Key takeaways:

- Active enhanced income strategies typically use three adjustable levers – stock selection, dividend yield, and option writing – to seek total return, not just the highest available yield.

- We believe quality matters more than headline yield. In our view, companies with strong free cash flow and sound balance sheets may make better long-term income sources and stronger covered-call candidates.

- Writing covered calls on individual securities and adjusting how much of a portfolio is overwritten based on conviction and market conditions may enable managers to capture premiums where they are most compelling while preserving upside where it matters most.

Enhanced income equity strategies have attracted considerable interest in recent years, and the reasons are straightforward. Investors, particularly those in or approaching retirement, are searching for yield. Traditional dividend strategies help but can fall short of meeting income goals on their own, while bonds offer income but limit participation in equity upside.

Enhanced income strategies offer a third path: equity ownership combined with an options overlay that seeks to generate additional yield and may help dampen volatility, typically through writing out-of-the-money covered calls.

Growth and accessibility of the options market

Familiarity with the options market has grown, helping enhanced income strategies break through to income-seeking investors. Retail participation in options expanded meaningfully in the post-2021 period alongside “meme” investing.1 The introduction of daily index options in 2022 further broadened access and liquidity.

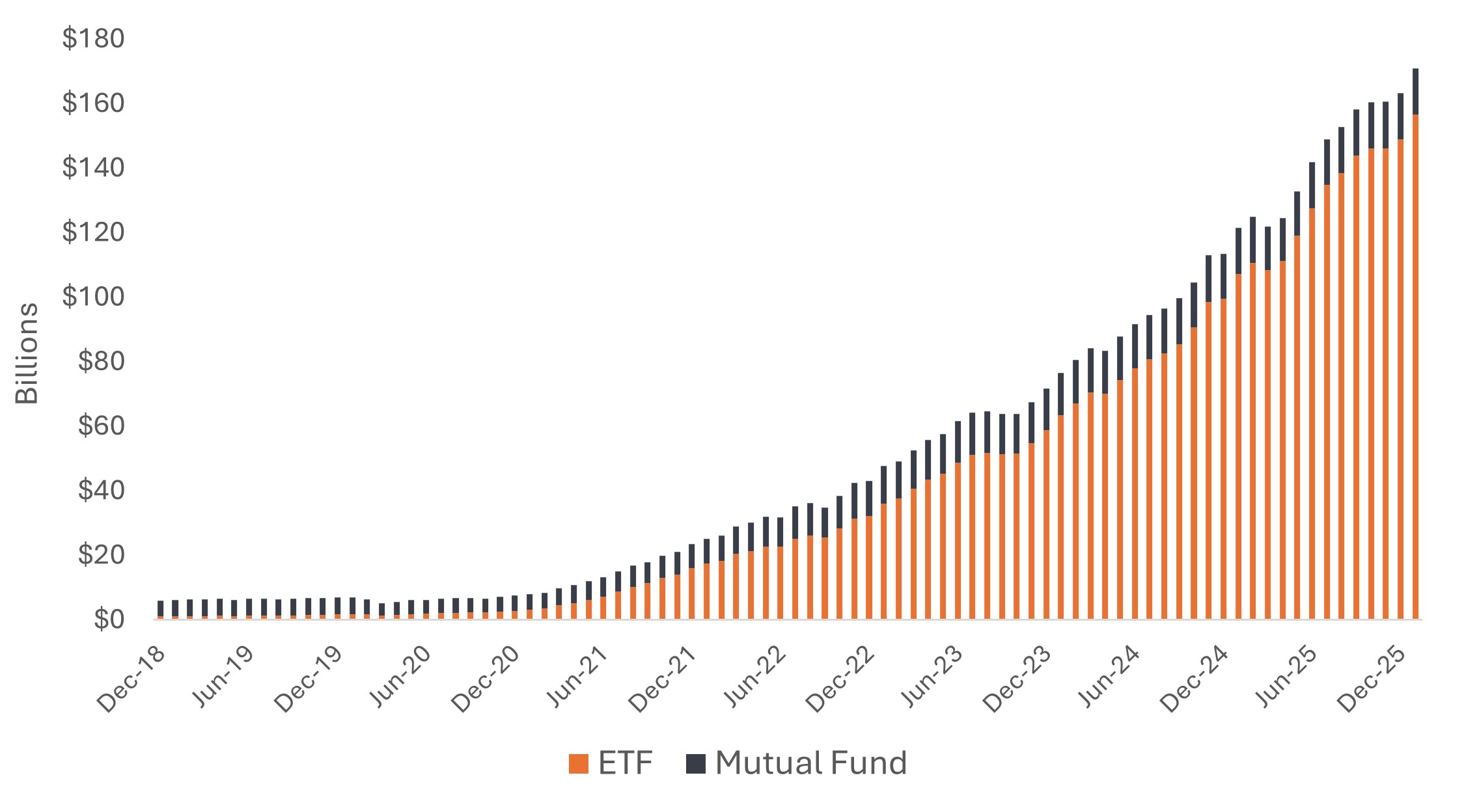

As a result of this widened adoption, Morningstar’s Derivative Income category has grown rapidly. In April 2021, assets in the category stood at roughly $7 billion across mutual funds and exchange-traded funds (ETFs). Today the category holds approximately $160 billion in ETFs alone – a roughly 23-fold increase – with the majority of assets in actively managed ETFs. Since January 2025, approximately 115 derivative-income ETFs have launched, bringing the total to around 235 funds in the category.2

Part of the appeal also relates to risk considerations and simplicity. Enhanced income strategies are designed to generate yield that would otherwise require either taking on significant credit risk in fixed income or concentrating heavily in the highest-yielding corners of the equity market. In ETF form, they make an approach that was once complex and operationally demanding for individual investors – setting up option accounts, managing approvals, executing trades – more accessible through a single fund holding.

Exhibit 1: A growing category of income diversifiers: Morningstar Derivative Income Category

Source: Morningstar Direct, as of 31 January 2026.

Three levers, actively managed

When it comes to active variations of enhanced income strategies, it helps to think about the components of total return and the flexibility to adjust each one. We see value in an approach that can engage three levers simultaneously – fundamental stock selection, dividend yield management, and an active options strategy overlay – and calibrate each depending on where the best risk-adjusted opportunities sit at any given time.

