Key takeaways:

- Markets are reacting to energy supply and shipping risks rather than geopolitical escalation. Oil prices are reflecting a temporary risk premium, with duration – not headlines – determining whether the shock becomes macro‑relevant for emerging markets (EMs).

- Sustained higher energy prices would increase differentiation across EMs, benefiting exporters while pressuring importers through weaker trade balances, inflation pass‑through and wider spreads. So far, market reactions remain orderly and contained.

- We are closely monitoring energy‑driven pressures, sovereign bond market responses and country‑level impacts, engaging actively with research providers and market participants to identify vulnerabilities should a persistent shock materialise.

As markets assess the conflict in the Middle East, the dominant transmission channel has not been geopolitical escalation itself, but the implications for energy flows. Oil prices moved sharply higher and commercial shipping through the Strait of Hormuz effectively stalled, driven by heightened security risks, tanker incidents, GPS interference and the withdrawal of insurance coverage. To date, markets are pricing in an energy risk premium, rather than a confirmed or permanent loss of supply, but the situation remains fluid.

Will it be short-lived?

Whether this is a short-lived geopolitical risk-shock, a structural shock to oil prices or somewhere in between is key as it will determine the impact on the global economy and the resultant winners and losers.

Other channels, including inflation dynamics and potential US Federal Reserve (Fed) interest rate repricing, are secondary and become relevant only if energy prices remain elevated for a sustained period.

In practical terms, markets will be driven by oil prices and their persistence over time, with clear implications for EM winners and losers:

- Short-term: Oil price volatility is the dominant driver. Short‑lived geopolitical shocks historically have little real economic effect, and markets can absorb temporary energy spikes. Near‑term price action is therefore likely to reflect risk premia and positioning rather than a fundamental reassessment of growth.

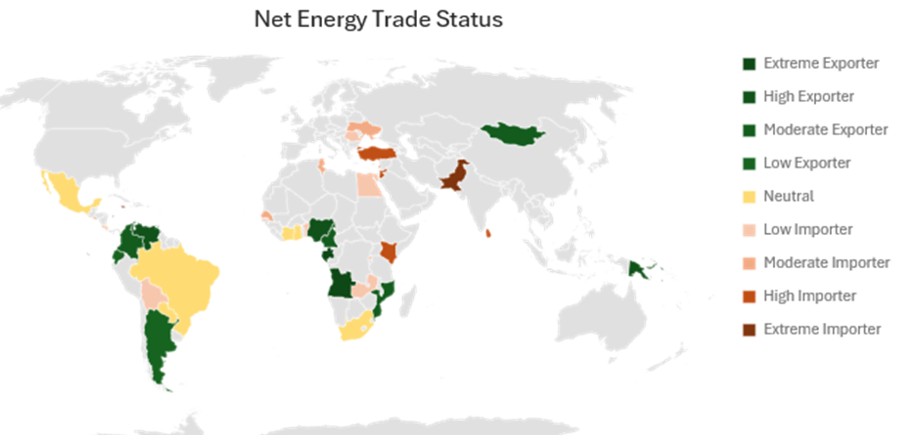

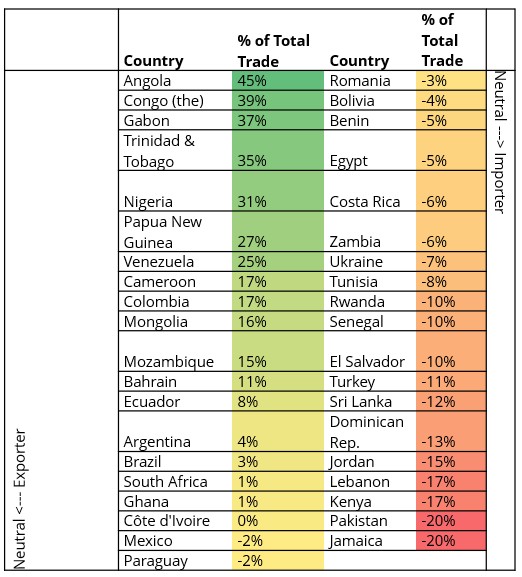

- Medium-term: If elevated oil prices persist, differentiation across EM becomes more pronounced. Oil exporters benefit, while energy‑importing sovereigns face pressure through weaker trade balances (as reflected in their net energy trade positions in Figure 1 and 2), inflation pass‑through and wider sovereign bond spreads.

- Long term: A sustained period of high energy prices would materially alter the global macroeconomic outlook, feeding into inflation expectations, central‑bank policy re-pricing (including the Fed), and broader financial conditions.

In short, duration matters more than headlines. The longer energy prices remain elevated, the more macro‑relevant the shock becomes, and the more differentiation we expect to see within EM.

Figure 1: Emerging market oil/energy sensitivity

Source: Austrlian Bureau of Statistics, GeoNames, Microsfot, Navinto, Open Places, OpenstreetMap, Overture Maps Foundation, TomTom, Zenrin, as at 2 March 2026.

Figure 2: Net energy trade as a % of total trade

Source: Stifel, 2 March 2026.

