening demand; they are extending it. Rather than a fast, frictionless digital adoption curve, AI is unfolding as a capital‑intensive industrial expansion that will likely run for many years.

Figure 2: By 2030 consumer and enterprise agents could push token consumption 24x above today’s estimated global capacity

Source: Goldman Sachs Global Investment Research, as at 5 May 2026. Forecasts may vary and are not guaranteed.

Intelligence factories: redefining economic infrastructure

The CEO of Nvidia, Jensen Huang, believes many people are wrongly thinking about AI datacentres as cost centres – as big buildings that simply store data. Rather they ought to be thought of as “intelligence factories” where their output is not data storage, but tokens – units of productive intelligence that drive economic value. From that perspective, AI becomes a horizontal enabling layer, analogous to electricity. Just as electricity, when it was first deployed industrially, did not replace a single industry – it transformed every industry by making energy universally available, abundant and cheap – AI is doing the same for intelligence. Every sector, every workflow, every decision process, therefore, can and will be augmented or transformed by making intelligence abundant and scalable.

The implication is profound. If every economy and every business require intelligence at scale, then AI datacentres become critical national and commercial infrastructure. This is why we believe AI datacentres represent one of the largest global infrastructure build‑outs in modern history, with estimates suggesting global spending could reach US$7 trillion by 2030.6

Power, efficiency and the new competitive frontier

Unlike past digital revolutions, this one is tightly bound to the physical world. AI factories are limited not by code, but by power. Land, grid connection and energy availability are the binding constraints, and within that envelope, competitive advantage is determined by efficiency: how many tokens can be produced per unit of energy consumed.

“Your data centre, it used to be a data centre for files. It’s now a factory to generate tokens. Your factory is limited no matter what. Everybody is looking for land, power and shell. Once you build it, you are power limited. Within that power-limited infrastructure, you better make for darn sure that your inference — because tokens are your new commodity — that the architecture is as optimised as you can.”

– Jensen Huang, CEO Nvidia at the 2026 Nvidia GPU Technology Conference Keynote

For decades, the driving question of the semiconductor industry was: how many transistors can we fit on a chip? Today, the defining metric of the AI era is fundamentally different: how many tokens can we produce for a given unit of energy? Just as a physical factory is limited by its energy supply, its throughput per unit of energy, and the bottlenecks in its production line, so too is an AI data centre. The metric that determines competitive advantage is not raw compute — it is compute per watt. And the limiting constraint, as NVIDIA’s infrastructure team confirmed, is not physical space. It is power.

At NVIDIA’s GTC 2026 keynote Jensen Huang revealed the pace at which Nvidia is improving the power efficiency of its AI systems. NVIDIA’s Grace Blackwell NVL 72 system delivered 35x the inference performance per watt compared to the previous generation Hopper H200 – in a single product generation. For context, Moore’s Law at its peak would have delivered perhaps 1.5x improvement per generation. When the independent benchmarking firm SemiAnalysis published its analysis, it concluded the actual figure was closer to 50x – and accused Jensen of sandbagging.

Jensen’s response: “He’s not wrong.”

The implication is stark. In a world where every data centre operator is power-constrained — where land, power and shell are the binding constraints on AI factory construction — the operator who can generate 50x more tokens from the same power envelope generates 50x more revenue. The token factory analogy is therefore not hyperbole. It is the correct industrial and economic framework through which to understand AI infrastructure investment. An AI data centre is a factory. Its output is tokens. Its raw material inputs are electricity, memory bandwidth, storage and cooling capacity. Its limiting constraint is power. And its competitive moat is efficiency per unit of energy consumed.

