Downturn implications and a reconvergence of rates

The global manufacturing downturn has recently entered its fourteenth consecutive month of decline as measured by the Global Manufacturing PMI. The downturn, which emanated in Asia, has had a severe knock-on effects on economies like Germany, which have created an economic model heavily interconnected with an emergent China in recent decades.

6 beknopt artikel

Kernpunten

- The global manufacturing downturn has recently entered its fourteenth consecutive month; but examining the downturn through the prism of the US may leave investors with too sanguine a view.

- While policy options are mostly hamstrung in Japan, Europe has ample room to buy more corporate bonds. Meanwhile, the US and Australia have the means for further conventional easing.

- In our view, the next big move in developed bond markets will ultimately see interest rates reconverge, with the US moving down towards the rest.

In other countries, such as Australia, it has coincided with a housing and consumer downturn, whose rhythm has been out of step with the slow consumer deleveraging in the rest of the developed world.

The result of such a prolonged period of weak global trade and export growth is that many central banks have moved on from the ‘denial’ phase and are actively discussing, and in some cases pursuing, monetary easing (Australia and New Zealand).

An unusual cycle with the Fed out of the driving seat

Looking at this global growth downturn through the prism of the US economy is fraught with danger, as investors are likely to come away with too sanguine a view. We have said in the past that the US was not the source of this slowdown (unlike in 2000 and 2007) and it remains a relatively insular economy — US exports form approximately 15% of its GDP versus 50% in Germany and 30% in the UK.

This is an unusual cycle where other central banks and the bond markets in the developed world are now conducting the mood music, which the US Federal Reserve (Fed) is increasingly reactive to. This note explores the policy options in various countries to enact meaningful policy easing.

As we sit near or at the lower bound for interest rates, the ability to act is a new question for investors who previously focused on the willingness to act.

Central banks that have not done QE yet…

…a relatively sparse list of central banks in the developed world, but one that includes both Australia and Canada. Notably, Australia has only cut rates since 2011. With interest rates currently sitting at a historic low of 1.25% and expected to fall to at least 1%, this bank only begun discussing quantitative easing (QE) as a policy tool in December 2018. In a speech given by Guy Debelle, Deputy Governor, he stated that “QE is a policy option in Australia, should it be required. There are less government bonds here, which may make QE more effective. But most of the traction in terms of borrowing rates in Australia is at the short end of the curve rather than the longer end of the curve, which might reduce the effectiveness of QE.”

In our view, it was no coincidence that the foreign currency pairing of AUDJPY (Australian dollar versus the Japanese yen) experienced a 7% flash crash in a few hours in early January 2019, following an eight percent depreciation in the month prior to this move. This currency pairing perfectly encapsulates the central bank with the most (Australia), and the one with the least (Japan), scope for monetary policy easing.

Evolving reaction function at the Fed

The Fed signalled in early 2019 that rates had peaked but appears to be in an intellectual transition regarding the policy framework and the ability of the US economy to remain immune from the global industrial downturn.

In this context, there is renewed focus on the structural undershooting of inflation since 2009. Notably, this is a very different spin from the comparisons to 1967 (inflation breakout risk) provided by Fed Chair Powell in the summer of 2018. Here, under the guidance of Vice Chair, Clarida, there is renewed focus on the international experience of low inflation and interest rates.

The recent signalling of a readiness to cut interest rates appears logical. The final 50 basis points of hikes in October and December 2018 into pronounced weakness in rates-sensitive sectors such as housing and autos, was clearly a mistake. Any deterioration in the employment market from here will likely engender an even stronger reaction. It is worth remembering that ‘surprising’ in a rate cutting cycle is admirable (unlike in a rate hiking cycle).

ECB’s Draghi (and board) retiring soon plus hamstrung policy options in Japan

This is where it gets really interesting. First, because the starting point is not one that you would choose as a policymaker (negative interest rates plus government bond purchases close to their legal and technical limit), and second, because in Europe President Draghi and significant members of the board are due to retire in 2019.

