Key takeaways:

- U.S. GDP growth is expected to remain around 2% in 2026, supported by resilient consumer spending and AI-driven investment, despite lingering geopolitical and tariff risks.

- In our view, inflation is likely to stay above target, but markets anticipate at least three Federal Reserve (Fed) rate cuts by year-end 2026, which would lead to a steeper yield curve and supportive conditions for spread sectors.

- Attractive opportunities exist within credit spread sectors broadly, and securitized sectors specifically, with positive real yields and active, flexible management key to navigating volatility and policy uncertainty.

As investors consider their fixed income positioning for 2026, we believe current yields offer an attractive entry point to the multi-sector fixed income category. Various spread sectors exhibit compelling relative value opportunities and are supported by a constructive macro backdrop and monetary policy environment.

1. Macro backdrop

We expect the overall macroeconomic environment to continue to be supportive of current spread levels. We anticipate U.S. economic growth will remain positive, with real gross domestic product (GDP) growth coming in at about 2.0% in 2026.

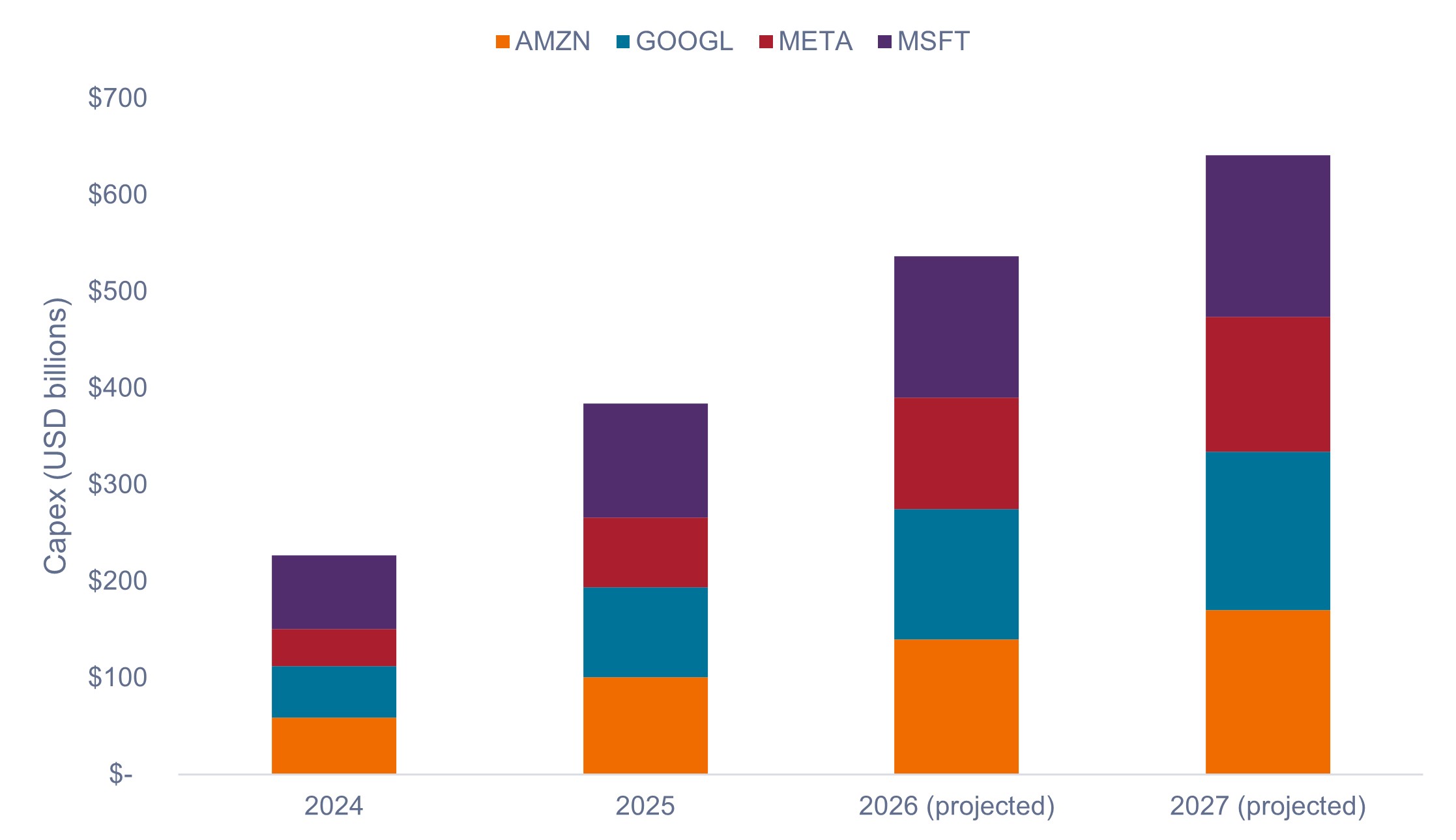

While some industries are entering 2026 on late-cycle footing, resilient spending from higher-end consumers and corporate profitability gains from artificial intelligence (AI) implementation should continue to underpin a resilient U.S. economy. Additionally, parabolic increases in AI-driven investment in chips and data centers will likely provide fuel for sustained economic growth, as shown in Exhibit 1.

Exhibit 1: Hyperscalers’ capital expenditures (2024-2027)

Aggressive increases in AI infrastructure spend should fuel sustained economic growth.