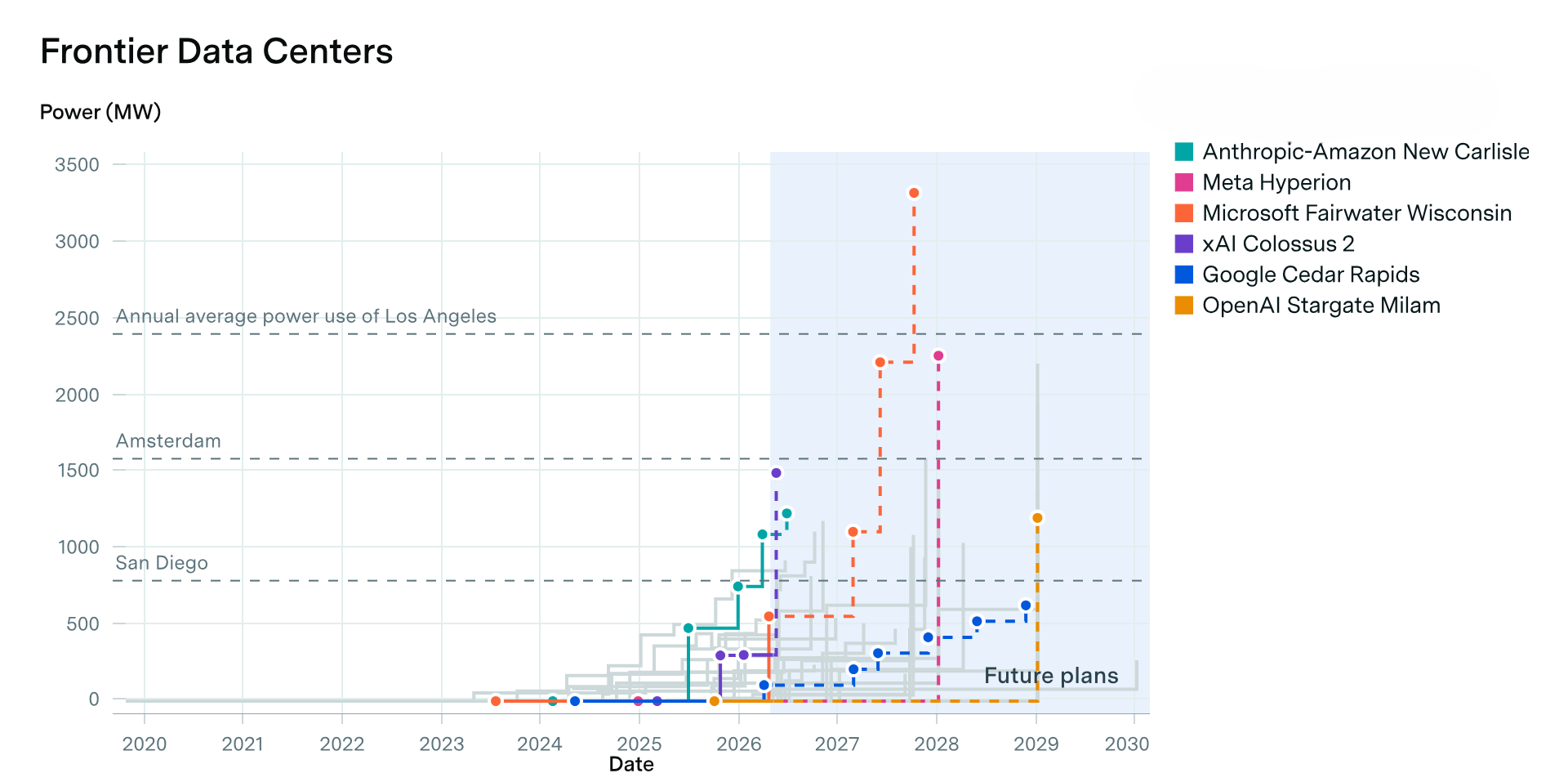

Figure 3: AI data centres, using satellite and permit data to track power use

Source: Epoch AI, ‘Frontier Data Centers’. Published online at epoch.ai. Retrieved from ‘https://epoch.ai/data/data-centers’ [online resource]. Accessed 30 Apr 2026.

Investing in bottlenecks – and reducing carbon intensity

Given our conviction in both the scale and the duration of the AI investment cycle, we have continued to focus on areas of the AI value chain where capital intensity, physical constraints and bottlenecks are most pronounced. Our focus has been on critical infrastructure and enabling technologies that underpin the AI ecosystem, rather than on downstream applications alone.

At the same time, we are highly selective, prioritising businesses that improve the efficiency and carbon intensity of AI. Allocating capital towards technologies that reduce energy consumption, improve power utilisation and enhance system‑level efficiency is central to how we approach sustainable investing in this new era.

