Jennifer James, Lead Analyst within the Emerging Market Debt team, looks at the importance of China both for developed and emerging market growth.

If you had to pick between two economies, the Netherlands and Saudi Arabia, which would it be?

Why the question? Well, at the second session of China’s 13th National People’s Congress that concluded in March 2019, Chinese annual economic growth (real gross domestic product) was downgraded from 6.5% to 6.0-6.5%. To get a sense of what those numbers mean, growth of 6.5% adds an economy about the size of the Netherlands to China’s existing economy, while growth of 6% adds one about the size of Saudi Arabia1. Whichever way you look, those are big figures. Only the US, when it is firing on all cylinders, comes close.

Piece of the pie

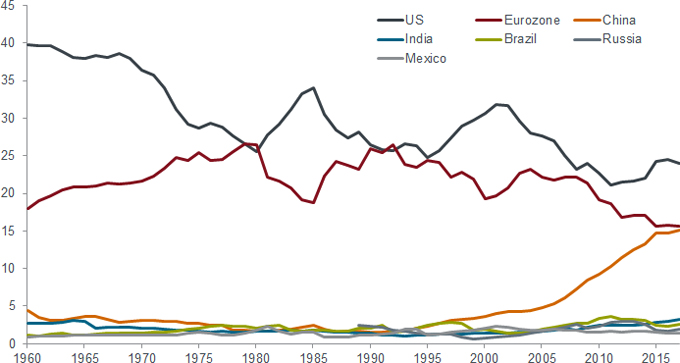

Figure 1 shows the percentage contribution to global gross domestic product (GDP) of the US, the eurozone, China and several emerging market countries. The first thing to notice is that there is an inverse relationship between the eurozone and the US. Such was the size of these two economic powerhouses that when one was outperforming it tended to push down the relative weighting of the other. What is clear is that since its ascendancy 30 years ago, China has been taking share away from both the US and the eurozone as evidenced in their lower peaks. In fact, the International Monetary Fund predicts that by 2030, China will overtake the US to become the largest economy in the world2.

Selected countries and regions share of global GDP (%)

[caption id=”attachment_74579″ align=”alignnone” width=”680″] Source: Bloomberg, World Bank GDP in current USD, latest available figures to end 2017.[/caption]

Source: Bloomberg, World Bank GDP in current USD, latest available figures to end 2017.[/caption]

For Europe, this competitive threat is less disconcerting: it is a long time since a single European country held top spot, but for the US — the world’s existing economic hegemon — it is a source of wounded pride and helps explain why the US has engaged in a trade stand-off with China.

Borrowing slogans

Should investors fear an escalation of the US-China trade war? For all the posturing, neither side wants to escalate the current spat. First, the US may have an unpredictable leader but there is an election in 2020 and President Trump will not want to face the electorate with a downturn in the economy. In 2018, the US’ trade gap with China reached a record high despite tariffs on US$250 billion of Chinese goods, so it is questionable whether the tariffs are having much effect other than raise prices for US consumers.

Second, any escalation of the trade war would see China borrow the ‘America First’ slogan and orientate it to ‘China First’, which would translate into support for domestically-focused Chinese companies. China is not short of firepower to shore up demand. The latest Congress saw VAT cuts announced (3% off the manufacturing rate and 1% off the construction and transport rate) that is part of a RMB 2 trillion (US$298 billion) package to cut costs for businesses and put money back in Chinese consumers’ pockets. This comes on top of recent cuts to the spread premium that local governments must pay to issue debt, making it easier for them to issue debt for infrastructure investment. What is more, unlike in the West, the monetary arsenal is far from exhausted, with China’s key policy rate (the major loan rate) at 4.35%, which has been held since October 2015, giving plenty of room to loosen policy with conventional interest rates.

High speed to high quality

More challenging for western economies is that China is intent on shifting its economic model up the quality scale. With more than 800 million regular internet users in 2018 according to the China Internet Information Center, it already has an internet base nearly three times the size of the US, allowing domestic companies to incubate at size before launching into the wider world. This domestic market size advantage goes some way to explaining why China has an equivalent of Facebook (Tencent’s WeChat) and Amazon (Alibaba), yet Europe, with its linguistic and cultural disparity, does not. Companies like Alibaba and Tencent have low levels of net debt and can provide investors with exposure to a sector with near-inelastic demand. The tech sector in China, however, is prone to policy changes, so while policy has allowed these companies to grow rapidly in the past, it could also be a headwind in the future.

Rapid development has come at a price as attested by the pollution and environmental degradation within China, but even here China is moving at speed. It is already the world’s largest producer of electric vehicles, with sales exceeding one million vehicles in 2018, and a new initiative (new energy vehicle credits) launched this year will mean that car manufacturers will be penalised unless they meet low emission quotas or buy credits off manufacturers that do. It is literally a carrot and stick approach to changing behaviour.

Command economy

This capacity to rapidly manipulate the economy is one of China’s great strengths. There is a strong political desire for stability — born of the preservation instinct of the ruling Communist party — so if the authorities proclaim 6% growth, then that is what they will aim to achieve. Yes, the data may be suspect, but naysayers have been decrying China for years, yet the country continues tangibly to deliver.