Source: Company data, Morgan Stanley Research estimates, as of 21 November 2025. No forecasts can be guaranteed.

While tariff-related uncertainty, immigration reform, and geopolitical tensions have been key risks in 2025, we expect their effects to be less pronounced in 2026. Importantly, we believe any lingering negative impacts from these risks should be countered by the positive effects of tax reform within the One Big Beautiful Bill (OBBB), much of which takes effect in 2026. Other notable contributors to U.S. GDP growth and overall sentiment may include North America hosting the FIFA World Cup 2026 and celebrations surrounding the 250th anniversary of U.S. independence.

Despite seeing disinflationary progress – especially within oil prices and the critical housing component – we think inflation is likely to stay above the Federal Reserve’s (Fed) target due to upward pressure from delayed tariff impacts and sticky services prices. We expect inflation to remain in the 2.6%-3.0% range.

2. Monetary policy and rates

Given our view that inflation will remain sticky, we think investors may be best positioned on the short end of the yield curve, where we believe one can take advantage of further curve steepening.

In our view, this positioning may also better shield portfolios from increases in term premiums on the long end due to potential concerns surrounding Fed independence, as well as large and continued fiscal deficit spending, with the Fed seemingly willing to let inflation run higher than target.

The U.S. central bank is walking a fine line on easing to support a softening labor market while guarding against a resurgence in inflation. With September’s delayed jobs report beating expectations, the likelihood of a cut at the December meeting has become less certain.

