Key takeaways:

- Credit default swaps (CDS) allow investors to buy or sell protection against default, transferring credit risk from one counterparty to another.

- CDS spreads reflect perceived credit risk, rising when default risk increases and falling as a borrower’s creditworthiness improves.

- Widely used and standardised, CDS are a useful risk-management and investment tool, enabling investors to express positive or negative credit views efficiently.

Credit default swaps (CDS) are derivatives that enable an investor to swap or offset their credit risk (the risk that a borrower defaults on meeting its repayment obligations). It allows the transfer of credit risk from one counterparty to another.

That might sound intimidating but at its heart a CDS is essentially a form of insurance against a borrower failing to repay its debt.

What is credit risk?

Whenever someone lends money there is a risk that the borrower might default, i.e. not pay back the lender. For a bondholder a default would mean not receiving either the coupon (the regular interest payment on the bond) or the principal (the par value of the bond at maturity). This risk is called credit risk.

Differing views on credit risk is something that investors can potentially exploit, either by identifying bonds where the yields on offer either over or under-compensate for the risk.

One way to do that is by owning the physical bonds an investor likes and avoiding those they do not. Another way is by expressing a view on the creditworthiness of a bond issuer through a derivative such as a CDS.

CDS usage among investors – especially professional and institutional investors – is very common. In fact, during the first nine months of 2025 the combined European and US CDS traded notional value was US$24.6 trillion.1 This massive figure demonstrates just how widely used CDS are as both a risk management and investment tool.

1Source: ISDA (International Swaps and Derivatives Association), Credit Derivative Trading Activity Reported in EU, UK and US Markets: Third Quarter of 2025 and Year-to-September 30, 2025, January 2026. Traded notional is the total value of the underlying asset represented in a contract.

CDS: The basics

So how does an investor use CDS?

A CDS is a contract between two parties:

- The protection buyer who wants insurance against default

- The protection seller who agrees to compensate the buyer if default occurs

In exchange for this protection, the buyer pays a regular fee, known as the CDS premium or spread.

Buying protection is equivalent to taking a short position. The protection buyer (the CDS buyer) has effectively gone “short” the bond and will benefit when the reference entity’s credit quality deteriorates. Essentially, a buyer of CDS believes that the cost of insuring debt against default will rise. The buyer pays a premium (akin to an insurance premium and typically paid quarterly or semi-annually) to the seller.

Selling protection is equivalent to taking a long position. The seller receives the premium but is obligated to make the buyer whole again if the bond defaults. From a risk perspective, selling a corporate bond CDS means selling protection (and receiving premiums) and is equivalent to owning or being “long” the bond. This position will generate positive mark-to-market present value changes if the reference entity’s credit quality improves and credit spreads narrow during the life of the position.

CDS can therefore be useful in fund management as it allows the fund manager to express either a positive or negative view on a bond.

It is not necessary to own the bond to hold a CDS

Unlike traditional insurance (say on a house or car) you do not need to own the bond to buy a CDS on it. An investor can buy a CDS purely as a bet that a company’s creditworthiness will deteriorate. If they are wrong, then they have lost out as they have paid premiums for nothing.

For the CDS seller, they can sell CDS and collect the premiums in the hope that they will not have to pay out on the bond. CDS are unaffected by a bond being called early because unlike bondholders who when repaid need to identify another bond to invest in (reinvestment risk), the CDS seller continues to receive the premium from the counterparty to the end of the CDS contract.

CDS indices

As well as CDS for individual issuers, there are also CDS indices which operate in a similar manner but allow an investor to express a view on a basket of companies or the wider corporate bond market.

Standardised contracts

The market has steadily moved towards standardised CDS contracts. Typically these trade to 20 June and 20 December standardised maturity dates, and the contracts have a 100 basis points (bps) spread for investment grade bonds and 500bps for high yield (aligned with the CDS indices). This standardisation is useful because it makes valuation and trading much easier. It means buyers and sellers of CDS can open and close positions with multiple counterparties who can then enter into netting arrangements with each other. This is typically done at a Clearing House, which is essentially an intermediary that deals with both sellers and buyers of CDS.

The contract will include key terms such as

- Reference entity: the company whose credit risk is being traded.

- Notional amount: The total face value of the debt being protected.

- Maturity date: The period over which the contract runs, e.g. 3 or 5 years.

How is a CDS priced?