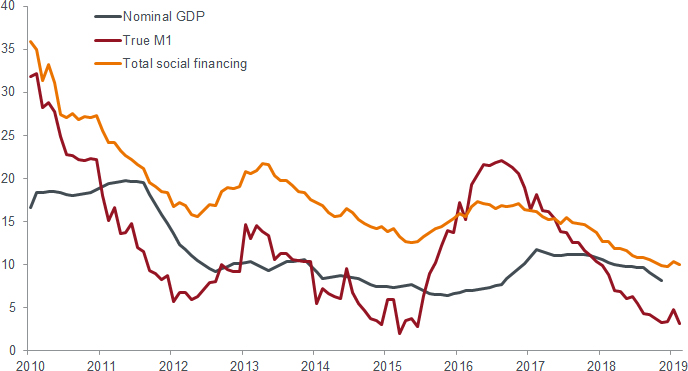

It is worth remembering that China has deliberately been trying to deleverage the economy in the past two years. Coupled with western countries removing some of their policy accommodation, some decline in GDP is to be expected and this is showing through in the data as seen in Figure 2. The Chinese authorities have only latterly begun to relax some of the tighter policies so with the usual time lag between these initiatives and it translating into growth, conditions in China and the rest of the world may get worse in the coming months before they begin to improve. This is reflected in weakness in economies that have a high beta with Chinese growth including Australia, Germany and emerging market commodity suppliers.

Figure 2: China nominal GDP, money and financing (% change year-on-year)

[caption id=”attachment_74568″ align=”alignnone” width=”688″] Source: Thomson Reuters Datastream, 31 January 2010 to 28 February 2019. M1 is narrow money. Total social financing (TSF) is a credit and liquidity measure that reflects total funds provided by China’s domestic financial system to the private sector of the real economy.[/caption]

Source: Thomson Reuters Datastream, 31 January 2010 to 28 February 2019. M1 is narrow money. Total social financing (TSF) is a credit and liquidity measure that reflects total funds provided by China’s domestic financial system to the private sector of the real economy.[/caption]

Chinese banks play a unique role in implementing growth targets. The central bank has been cutting the reserve requirement ratio (RRR) and the market expects several more cuts this year. The effect of the RRR cuts is to allow the banks to have more capacity to lend, essentially putting more money into the system. Banks like Bank of China, China Construction Bank, ICBC and Bank of Communications are considered ‘pillar banks’ by the government. Although these banks have partial listings, they are effectively controlled by the government. As such, these banks have strong balance sheets, high coverage ratios and a managed bad debt balance.

A lot of attention has focused on the Chinese government seeking to slow the property market but this has been directed at speculative buyers. The government is still keen for urbanisation to progress, ie, first-time buyers moving from the land into towns and cities. This is not for altruistic purposes but to encourage more work and economic development: city workers who buy houses help support infrastructure and consumer spending. The authorities are cutting rates to promote this and have delegated housing to the provinces.

We view the bonds of property developers as an area of value. Some 8.1% of the JP Morgan Corporate Emerging Markets Bond Index (CEMBI) Broad Diversified is China (which is investment grade rated) but Chinese property developers, which represent 1.7% of the index, are mostly high yield. With around 30 issuers in this space, we prefer large- and mid-scale developers in Tier 1 and 2 cities (these are the larger cities). In particular, we like the builders in the Greater Bay Area (GBA), a megalopolis that links Macau and Hong Kong with southern coastal cities that has been targeted as a growth area for finance, trade, shipping and tech/innovation. Builders with high exposure to the GBA include Agile and Logan. Agile 2021 bonds were issued at 8.50% yield in July 2018, and these bonds are now yielding 5.6% yield to worst (Bloomberg, as at 21 March 2018), reflecting the company’s deleveraging, strong order backlog, and an improvement in bond technicals. We believe value remains in this space, with the bonds offering strong carry with upside potential. For investors concerned about the geopolitics of trade wars, Chinese property is a domestic growth story that is nearly immune from the machinations of the trade negotiations.

Supply chains

More globally, China remains pivotal for many other emerging economies. While China is a large country, its appetite for resources means its reserves to production ratios for key commodities are quite low. Instead, it relies on imports for many commodities, existing in a symbiotic relationship with the wider global economy. This creates opportunities for many commodity producers such as Brazilian soybean and meat farmers, iron ore producers from around the world and oil/petroleum product exporters. Meanwhile, surplus Chinese savings, together with a desire to secure global supply chains with other countries has made China a major international creditor. For example, within the continent of Africa, seventeen countries now owe between 5% and 25% of their GDP to Chinese banks (IMF staff estimates, 2017). This is likely to deepen as China pursues its Belt and Road Initiative, which seeks to enhance connectivity.

In our view, the global slowdown is symptomatic of the two leading economies — the US and China — having tightened policy in the last two years. The pendulum may now have swung as far as it can in the tightening direction, with policy pausing or moving back towards easing mode. Ultimately, China will do whatever it takes to meet its growth targets and that should be supportive for the global economy.

1Source: Janus Henderson using World Bank national accounts data, GDP current prices USD for 2017.

2Source: IMF, People’s Republic of China, Article IV consultation, 26 July 2018

These are the views of the author at the time of publication and may differ from the views of other individuals/teams at Janus Henderson Investors. References made to individual securities do not constitute a recommendation to buy, sell or hold any security, investment strategy or market sector, and should not be assumed to be profitable. Janus Henderson Investors, its affiliated advisor, or its employees, may have a position in the securities mentioned.

Past performance does not predict future returns. The value of an investment and the income from it can fall as well as rise and you may not get back the amount originally invested.

The information in this article does not qualify as an investment recommendation.

There is no guarantee that past trends will continue, or forecasts will be realised.

Marketing Communication.