That flexibility is the key contrast with systematic strategies, which typically apply a fixed options overlay – selling covered calls on the entire portfolio at predetermined intervals – regardless of market conditions or the investment outlook for individual holdings. When equity markets are trending strongly, a systematic approach has no mechanism to pull back on option writing. When a specific stock looks fully valued, it gets treated the same as ones with meaningful upside remaining.

In contrast, an active approach treats options writing as an investment decision: If a company is approaching a high-stakes earnings announcement and implied volatility is elevated, selling calls in that situation may potentially harvest richer premiums without broadly capping a portfolio’s upside. That kind of selectivity – which requires both a fundamental view on the stock and an understanding of options pricing – is where active management can add value, in our view.

Lever one: Start with the right companies

The foundation of an enhanced income strategy is the equity portfolio itself. We believe it is important to start with businesses that have the financial strength to sustain and grow their dividends over time – not just in favorable conditions, but through full economic cycles. That means looking for strong free cash flow, sound balance sheets, competitive advantages, and management teams with a track record of disciplined capital allocation.

This focus on quality may also make the underlying portfolio more suitable for an options overlay. Higher-quality businesses tend to produce less volatile stock prices, which supports a more consistent environment for writing options. In other words, the same attributes that make a company a sound long-term equity holding can make it a stronger candidate for covered call writing. Long-term earnings growth potential is also a key input, as capital appreciation remains a meaningful component of total return alongside income.

Conversely, avoiding value traps – companies where an apparently elevated dividend yield reflects a falling share price and a likely dividend cut – is as important as identifying the right names to own.

Lever two: Managing yield as a variable

The second lever is dividend yield – specifically, how much total return comes from dividend income versus capital appreciation at any given time. Even when aiming for a baseline yield level, that level is a starting point, not a fixed constraint. If the environment favors capital appreciation, the portfolio can carry a lower yield and lean toward companies with stronger growth profiles. When income needs to carry more weight – in a sideways or more volatile market – the portfolio can shift toward higher-yielding names.

The composition of yield also varies between U.S. and international portfolios, reflecting different opportunity sets in each market. A U.S.-focused portfolio may derive a smaller share of total yield from dividends and a larger share from option premiums. In part this reflects that some lower- or non-dividend paying U.S. companies may pass quality screens and offer attractive prospects for options income, making them strong candidates for inclusion. An international portfolio, where dividend yields on underlying holdings are typically higher, could draw more heavily on dividend income, with the options overlay providing a complementary boost to reach a similar total yield range.

