Key takeaways:

- AI innovation continues apace, with agentic AI nearing an inflection point. Reasoning models and AI agents are expanding use cases and materially increasing compute demand, but this has led to debates around funding versus revenues.

- Compared to the internet era, today’s capex appears more sustainable than past tech cycles. Meanwhile, some areas looked upon as circular financing – financing that is unsustainable – are supported by hyperscaler balance sheets rather than mere speculative financing.

- In a ‘winner‑takes‑most landscape’, active investing is critical to identify companies with underappreciated future earnings growth and to navigate the key risks.

AI is a work in progress

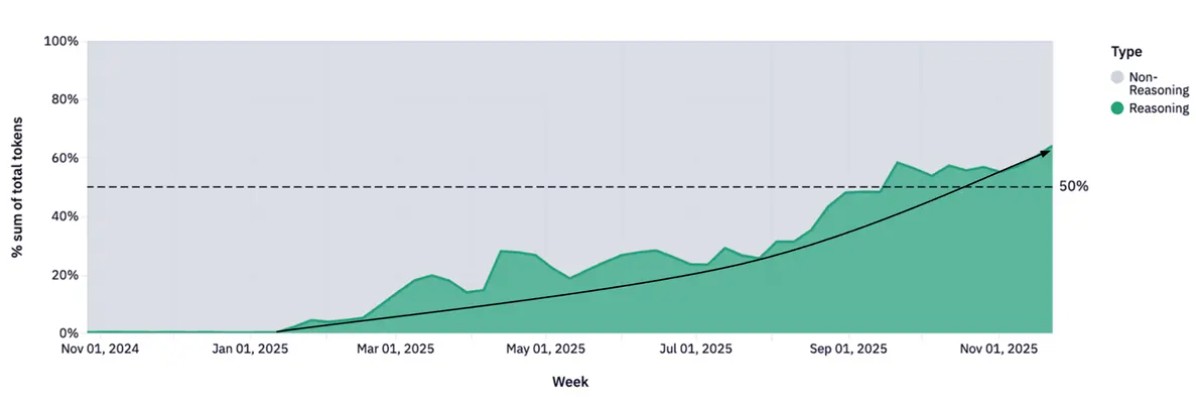

When we talk about AI, it is a dynamic conversation. In the wake of DeepSeek a year ago, we opined that this was the ‘coming out party’ for much more intelligent, capable and cheaper reasoning models that would take AI use cases to the next level. But this would require 10x the compute, hence instead of the market consensus that we would need less compute post-DeepSeek, it was our assertion that exponentially more is required. By the end of 2025, reasoning models accounted for more than 50% of all tokens processed from zero at the beginning of the year,1 while AI capital expenditure (capex) took another major step up.

Figure 1: Reasoning models now represent more than half of token usage

Reasoning vs non-reasoning token trends over time

Source: Openrouter.AI; An Empirical 100 Trillion Token Study with OpenRouter; December 2025.

Agentic AI is nearing an inflection point

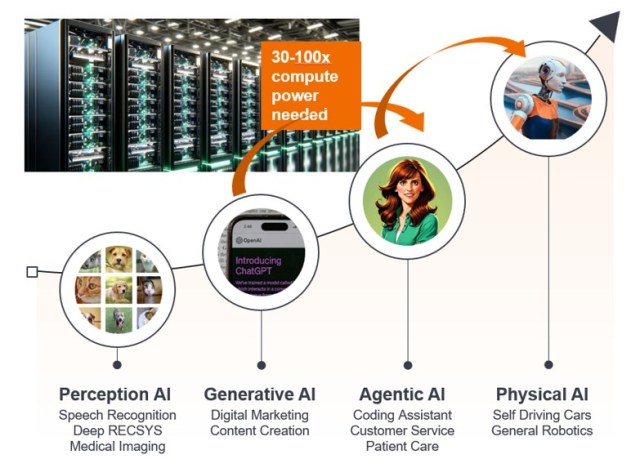

We believe we are now on the cusp of the next major inflection – agentic AI (autonomous decision-making and action) is manifesting both in the digital world as AI agents, as well as the physical world in autonomous vehicles and humanoids. Several profound technological unlocks are converging to create the potential for AI innovation to accelerate rather than slow down. AI coding agents are said to have now surpassed human capabilities, and is accelerating the development curve of large language models (LLMs) as highlighted in a recent essay from Dario Amodei, the CEO of Anthropic.2 Throw in the fact that we will soon see LLMs trained on the latest Blackwell infrastructure from mid-2026 – the stage is set for a faster innovation curve with the ability to code and compute much faster. Every LLM that we have seen to-date, including Gemini 3 and ChatGPT 5.2 were all trained on a variant of NVIDIA’s Hopper chip. By the time we get to LLMs trained on the most advanced chip, Vera Rubin Ultra (slated for 2028), AI infrastructure could be around 400x faster, enabling exponentially speedier training runs and feedback loops.3

Figure 2: AI evolution expands use cases

Source: Janus Henderson Investors.