Starting with the European Central Bank (ECB), Mario Draghi has been clear that he believes the bank has room in all of its policy levers — including rate cuts into even more negative territory. It is worth noting that at -0.4% deposit rate the only relevant comparable is Switzerland with a -0.75% sight deposits rate, even Japan sits at -0.1% (key interest rate).

In our view the most likely meaningful policy loosening is through investment grade corporate bond purchases, which was first announced in March 2016. The ECB owns €178bn (approximately 20%) of the eligible universe of corporate bonds. Its mandate allows purchases of up to 70% (ECB, 31 May 2019). An increase to 40% seems wholly credible and would imply another €200bn of purchases of eligible investment grade corporate bonds.

In the case of Japan, policy options really do look close to exhausted. With close to 50% of the JGB market owned by the central bank, explicit yield curve control (target for 10-year yields), negative interest rates and purchases of equity ETFs for years, it is difficult to find a policy option which could surprise to the upside.

The key constraining factor for the Bank of Japan was the market reaction in January 2016 when it cut interest rates into negative territory. The share price of banks plummeted and its currency moved higher as a result of a risk-off reaction. This effectively tightened financial conditions and illustrated how hamstrung policy options were and still are.

Stopping inflation expectations from sliding into the abyss

In summary, the next big move for bond markets will likely see interest rates in the developed world reconverge. For many years, consensus has argued that this was likely to occur through rates in the rest of the developed world moving up towards US interest rates. We have long disagreed and positioned for continuing divergence between the US and rest of the world viewing many economies as trapped in a lobster pot of low interest rates and quantitative easing.

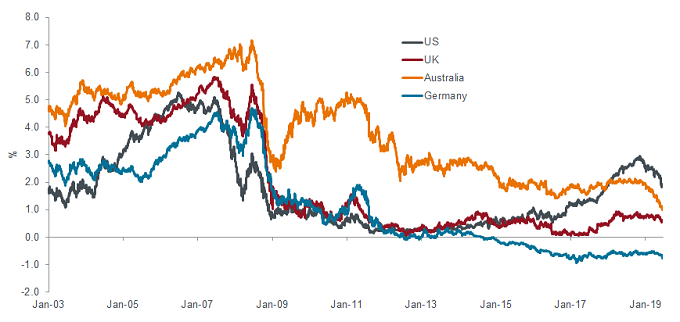

Short-term rates signalling rate cuts?

Source: Bloomberg, Janus Henderson Investors, as at 18 June 2019 Note: Generic 2-year bond yields

Source: Bloomberg, Janus Henderson Investors, as at 18 June 2019 Note: Generic 2-year bond yields

The next big structural move in interest rates and government bond yields should be policy easing from those with ability to do so (ie, the US and Australia). For Europe, a move into private assets (corporate bonds) is likely as the limit of meaningful government bond QE is reached.

This may not be the ‘normalisation’ many hoped for but it is a natural reaction for inflation targeting central banks trying desperately to keep inflation expectations from sliding into a natural abyss, driven by long-term structural factors over which they have little control.

Dit zijn de standpunten van de auteur op het moment van publicatie en kunnen verschillen van de standpunten van andere personen/teams bij Janus Henderson Investors. Verwijzingen naar individuele effecten vormen geen aanbeveling om effecten, beleggingsstrategieën of marktsectoren te kopen, verkopen of aan te houden en mogen niet als winstgevend worden beschouwd. Janus Henderson Investors, zijn gelieerde adviseur of zijn medewerkers kunnen een positie hebben in de genoemde effecten.

Resultaten uit het verleden geven geen indicatie over toekomstige rendementen. Alle performancegegevens omvatten inkomsten- en kapitaalwinsten of verliezen maar geen doorlopende kosten en andere fondsuitgaven.

De informatie in dit artikel mag niet worden beschouwd als een beleggingsadvies.

Reclame.