Lever three: Writing options with judgement

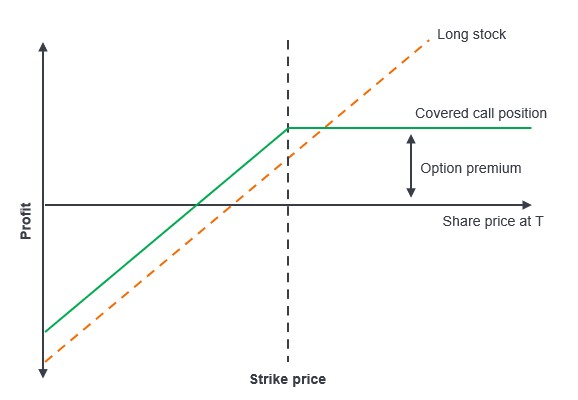

The third lever is the options overlay itself. Writing covered calls generates premium income by giving another party the right to purchase a stock at a set price within a defined time period. If the stock stays below that price, the seller keeps the premium. If it rises through the strike price, gains above that level are forgone – but the premium has already been collected.

Exhibit 2: Structure of a covered call

In a flat or range-bound market, this trade-off is favorable. In a sustained bull market, some upside is typically sacrificed. A 30-year Goldman Sachs analysis found that adding an option overlay to 60/40 portfolio increased expected returns while reducing volatility across a wide variety of environments.[1]

Writing options at the individual stock – rather than at the index level – creates an additional layer of opportunity. Beneath the surface of a broad index, individual names can carry very different volatility profiles. Writing calls on single stocks allows a strategy to harness that dispersion, which may help capture richer premiums where volatility is highest and applying a more selective touch where it is lower.

Active managers can also calibrate strike prices, expiration dates, and the percentage of each position overwritten to reflect both current market conditions and an investment view on the underlying stock. For a stock approaching a price target, writing a call near that level generates income and, if exercised, results in trimming the position at a price already considered full. For a stock with significant upside remaining, the appropriate response may be to write little or nothing, preserving participation in that appreciation.

In practice, enhanced income portfolios may only overwrite a portion of their portfolio, adjusting that range depending on conviction and market conditions. That leaves the majority of the portfolio uncapped and able to participate in equity upside. The put-writing component adds further flexibility: When conviction on the stock is high but near-term entry timing is uncertain, writing a put at an attractive price may collect additional premium while expressing a willingness to add to the position at a lower level.

The total return case for active enhanced income

Enhanced income strategies play a distinct role in a portfolio: seeking to provide yield, maintain equity participation, and offer a degree of stability that traditional equity exposure alone cannot. But the value of these strategies depends heavily on how they are built and managed, in our view.

We believe the more durable approach is one that treats each of the three levers as an active investment decision:

- Start with high-quality businesses selected for their ability to sustain dividends and deliver capital appreciation over time.

- Manage dividend yield as a flexible input that can be adjusted to what the market environment demands.

- Deploy the options overlay opportunistically – writing where premiums are most compelling, pulling back where upside conviction is highest, and calibrating strike prices and overwrite levels to reflect a view on each stock.

An enhanced income strategy that runs on an options “autopilot” may deliver yield but could sacrifice opportunities to maximize total return potential. In contrast, an active strategy that is focused on quality and treats options writing as discrete investment decisions may help deliver more than yield alone.

IMPORTANT INFORMATION

Actively managed portfolios may fail to produce the intended results.

Any yield management process discussed includes an effort to monitor and manage yield which should not be confused with and does not imply the ability to control yield.

Derivatives can be more volatile and sensitive to economic or market changes than other investments, which could result in losses exceeding the original investment and magnified by leverage.

Covered call strategies can limit the ability to benefit from increases in the market value of the underlying securities because upside potential is capped by the option’s strike price. While option premiums can help offset declines, they may not fully protect against losses, and option exercises can result in selling securities at times that may not be advantageous.

Equity securities are subject to risks including market risk. Returns will fluctuate in response to issuer, political and economic developments.

Fixed income securities are subject to interest rate, inflation, credit and default risk. As interest rates rise, bond prices usually fall, and vice versa. High-yield bonds, or “junk” bonds, involve a greater risk of default and price volatility. Foreign securities, including sovereign debt, are subject to currency fluctuations, political and economic uncertainty and increased volatility and lower liquidity, all of which are magnified in emerging markets.

Options may be difficult to trade under certain market conditions, and imperfect correlation between an option and its underlying securities can reduce the effectiveness of an options strategy.

Carry is the excess income earned from holding a higher yielding security relative to another.

Volatility measures risk using the dispersion of returns for a given investment.

Yield: The level of income on a security over a set period, typically expressed as a percentage rate. For equities, a common measure is the dividend yield, which divides recent dividend payments for each share by the share price. For a bond, this is calculated as the coupon payment divided by the current bond price.

1 CBOE, “Option Flow 2021 – Retail Rising”, 2022

2 Source: JHI analysis, Morningstar Direct, as of 5 March 2026.

3 Goldman Sachs Research, Optimal Asset Allocation with Option Overlay Strategies, 17 December 2025.