We favour areas like core computing infrastructure and advanced manufacturing, memory and bandwidth solutions, and the storage technologies required to manage the rapid accumulation of AI‑generated data. Key too are power and electrical infrastructure, recognising that efficient power conversion, grid connectivity and resilience are now binding constraints on AI deployment. Thermal management and energy storage have become equally important, as rising compute density places unprecedented demands on cooling systems and reliable, dispatchable power.

Taken together, these areas represent the physical backbone of the AI economy. They are where incremental improvements in efficiency can unlock disproportionate gains in productivity, lower system‑wide carbon intensity over time, and create durable competitive advantages in a world increasingly defined by energy and infrastructure constraints.

The great sustainability paradox: Confronting the carbon intensity of the AI era and its impact on sustainable investing

We need to be direct and honest about the double impact AI is having on our investment universe and on the framework of sustainable investing itself.

First, the AI buildout is carbon‑intensive. Semiconductor fabricators, heavy electrical equipment, grid reinforcement and cooling systems are all asset‑heavy, energy‑hungry businesses. And AI datacentres don’t just require carbon intensive capital formation; once they are built they require continuous power often supported by grids that still rely heavily on fossil fuels.

Second, AI is challenging the notion of the durability of business economics and defensibility of economic moats. Many of the businesses most highly regarded by ESG frameworks over the past decade — capital-light, low-carbon, high-margin software and platform companies — are precisely those most exposed to AI-driven terminal value erosion. The very characteristics that made them attractive on traditional sustainability metrics (low physical footprint, low emissions, high returns on intangibles) also makes them vulnerable to a technology that competes in the domain of information and cognition. We have been, as an industry of sustainability investors, somewhat too comfortable in these businesses. We liked them because they were clean, high-quality and seemed to fit a progressive narrative about the dematerialisation of the economy. But AI is now demonstrating that their moats were not as impregnable as we assumed. The terminal value debate is real, it is active, and it is being priced into markets at speed.

Our response: Navigating carbon intensity at a systems level

Our response is what we describe as systems‑level sustainability. Rather than assessing companies solely on their standalone operational footprints, we evaluate their role in enabling a more efficient, productive and resilient economic system. We are focused on investing in companies whose products are having a positive impact on the efficiency and carbon intensity of AI.

Our approach also includes active engagement using Janus Henderson’s Climate Transition Assessment framework to ensure that decarbonisation commitments are credible and embedded in capital allocation.

We are transparent about trade‑offs. There may be periods when portfolio carbon intensity rises as exposure to physical infrastructure increases. We believe this is the right approach given the reality of where capital is flowing, where durable competitive advantages are forming, and where we can have the greatest systems-level positive impact. We will continue to report these metrics transparently, explain the composition of any movements, and demonstrate that our engagement and stewardship activities are keeping the directional trajectory on track.

Ultimately, we believe the elevated carbon intensity of the AI infrastructure build-out is transitory and will be more than offset by the productivity and efficiency multiplier that AI brings to the global economy. We believe AI will do this by accelerating materials science for clean energy, optimising the operation of power grids and industrial processes, and dramatically reducing the resource intensity of everything from drug discovery to infrastructure design. We want to invest in that future without ignoring the near-term costs of getting there.

Durability in a world of accelerated disruption

AI is not only reshaping sustainability metrics; it is accelerating disruption across business models. In response, our portfolio turnover has risen as we actively reassess durability, defensibility and terminal value assumptions. This is not indiscipline, but a rational response to a rapidly changing competitive landscape.

Alongside AI infrastructure exposure, we are increasing allocation to businesses with physical assets, network effects or defensible intellectual property (IP) that AI is more likely to reinforce than undermine – while reducing exposure where long‑term disruption risks appear underappreciated.

Conclusion: Sustainability was always physical

For the last decade, many sustainability investors — and we include ourselves in this — found an intellectually comfortable home in capital-light digital businesses. We could tell a clean story: these businesses promoted efficiency, generated high returns on minimal capital, had low carbon footprints, and seemed to embody the kind of dematerialised economic progress that a sustainable future required. We now have to ask ourselves honestly: were we, at least partially, deluding ourselves?

The rise of AI and heightened geopolitical friction is forcing a repricing of the physical world. AI, electrification and automation are real and powerful — but they are not weightless. They run on energy, metals, grids and infrastructure that have been structurally underinvested and politically constrained.