The dawn of the agentic AI era

What will a faster AI development curve look like? Again the key area we are focused on is agentic AI, where AI agents mimic human decision-making to solve problems in real time, making them much more powerful than copilots being unleashed from human oversight and restraint. The challenge for a reasoning model and for any AI agent has been the context window and the horizon of the thought chain i.e. AI agents were like humans with short-term memory loss so while they could work very fast, they soon forgot what their goal was. There is a huge amount of ongoing innovation in the industry to address that via longer context windows (Google Gemini was the first to be able to accept 1 million tokens or 1,500 pages of text)4 and horizons utilising a variety of techniques from a sparse mixture of experts to reinforcement learning, to agent harnesses that guides how that agent behaves in a real-world setting.

AI’s ability to complete long horizon tasks looks to be roughly doubling every seven months. Hence why Anthropic commented that its coding agents have advanced from barely being able to write a line of code to being superior to its own best programmers all within the space of just three years, and the focus on ‘AI is eating software’ narrative. This important because of the potential productivity gains AI agents can deliver. McKinsey & Co. have talked about having a ‘workforce’ of approximately 65,000 comprising 40,000 humans and 25,000 agents.5 Unlike a human workforce there is no demographic limit on the number of agents that can be deployed. It has been estimated that if you extrapolate the curve of progress, AI agents may be able to reliably match a human’s daily workload in 2028, do a year’s work in a day by 2034 and a full century of human work in a day by 2037 – this will have profound implications for white collar work and related industries.

Unlocking of physical AI

The other major area of development is in physical AI. At CES 2026, the major consumer tech event, NVIDIA CEO Jensen Huang talked about a ‘ChatGPT moment’ for physical AI. Similarly to agentic AI, the technological unlock are LLM reasoning models as well as AI factories that enable limitless synthetic data to be created to make up for the lack of real-world data for autonomous driving and robots outside of factories.

ChatGPT was able to learn by scraping all the text, images and video off the internet. But there is no similar dataset for physical AI to understand real word forces such as gravity, friction and momentum or to deal with all the daily ‘corner cases’ (those that occur outside normal operating parameters with multiple variables and conditions) that are encountered in the real world.

British startup Wayve Technologies, one of the first next generation AI driving algorithm platforms, is using an end-to-end learning model rather than a traditional modular rules-based driving system. The company believes its software can learn to drive in the US on the other side of the road (British left, US right) with different driving rules in a matter of weeks, not years. As a result, we are seeing wider testing and rollout of robotaxis, with Waymo aiming to be present in most US cities by end-2026, and launching in London and Tokyo as well. Meanwhile, Tesla and Chinese companies such as PonyAI and WeRide also have ambitious plans globally.

We now see robots moving more gracefully, breakdancing and performing martial arts while performing more intelligent tasks such as putting groceries away in the fridge and other household chores. While a little more distant versus the progress we are seeing in say agentic AI-powered chatbots or autonomous driving, humanoids are now on the horizon. It is hoped that humanoids will help alleviate the demographic challenge facing us, as there will be only about two working-age people for every dependent (age over 65) in most developed countries as well as China by 2050. Humanoids are the robotic AI solution that can supply the workforce needed for manufacturing, services and helping a growing elderly population.

Active investment in AI requires being cognisant of the key risks

Being investors rather than futurologists, we constantly consider about the risks within the AI tech wave. Starting with technological development, we think about financing, and ultimately how companies will be rewarded for that and be able to monetise. As investors, in the back of our minds and what drives our investment thinking and decisions is that a company that never makes a profit is worth zero.

AI technological development is progressing well albeit requires constant, dynamic evaluation as to whether scaling laws are still working and whether new unlocks continue to enable next-generation capabilities. The market has rightly focused on the sustainability of AI financing given the huge capex we’ve witnessed in recent years, memories of the dotcom bubble and concerns around some areas of circular financing.