The price of a CDS will reflect a large number of factors, from the outlook for the specific company to the macroeconomic environment. Rising CDS spreads signal increasing default risk, while falling CDS spreads suggest improving credit quality. When there is heavy demand for protection, spreads rise. When there is heavy selling of protection, spreads fall. CDS spreads are constantly changing, reflecting the view of the creditworthiness of the borrower and the market environment.

| Often when there has been a default, the lender can recover some value. The percentage that might be recovered is known as the recovery rate so the market value of a bond may be higher than zero after default. An average recovery rate might be 40% but the range can vary significantly. |

In a very simplified formula:

Probability of default x loss given default = CDS spread

Taking the example above and assuming annual default probability is 2% and the loss given default is 60% (100-40% recovery) then CDS spread would be:

2% x 60% = 1.2% or 120 basis point spread

The buyer of protection would pay 120 basis points or 1.2% of the notional value of the contract each year to the seller for the length of the contract. For example, if a 5-year CDS is quoted at 120 basis points, and the notional value of the contract is $1 million, the buyer would pay $12,000 per annum (= $1 million x 1.2%) in return for the credit protection.

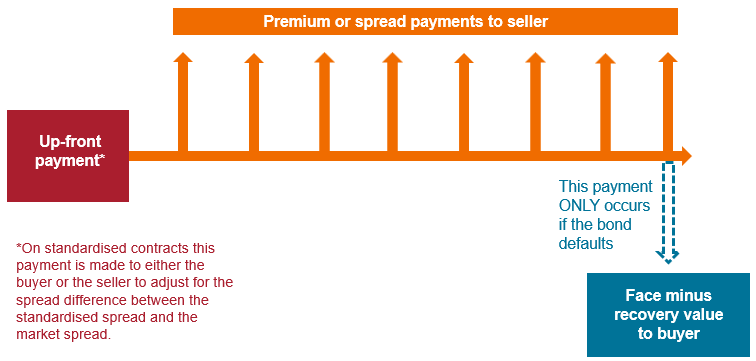

So how does that square with the standardised contracts? If an investment grade company’s CDS should be priced at 120 basis points, the seller does not want to be receiving only 100 basis points. To resolve this, the buyer of protection would pay an upfront payment to the seller that would make up the difference. The opposite would be true if the spread was lower than 100 basis points; the seller would need to make an upfront payment at the inception of the contract to the buyer to reflect the fact that the cashflows to be received each year are too generous.

Cash flows on CDS contracts

Source: Janus Henderson Investors. Simplified example for illustrative purposes only.

What happens if a bond defaults?

A CDS payout is triggered by specific events, called credit events, which are defined in the contract. Common examples include:

- Failure to pay interest or the principal

- Bankruptcy or insolvency

- Debt restructuring that is harmful to the lender

The exact definition of what counts as a default matters, so the legal wording has to be precise. Contracts are generally based on ISDA (International Swaps and Derivatives Association) Master Agreements, which dictate the terms for settlement.

When a credit event occurs, the CDS contract is settled in one of two ways:

- Cash settlement: The seller pays the buyer the difference between the bond’s face value and its market value after default.

- Physical settlement: The buyer delivers the defaulted bond to the seller and receives its full face value.

In practice, a CDS seller would a) aim to avoid holding exposure to an issuer that defaults and b) seek to go the other way on the contract if they began to lose conviction in the position and in so doing seek to limit the loss.

CDS contacts are mark-to-market. If perceived credit risk rises, credit spreads widen and the seller’s position may show a mark-to-market loss. They must post collateral (margin) even though no default has happened. The seller will of course receive the collateral back if the default does not occur.

Many of the risks facing a CDS buyer and seller are not much different to those facing any fixed income investor. For a CDS seller the biggest risk is that the borrower defaults and they have to pay the CDS buyer. Both sides face potential counterparty risk – the risk that the other side fails to honour the contract – however, with the move to central counterparty clearing, this risk is very much diminished.

Summary

In summary, CDS are commonly used in investment management to express views on the creditworthiness of borrowers. For buyers of CDS, they can help to mitigate risk, while sellers of CDS can earn a premium. Both buyers and sellers can also trade CDS, hoping to exploit movements in spread during the course of a contract. CDS have become an increasingly important tool in investment management and we anticipate the market to continue to grow over the coming years.

IMPORTANT INFORMATION

Fixed income securities are subject to interest rate, inflation, credit and default risk. The bond market is volatile. As interest rates rise, bond prices usually fall, and vice versa. The return of principal is not guaranteed, and prices may decline if an issuer fails to make timely payments or its credit strength weakens.