Near‑term outcomes hinge on energy and shipping stabilisation

This remains a developing situation, and near‑term outcomes will depend on how quickly energy markets and shipping conditions normalise. We are actively engaging with internal and external research providers, market participants and regional specialists to assess market sentiment, evolving risks and country‑level implications. Our focus is on understanding where energy‑driven pressures are most acute, how sovereign bond markets are responding, and how various EM countries are impacted. So far, the market reaction has been very orderly, with only a modest spread widening and muted safe-haven behaviour.

Sovereign: Typically refers to debt issued by a national government. Sovereign bonds are backed by the country’s creditworthiness and ability to repay.

Emerging market investments have historically been subject to significant gains and/or losses. As such, returns may be subject to volatility.

Sovereign debt securities are subject to the additional risk that, under some political, diplomatic, social or economic circumstances, some developing countries that issue lower quality debt securities may be unable or unwilling to make principal or interest payments as they come due.

Fixed income securities are subject to interest rate, inflation, credit and default risk. The bond market is volatile. As interest rates rise, bond prices usually fall, and vice versa. The return of principal is not guaranteed, and prices may decline if an issuer fails to make timely payments or its credit strength weakens.

Foreign securities are subject to additional risks including currency fluctuations, political and economic uncertainty, increased volatility, lower liquidity and differing financial and information reporting standards, all of which are magnified in emerging markets.

Credit spread: The difference in yield between securities with similar maturity but different credit quality, often used to describe the difference in yield between corporate bonds and government bonds. Widening spreads generally indicate a deteriorating creditworthiness of corporate borrowers, while narrowing indicates improving.

Financial Conditions: Financial conditions describe the overall ease or tightness with which households, businesses and governments can obtain funding in the economy.

Inflation: The rate at which the prices of goods and services are rising in an economy. The consumer price index (CPI) and retail price index (RPI) are two common measures; the opposite of deflation.

Interest rates: The amount charged for borrowing money, shown as a percentage of the amount owed. Base interest rates (the Bank Rate) are generally set by central banks, such as the Federal Reserve in the US or Bank of England in the UK, and influence the interest rates that lenders charge to access their own lending or saving.

Net energy trade position: The net energy trade position represents the difference between a country’s or region’s total energy exports and total energy imports, indicating whether they are a net exporter (positive) or a net importer (negative).

Risk premium: The additional return an investment is expected to provide in excess of the risk-free rate. The riskier an asset is deemed to be, the higher its risk premium to compensate investors for the additional risk.

These are the views of the author at the time of publication and may differ from the views of other individuals/teams at Janus Henderson Investors. References made to individual securities do not constitute a recommendation to buy, sell or hold any security, investment strategy or market sector, and should not be assumed to be profitable. Janus Henderson Investors, its affiliated advisor, or its employees, may have a position in the securities mentioned.

Past performance does not predict future returns. The value of an investment and the income from it can fall as well as rise and you may not get back the amount originally invested.

The information in this article does not qualify as an investment recommendation.

There is no guarantee that past trends will continue, or forecasts will be realised.

Marketing Communication.

Important information

Please read the following important information regarding funds related to this article.

- An issuer of a bond (or money market instrument) may become unable or unwilling to pay interest or repay capital to the Fund. If this happens or the market perceives this may happen, the value of the bond will fall. High yielding (non-investment grade) bonds are more speculative and more sensitive to adverse changes in market conditions.

- When interest rates rise (or fall), the prices of different securities will be affected differently. In particular, bond values generally fall when interest rates rise (or are expected to rise). This risk is typically greater the longer the maturity of a bond investment.

- Some bonds (callable bonds) allow their issuers the right to repay capital early or to extend the maturity. Issuers may exercise these rights when favourable to them and as a result the value of the Fund may be impacted.

- Emerging markets expose the Fund to higher volatility and greater risk of loss than developed markets; they are susceptible to adverse political and economic events, and may be less well regulated with less robust custody and settlement procedures.

- The Fund may use derivatives to help achieve its investment objective. This can result in leverage (higher levels of debt), which can magnify an investment outcome. Gains or losses to the Fund may therefore be greater than the cost of the derivative. Derivatives also introduce other risks, in particular, that a derivative counterparty may not meet its contractual obligations.

- When the Fund, or a share/unit class, seeks to mitigate exchange rate movements of a currency relative to the base currency (hedge), the hedging strategy itself may positively or negatively impact the value of the Fund due to differences in short-term interest rates between the currencies.

- Securities within the Fund could become hard to value or to sell at a desired time and price, especially in extreme market conditions when asset prices may be falling, increasing the risk of investment losses.

- The Fund may incur a higher level of transaction costs as a result of investing in less actively traded or less developed markets compared to a fund that invests in more active/developed markets.

- Some or all of the ongoing charges may be taken from capital, which may erode capital or reduce potential for capital growth.

- CoCos can fall sharply in value if the financial strength of an issuer weakens and a predetermined trigger event causes the bonds to be converted into shares/units of the issuer or to be partly or wholly written off.

- The Fund could lose money if a counterparty with which the Fund trades becomes unwilling or unable to meet its obligations, or as a result of failure or delay in operational processes or the failure of a third party provider.