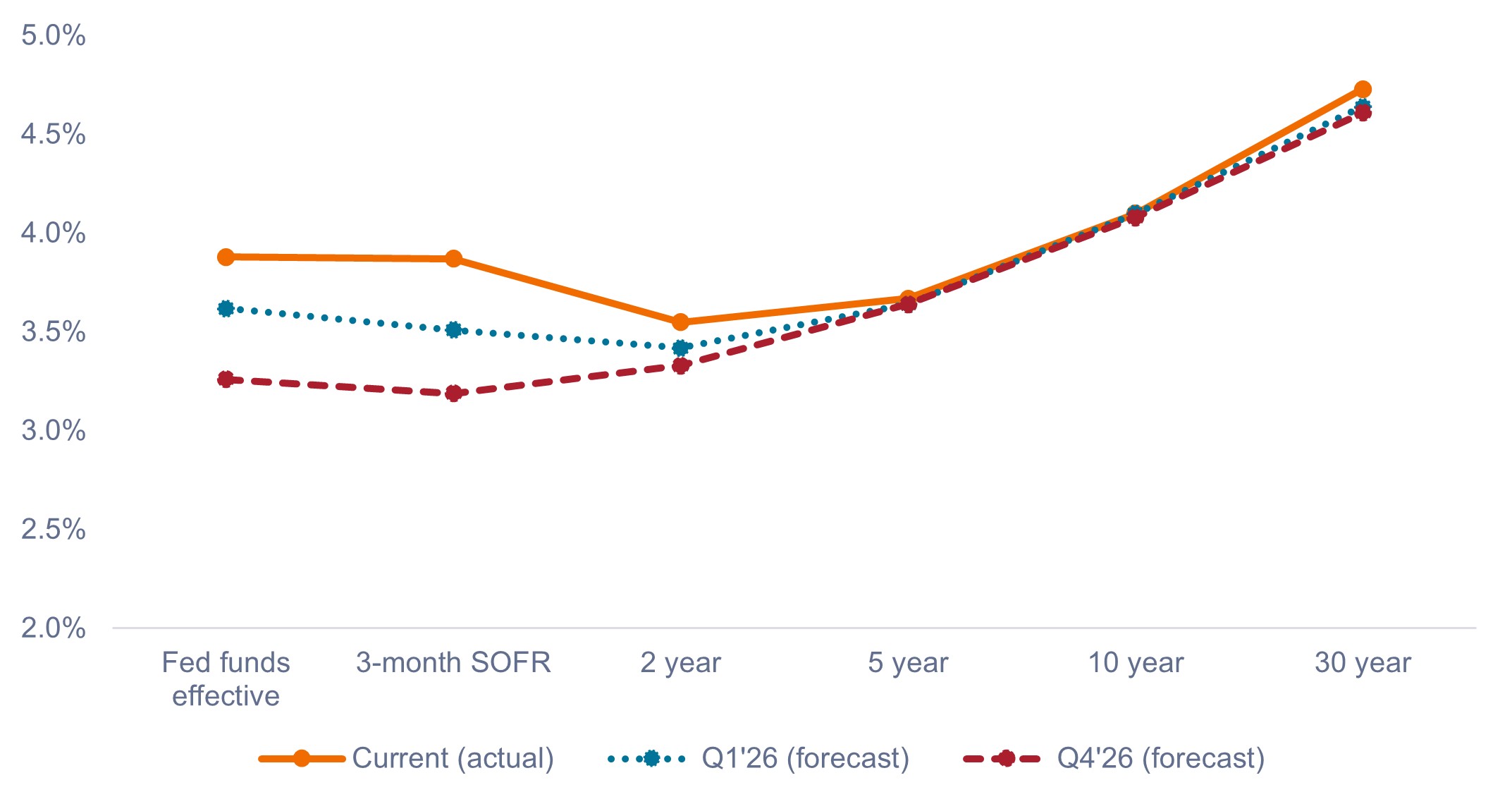

Notwithstanding uncertainty surrounding the Fed’s December decision, the market is pricing in at least three cuts by the end of 2026 (which would bring the federal funds rate down to the 3.25%–3.50% range). We expect the yield curve to steepen, with front-end rates declining and long-end yields staying rangebound amid debt overhang and inflation concerns, as shown in Exhibit 2.

Exhibit 2: U.S. Treasury yield curves (actual vs. forecast)

Short-term yields are expected to come down, with little change to the long end.

Source: Bloomberg, as of 21 November 2025. Yield curve forecasts based on Bloomberg consensus forecasts.

Other positive drivers for fixed income markets include the Fed ending its quantitative tightening (QT) program, together with the likelihood that the “Fed put” is firmly back in place. If we see weakness in the economy, we think the central bank will ease aggressively, which would be supportive of spreads.

Another interesting phenomenon that may continue to take shape in 2026 is that unemployment could remain weak while the growth outlook remains strong. With tighter immigration policy, the labor market can ostensibly sustain equilibrium with a much lower number of jobs created. Meanwhile AI productivity improvements could lead to higher unemployment coupled with higher economic growth.

We believe this dynamic will be supportive of continued Fed cuts, while a lower policy rate should benefit cyclical sectors and business creation.

3. Fixed income themes and positioning

- Bullish on credit spread carry: While credit spreads are hovering around their cyclical tight levels, we believe current valuations are supported by robust corporate profitability, expected Fed easing, and economic growth, fueled in part by AI-driven investments.