We have confidence in our positioning. We have high conviction that the AI investment cycle will last for several years. We are invested in the power, memory, cables, cooling systems and hard assets that make the AI economy possible, while maintaining a disciplined sustainability framework grounded in realism and transparency. The transition to a sustainable economy was always going to require physical capital. AI has simply accelerated the timeline, expanded the scale and clarified the stakes.

1 Source: Ars Technica, ‘Google tells employees it must double capacity every 6 months to meet AI demand’, 21 November 2025.

2 Source: Open Router

3 Source: Anthropic, ‘Anthropic expands partnership with Google and Broadcom for multiple gigawatts of next-generation compute’, 6 April 2026.

4Source: Goldman Sachs Research, ‘Decoding the Agentic Economy: The coming Inflection in AI Usage and Margins’, 5 May 2026.

5Source: Goldman Sachs Research, ‘Decoding the Agentic Economy: The coming Inflection in AI Usage and Margins’, 5 May 2026.

6Source: McKinsey, ‘The $7 trillion data center build-out: How industrials can capture their share’, 27 March 2026.

Artificial intelligence (AI): A broad category of technologies that enable machines and software to perform tasks that typically require human intelligence, such as learning, reasoning, pattern recognition and decision‑making.

Capital expenditure: Money invested to acquire or upgrade fixed assets such as buildings, machinery, equipment, or vehicles in order to maintain or improve operations and foster future growth.

Carbon intensity: A measure of greenhouse gas emissions relative to a unit of output, such as revenue, energy produced or economic activity. Lower carbon intensity indicates greater efficiency or reduced emissions per unit of output.

Compute: The processing capacity of computer systems used to perform calculations and run workloads. In AI, compute refers to the ability to train and run models at scale.

Data centre: A physical facility that houses computing infrastructure, including servers, storage, networking equipment and power and cooling systems, to process and store data.

Environmental, Social, and Governance (ESG) factors relate to the quality and functioning of the natural environment, the rights, well-being and interests of people and communities, and the governance of companies & their stakeholders.

Energy storage: Technologies, such as batteries, that store electricity for later use, supporting grid stability, backup power and the integration of renewable energy sources.

Infrastructure investment: Investment into the physical assets of a nation or company, such as roads, railways, bridges, water, sewerage, port facilities, or telecommunications. Given that it usually requires large amounts of money, it is typically undertaken by governments or specialised investment strategies.

“Land, power and shell” refers to the core components of modern, hyperscale data centre development, particularly for AI infrastructure. It is a formula where developers secure land with guaranteed power access, constructing a “shell” building that is ready for a client to install their own IT equipment.

Moat (economic moat): A company’s sustainable competitive advantage that protects its long‑term profitability from competitors, such as network effects, scale, intellectual property or regulatory barriers.

Moore’s Law is the observation that the number of transistors on a microchip doubles roughly every two years, while the cost of computers is cut in half.

Next-generation infrastructure: The infrastructure needed to meet the evolving needs of businesses. It includes the shift to cloud infrastructure, industrial-scale computing, and storage that enables cheap and fast computing, as well as access to machine learning.

Portfolio: A grouping of financial assets such as equities, bonds, commodities, properties, or cash. Also often called a ‘fund’.

Portfolio turnover: The rate at which assets within a portfolio are bought and sold over a given period. Higher turnover indicates more frequent changes to portfolio holdings.

Productivity: A measure of efficiency that reflects how effectively inputs such as labour, capital or energy are converted into economic output.

A supercycle is an extended period – often 10 to 25 years – of abnormally strong demand and sustained price increases for commodities or economic sectors, where demand consistently outpaces supply.

Sustainable investing: An approach to investment that considers long‑term economic growth alongside environmental stewardship, social responsibility and sound governance.

Systems‑level sustainability: An investment framework that evaluates a company not only on its own operational footprint, but also on its role in enabling broader economic and environmental efficiency across the system it operates in.

Token: In the context of AI, a unit of data processed by an AI model. Tokens represent the basic units of input and output that AI systems use to generate responses or predictions.

Volatility: The rate and extent at which the price of a portfolio, security, or index, moves up and down. If the price swings up and down with large movements, it has high volatility. If the price moves more slowly and to a lesser extent, it has lower volatility. The higher the volatility, the higher the risk of the investment.