However, today we are in a very different place in terms of financing this capex. The vast majority of AI capital spending is from US hyperscalers who are funding this spend from profits and free cash flow (FCF) and net cash balance sheets, as well as enterprises and sovereigns (governments),6 which account for most of NVIDIA’s business today. But we see risks as being more elevated in the new entrant start up bucket that will become a growing proportion of spend in the years to come.

While the market has some misconceptions around funding and revenues, we view ChatGPT creator, OpenAI as having the highest risk of the high-profile new entrants. But the company does appear to have a credible pathway to generating hundreds of billions in revenues, which gives it the scale to be more flexible in terms of its financing needs. And recently, it appears to have taken a more pragmatic view around funding and revenue, reportedly scaled down its funding commitments from US$1.4 trillion to US$600 billion over the next four years.7 Meanwhile, Anthropic looks to be on track to be cashflow positive in 2028, mainly thanks to the success of Claude Code.8

We continue to see supportive financing channels for these companies that require external financing with Anthropic recently securing new funding taking it to a US$380 billion valuation8 and OpenAI announcing an up to US$110 billion blockbuster funding round,9 and potentially an initial public offering (IPO) at the end of the year. While some funding deals are indeed circular, with the US hyperscalers and NVIDIA looking to participate, they are likely to represent a small proportion of Anthropic and OpenAI’s future capex and operating expenditure (cloud contract) commitments.

NVIDIA has also made the point that investing part of its expected strong growth in FCF in some leading new AI companies is not unreasonable. Unlike the internet era when Facebook was able to buy Instagram and WhatsApp and Google to buy YouTube and Android, the stricter current regulatory environment does not allow for this, hence buying stakes in companies is the next best approach.

AI bubble: Fact or fizz?

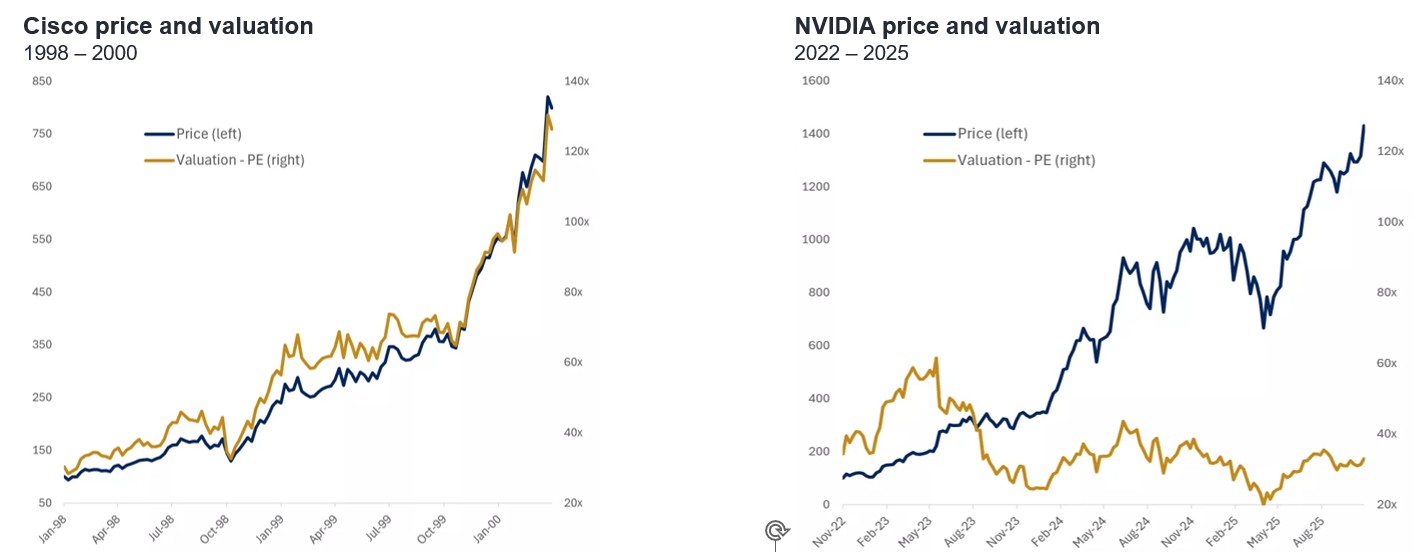

There are key differences between today and 2000. In 1999, there were about 20 large cap technology stocks that went up more than 900% powering the Nasdaq to a circa 100% move in only a few months.10