Belangrijke informatie

Lees de volgende belangrijke informatie over fondsen die vermeld worden in dit artikel.

- Het is mogelijk dat een emittent van een obligatie (of geldmarktinstrument) niet langer bereid of in staat is om de rente te betalen of kapitaal aan het Fonds terug te betalen. Als dit gebeurt of als de markt denkt dat dit kan gebeuren, zal de waarde van de obligatie dalen.

- Wanneer de rentevoeten stijgen (of dalen), zullen de prijzen van verschillende effecten anders worden beïnvloed. In het bijzonder zal de waarde van obligaties gewoonlijk dalen als de rentevoeten stijgen. Over het algemeen wordt dit risico groter naarmate de looptijd van een obligatiebelegging toeneemt.

- Het Fonds belegt in hoogrentende obligaties (onder beleggingskwaliteit). Hoewel dergelijke obligaties doorgaans hogere rentevoeten bieden dan obligaties van beleggingskwaliteit, zijn ze speculatiever van aard en zijn ze gevoeliger voor ongunstige veranderingen in de marktomstandigheden.

- Sommige obligaties (op verzoek aflosbare obligaties) geven hun emittenten het recht om kapitaal vervroegd terug te betalen of om de looptijd te verlengen. Emittenten kunnen deze rechten uitoefenen wanneer dit voor hen gunstig is en dit kan invloed hebben op de waarde van het Fonds.

- Als een Fonds een hoge blootstelling heeft aan een bepaald land of een bepaalde geografische regio, loopt het een hoger risico dan een Fonds dat meer gediversifieerd is.

- Het Fonds kan gebruikmaken van derivaten om zijn beleggingsdoelstelling te verwezenlijken. Dit kan leiden tot hefboomwerking, wat de resultaten van een belegging kan uitvergroten en waardoor de winsten of verliezen van het Fonds groter kunnen zijn dan de kosten van het derivaat. Het gebruik van derivaten gaat ook gepaard met andere risico's, waaronder met name het risico dat een tegenpartij bij derivaten niet in staat is om haar contractuele verplichtingen na te komen.

- Wanneer het Fonds, of een afgedekte aandelenklasse/klasse van deelnemingsrechten, tracht de wisselkoersschommelingen van een valuta ten opzichte van de basisvaluta te beperken, kan de afdekkingsstrategie zelf een positieve of negatieve impact hebben op de waarde van het Fonds vanwege verschillen in de kortetermijnrentevoeten van de valuta's.

- Effecten in het Fonds kunnen moeilijk te waarderen of te verkopen zijn op het gewenste moment of tegen de gewenste prijs, vooral in extreme marktomstandigheden waarin de prijzen van activa kunnen dalen, wat het risico op beleggingsverliezen verhoogt.

- De volledige lopende kosten of een deel daarvan kunnen aan het kapitaal worden onttrokken, wat het kapitaal kan uithollen of het potentieel voor kapitaalgroei kan verminderen.

- CoCo's (Voorwaardelijk converteerbare obligaties) kunnen sterk in waarde dalen wanneer de financiële gezondheid van een emittent verzwakt en een vooraf bepaalde 'triggergebeurtenis' ertoe leidt dat de obligaties worden omgezet in aandelen van de emittent of gedeeltelijk of volledig worden afgeschreven.

- Het Fonds kan geld verliezen als een tegenpartij met wie het Fonds handelt niet bereid of in staat is om aan zijn verplichtingen te voldoen, of als gevolg van een fout in of vertraging van operationele processen of verzuim van een derde partij.

Specific risks

6 beknopt artikel

Kernpunten

- The global manufacturing downturn has recently entered its fourteenth consecutive month; but examining the downturn through the prism of the US may leave investors with too sanguine a view.

- While policy options are mostly hamstrung in Japan, Europe has ample room to buy more corporate bonds. Meanwhile, the US and Australia have the means for further conventional easing.

- In our view, the next big move in developed bond markets will ultimately see interest rates reconverge, with the US moving down towards the rest.