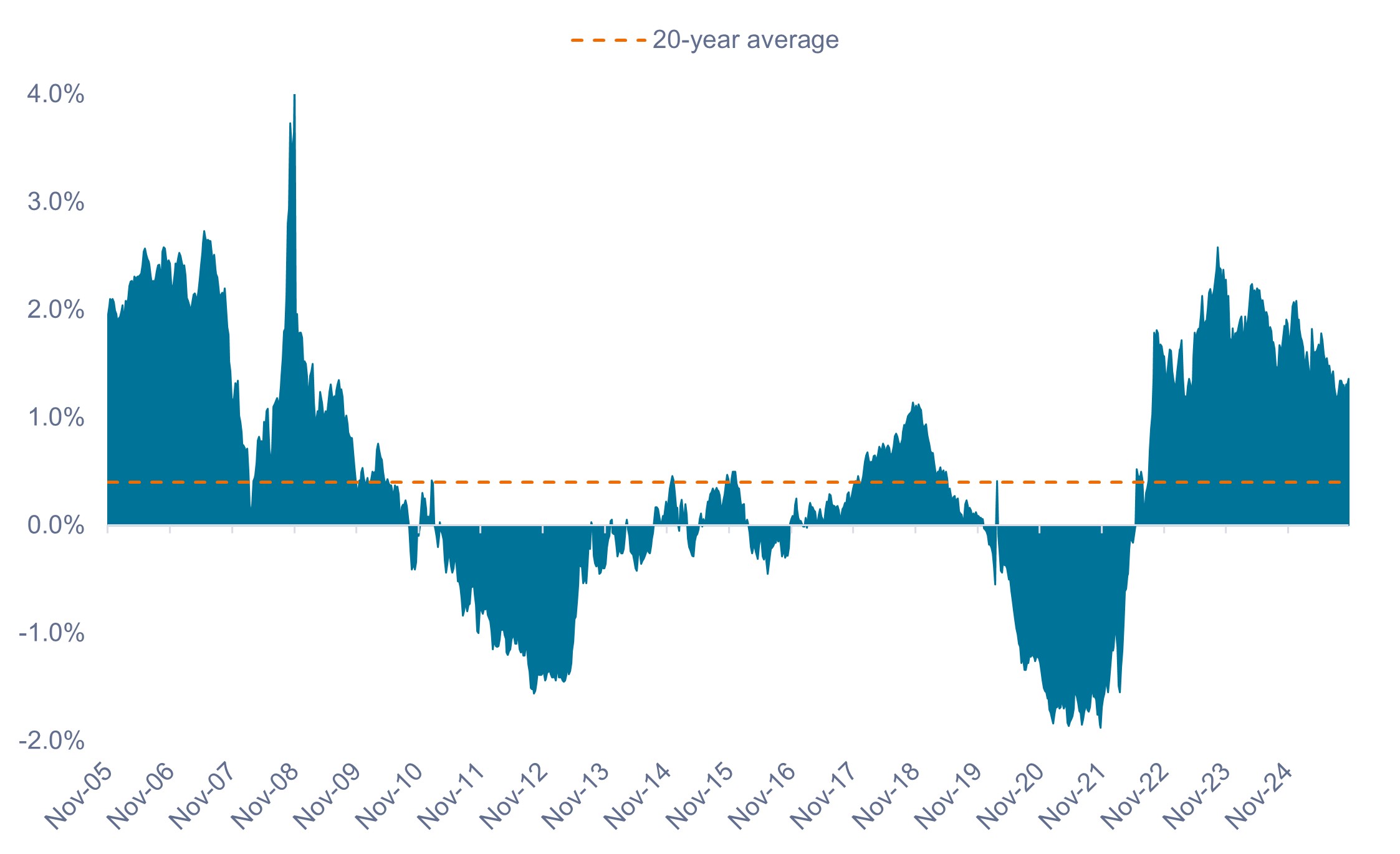

- Real yields remain firmly positive: Despite spreads trading at historically tight levels, overall real yields remain above 1.25%, providing a solid foundation for positive inflation-adjusted returns for bond investors.

Exhibit 3: U.S. 5-year real Treasury yield (2005-2025)

Real Treasury yields remain positive and well above their 20-year average.

Source: Bloomberg, as of 20 November 2025. Past performance is no guarantee of future results.

- Securitized spreads continue to look attractive relative to corporates: Attractive valuations and strong credit quality within securitized sectors support our positive view on securitized credit, and ties into the theme of maximizing carry per unit of risk.

- Active management and flexibility are paramount: With policy uncertainty and uneven growth, a dynamic, diversified approach is essential. Volatility is likely to create opportunities across sectors and geographies. Maximizing carry per unit of risk will be key, while also seeking out idiosyncratic opportunities to add value.

In summary

U.S. growth and AI-driven investment should support a constructive macro backdrop, while sticky inflation and expected Fed cuts point to a steeper yield curve. In our view, attractive opportunities in credit and securitized sectors, combined with positive real yields, make active management essential for 2026.

IMPORTANT INFORMATION

Actively managed investment portfolios are subject to the risk that the investment strategies and research process employed may fail to produce the intended results. Accordingly, a portfolio may underperform its benchmark index or other investment products with similar investment objectives.

Fixed income securities are subject to interest rate, inflation, credit and default risk. The bond market is volatile. As interest rates rise, bond prices usually fall, and vice versa. The return of principal is not guaranteed, and prices may decline if an issuer fails to make timely payments or its credit strength weakens.

Diversification neither assures a profit nor eliminates the risk of experiencing investment losses.

Securitized products, such as mortgage- and asset-backed securities, are more sensitive to interest rate changes, have extension and prepayment risk, and are subject to more credit, valuation and liquidity risk than other fixed-income securities.