Figure 3: This is not 2000 – it’s hard to call a bubble when everyone is warning we’re in a bubble

Source: Janus Henderson Investors, FactSet, Edward Jones, as at 30 September 2025. Note: Use of third party names, marks or logos is purely for illustrative purposes and does not imply any association between any third party and Janus Henderson Investors, nor any endorsement or recommendation by or of any third party. Unless stated otherwise, trademarks are the exclusive property of their respective owners. References made to individual securities do not constitute a recommendation to buy, sell or hold any security, investment strategy or market sector, and should not be assumed to be profitable. Janus Henderson Investors, its affiliated advisor, or its employees, may have a position in the securities mentioned. Exposures are subject to change without notice.

A lot of that stock movement came from valuation given earnings growth did not keep pace e.g. Cisco hit well over 120x Price-to-earnings (P/E) ratio (Figure 3). It is a very different story today with NVIDIA that trades on a forward P/E of around 25 to 30x, not too dissimilar a valuation as McDonald’s for a different type of chip!11 It is very hard to have a bubble when everyone is worrying about a bubble, and is concerned about whether AI will live up to its huge expectations and capex sustainability.

We have highlighted before that there is always a time lag between capex, growth in usage and monetisation similar to what we experienced in the internet era; understandably, markets are often overly impatient. Stock valuation metrics like P/E are market opinion, not facts, especially in the technology sector where consensus can be significantly wrong. We believe the key to harnessing the investment opportunity of AI is via active investing, to find companies that we think the market has yet to fully appreciate its future earnings growth, and as a result could be trading at cheaper valuations today versus its future growth trajectory.

The challenging part is this being a ‘winner takes most’ industry, the vast majority of profits will accrue to only a few companies. Hence the challenge of using thematic exchange traded funds (ETFs) is that they may have many stocks that have no connection to the underlying theme; but more importantly, may never make incremental profit from the theme, and therefore are unlikely to deliver sustainable growth.

As a team we remain focused on identifying unexpected earnings growth – major new technology waves like AI or new themes are great hunting grounds for stock pickers, but we believe the best investment outcome is likely to be from a high conviction portfolio of real winners, rather than a portfolio of hundreds of stocks.

1 Sequoiacap.com; ‘This is AGI’; accessed February 2026.

2 DarioAmodei.com, ‘the Adolescence of Technology’, January 2026.

3 NVIDIA GTC event presentation, March 2025.

4 Gemini.google.com; What Gemini can do; accessed 2 March 2026.

5 Business Insider; ‘McKinsey CEO Bob Sternfels says the firm now has 60,000 employees: 25,000 of them are AI agents’; 12 January 2026.

6 Andreesen Horowitz LinkedIn post; ‘AI capex is massive, but sustainable’, January 2026.

7 CNBC.com, ‘OpenAI resets spending expectations, tells investors compute target is around $600 billion by 2030’, 20 February 2026.

8 Forbes.com, ‘Anthropic: The $380 Billion Powerhouse Hiding In Plain Sight’, 13 February 2026.

9 FT.com; OpenAI secures up to $110 bn in record funding deal; 27 February 2026.

10 Goldman Sachs; 25 Years on; Lessons from the bursting of the technology bubble; 27 March 2025.

11 Bloomberg; NVDA vs MCD 12m forward P/E as at 26 February 2026. Past performance does not predict future returns.

Agent harness: Software infrastructure that wraps around an AI model, providing the environment for the brain with the tools, memories, and safety limits it needs to function in a real-world setting.

Agentic AI: An AI system that uses sophisticated reasoning and iterative planning to autonomously solve complex, multi-step problems. Vast amounts of data from multiple data sources and third-party applications are used to independently analyse challenges, develop strategies and execute tasks.

Capital expenditure (capex): Money a business spends on major, long-term assets such as property and equipment (tangible assets) or technology, software, trademarks, patents etc (intangible assets) to facilitate new projects or investments that support business growth and expansion.

Circular financing: Concerns that financing of AI infrastructure investment among mega caps is becoming unsustainable. Interconnected deals and investments within a small group of companies means companies are investing in each other, with the funding recipient using the capital to make purchases from the original investor. Some of these companies may have insufficient cash flows and it could lead to a bubble when company valuations become excessive, with broader market implications.