High-yield or “junk” bonds involve a greater risk of default and price volatility and can experience sudden and sharp price swings.

Derivatives can be more volatile and sensitive to economic or market changes than other investments, which could result in losses exceeding the original investment and magnified by leverage.

Basis point (bp) equals 1/100 of a percentage point, 1bp = 0.01%, 100bps = 1%.

Callable bond: A bond that can be redeemed or paid off by the issuer prior to the agreed maturity date.

Cash flow: The movement of cash from one party to another.

Coupon: A regular interest payment that is paid on a bond described as a percentage of the face value of an investment. For example, if a bond has a face value of $100 and a 5% annual coupon, the bond will pay $5 a year in interest.

Corporate bond: A bond issued by a company. Bonds offer a return to investors in the form of periodic payments and the eventual return of the original money invested at issue on the maturity date.

Credit rating: An independent assessment of the creditworthiness of a borrower by a recognised agency such as S&P Global Ratings, Moody’s or Fitch. Standardised scores such as ‘AAA’ (a high credit rating) or ‘B’ (a low credit rating) are used, although other agencies may present their ratings in different formats. BB, B and CCC are high yield ratings in declining order of creditworthiness.

Credit spread: The difference in yield between securities with similar maturity but different credit quality. Widening spreads generally indicate deteriorating creditworthiness of corporate borrowers, and narrowing indicate improving.

Creditworthiness: A measure of a borrower’s ability and willingness to repay their debts. A company with high creditworthiness is seen as safer to lend to while low creditworthiness signals higher risk.

Counterparty: The opposite party in a contract or financial transaction. Central Counterparty (CCP) Clearing is where a financial institution acts as an intermediary between buyers and sellers. A central counterparty will net off trades between market participants, simplifying an otherwise complex web of bilateral trades. They also demand collateral (margin) from members which helps reduce the risk of potential future exposure in the event of default by a clearing member.

Default: The failure of a debtor (such as a bond issuer) to pay interest or to return an original amount loaned when due.

Derivative: A financial instrument for which the price is derived from one or more underlying assets such as shares, bonds, commodities, or currencies. It is a contract between two or more parties which allows investors to take advantage of price movements in the asset(s).

Fundamentals: The underlying financial and operational factors, such as profitability, cash flow and management quality, that indicate a company’s ability to meet its financial obligations.

High yield bond: Also known as a sub-investment grade bond, or ‘junk’ bond. These bonds usually carry a higher risk of the issuer defaulting on their payments, so they are typically issued with a higher interest rate (coupon) to compensate for the additional risk.

Investment grade bond: A bond typically issued by governments or companies perceived to have a relatively low risk of defaulting on their payments, reflected in the higher rating given to them by credit ratings agencies.

ISDA: The International Swaps and Derivatives Association is a trade organisation that seeks to foster safe and efficient derivatives markets. The ISDA Master Agreement outlines the contractual relationship between parties in derivative transactions.

Issuance: The act of making bonds available to investors by the borrowing (issuing) company, typically through a sale of bonds to the public or financial institutions. The company issuing the bonds is the Issuer.

Long position: A trade that seeks to profit from an appreciation in the price of an asset.

Mark-to-market: The daily adjustment of a contract’s value based on current market prices.

Maturity: The maturity date of a bond is the date when the principal investment (and any final coupon) is paid to investors. For a CDS, the maturity date is the last date of the contract’s term.

Notional value/amount: In a CDS contract this is the principal amount of debt insured by the contract.

Par value, Face value or Principal: The original value of a security, such as a bond, when it is first issued. Bonds are usually redeemed at par value when they mature.

Present value: The current worth of a future sum of money or stream of cash flows, discounted at a specific rate of return.

Reference entity: The company whose credit quality is being traded, i.e. the one on which protection is bought and sold.

Reinvestment risk: The risk that an investor may be unable to reinvest coupon payments or principal repayments on a bond at a rate comparable to their current bond’s yield, notably when interest rates fall. Callable bonds are susceptible this as issuers often call (redeem) them early when interest rates fall.

Short position: A trade that seeks to profit from the deterioration in the price of an asset.

Yield: The level of income on a security over a set period, typically expressed as a percentage rate. For a bond, at its most simple, this is calculated as the coupon payment divided by the current bond price.

Volatility: A measure of risk using the dispersion of returns for a given investment. The rate and extent at which the price of a portfolio, security or index moves up and down.