U.S. Treasury securities are direct debt obligations issued by the U.S. Government. With government bonds, the investor is a creditor of the government. Treasury Bills and U.S. Government Bonds are guaranteed by the full faith and credit of the United States government, are generally considered to be free of credit risk and typically carry lower yields than other securities.

Carry is the excess income earned from holding a higher yielding security relative to another.

Credit Spread is the difference in yield between securities with similar maturity but different credit quality. Widening spreads generally indicate deteriorating creditworthiness of corporate borrowers, and narrowing indicate improving.

Monetary Policy refers to the policies of a central bank, aimed at influencing the level of inflation and growth in an economy. It includes controlling interest rates and the supply of money.

Quantitative tightening (QT) is a contractionary monetary policy tool applied by central banks to decrease the amount of liquidity or money supply in the economy.

Real yields are the return on an investment after accounting for the loss of purchasing power due to inflation.

Risk assets: Financial securities that may be subject to significant price movements (ie. carrying a greater degree of risk). Examples include equities, commodities, property lower-quality bonds or some currencies.

Volatility measures risk using the dispersion of returns for a given investment.

The yield curve is a graph that plots the yields of U.S. government bonds with different maturities at a single point in time. It is used to visualize the relationship between the interest rates (yields) and the time until the bonds mature, providing insights into economic expectations.

These are the views of the author at the time of publication and may differ from the views of other individuals/teams at Janus Henderson Investors. References made to individual securities do not constitute a recommendation to buy, sell or hold any security, investment strategy or market sector, and should not be assumed to be profitable. Janus Henderson Investors, its affiliated advisor, or its employees, may have a position in the securities mentioned.

Past performance does not predict future returns. The value of an investment and the income from it can fall as well as rise and you may not get back the amount originally invested.

The information in this article does not qualify as an investment recommendation.

There is no guarantee that past trends will continue, or forecasts will be realised.

Marketing Communication.

Important information

Please read the following important information regarding funds related to this article.

- An issuer of a bond (or money market instrument) may become unable or unwilling to pay interest or repay capital to the Fund. If this happens or the market perceives this may happen, the value of the bond will fall.

- When interest rates rise (or fall), the prices of different securities will be affected differently. In particular, bond values generally fall when interest rates rise (or are expected to rise). This risk is typically greater the longer the maturity of a bond investment.

- The Fund invests in high yield (non-investment grade) bonds and while these generally offer higher rates of interest than investment grade bonds, they are more speculative and more sensitive to adverse changes in market conditions.

- Some bonds (callable bonds) allow their issuers the right to repay capital early or to extend the maturity. Issuers may exercise these rights when favourable to them and as a result the value of the Fund may be impacted.

- If a Fund has a high exposure to a particular country or geographical region it carries a higher level of risk than a Fund which is more broadly diversified.

- The Fund may use derivatives to help achieve its investment objective. This can result in leverage (higher levels of debt), which can magnify an investment outcome. Gains or losses to the Fund may therefore be greater than the cost of the derivative. Derivatives also introduce other risks, in particular, that a derivative counterparty may not meet its contractual obligations.

- When the Fund, or a share/unit class, seeks to mitigate exchange rate movements of a currency relative to the base currency (hedge), the hedging strategy itself may positively or negatively impact the value of the Fund due to differences in short-term interest rates between the currencies.

- Securities within the Fund could become hard to value or to sell at a desired time and price, especially in extreme market conditions when asset prices may be falling, increasing the risk of investment losses.

- The Fund may incur a higher level of transaction costs as a result of investing in less actively traded or less developed markets compared to a fund that invests in more active/developed markets.

- Some or all of the ongoing charges may be taken from capital, which may erode capital or reduce potential for capital growth.

- The Fund could lose money if a counterparty with which the Fund trades becomes unwilling or unable to meet its obligations, or as a result of failure or delay in operational processes or the failure of a third party provider.

- In addition to income, this share class may distribute realised and unrealised capital gains and original capital invested. Fees, charges and expenses are also deducted from capital. Both factors may result in capital erosion and reduced potential for capital growth. Investors should also note that distributions of this nature may be treated (and taxable) as income depending on local tax legislation.

- The Fund invests in Asset-Backed Securities (ABS) and other forms of securitised investments, which may be subject to greater credit / default, liquidity, interest rate and prepayment and extension risks, compared to other investments such as government or corporate issued bonds and this may negatively impact the realised return on investment in the securities.