End-to-end learning model: Unlike a traditional learning model, an end-to-end model (typically a deep neural network) handles learning tasks simultaneously, learning to transform raw input data (such as images, text, or audio) into the target output (such as classifications, predictions, or actions) in one integrated process.

Exchange Traded Fund (ETF): A security that tracks an index, sector, commodity, or pool of assets (such as an index fund). ETFs trade like an equity on a stock exchange and experience price changes as the underlying assets move up and down in price. ETFs typically have higher daily liquidity and lower fees than actively-managed funds.

Free cash flow: Cash that a company generates after allowing for day-to-day running expenses and capital expenditure. It can then use the cash to make purchases, pay dividends or reduce debt.

High conviction: A strategy where a portfolio holds a select number of stocks that represent the portfolio manager’s best opportunities for outperformance. Fewer holdings mean each stock has a larger impact on under/outperformance. A high-conviction approach can also lead to higher volatility or risk.

Hyperscaler: Companies that provide infrastructure for cloud, networking, and internet services at scale. Examples include Google Cloud, Microsoft Azure, Facebook Infrastructure, Alibaba Cloud, and Amazon Web Services.

Large language model (LLM): A specialised type of artificial intelligence that has been trained on vast amounts of text to understand existing content and generate original content.

Net cash: Refers to the liquidity position of a company calculated by deducting its current liabilities from its cash balance. This includes highly liquid funds that are readily available for disbursement.

Physical AI: Integration of sophisticated AI algorithms into tangible, interactive systems, enabling autonomous machines with cognitive reasoning and spatial knowledge to learn from their interactions and respond in real time. Examples include autonomous vehicles, surgical and humanoid robots.

Price-to-earnings (P/E): A popular stock valuation metric, it measures share price compared to earnings per share.

Reasoning model: Learning models that make use of available information to generate predictions, make inferences and draw conclusions. It involves representing data in a form that a machine can process and understand, then applying logic to arrive at a decision.

Token: AI tokens are the fundamental building blocks of input and output that Large Language Models (LLMs) use. They are the smallest units of data used by a LLM to process and generate text/output that is useful.

These are the views of the author at the time of publication and may differ from the views of other individuals/teams at Janus Henderson Investors. References made to individual securities do not constitute a recommendation to buy, sell or hold any security, investment strategy or market sector, and should not be assumed to be profitable. Janus Henderson Investors, its affiliated advisor, or its employees, may have a position in the securities mentioned.

Past performance does not predict future returns. The value of an investment and the income from it can fall as well as rise and you may not get back the amount originally invested.

The information in this article does not qualify as an investment recommendation.

There is no guarantee that past trends will continue, or forecasts will be realised.

Marketing Communication.

Important information

Please read the following important information regarding funds related to this article.

- Shares/Units can lose value rapidly, and typically involve higher risks than bonds or money market instruments. The value of your investment may fall as a result.

- Shares of small and mid-size companies can be more volatile than shares of larger companies, and at times it may be difficult to value or to sell shares at desired times and prices, increasing the risk of losses.

- If a Fund has a high exposure to a particular country or geographical region it carries a higher level of risk than a Fund which is more broadly diversified.

- The Fund is focused towards particular industries or investment themes and may be heavily impacted by factors such as changes in government regulation, increased price competition, technological advancements and other adverse events.

- The Fund follows a sustainable investment approach, which may cause it to be overweight and/or underweight in certain sectors and thus perform differently than funds that have a similar objective but which do not integrate sustainable investment criteria when selecting securities.

- The Fund may use derivatives with the aim of reducing risk or managing the portfolio more efficiently. However this introduces other risks, in particular, that a derivative counterparty may not meet its contractual obligations.

- If the Fund holds assets in currencies other than the base currency of the Fund, or you invest in a share/unit class of a different currency to the Fund (unless hedged, i.e. mitigated by taking an offsetting position in a related security), the value of your investment may be impacted by changes in exchange rates.

- When the Fund, or a share/unit class, seeks to mitigate exchange rate movements of a currency relative to the base currency (hedge), the hedging strategy itself may positively or negatively impact the value of the Fund due to differences in short-term interest rates between the currencies.

- Securities within the Fund could become hard to value or to sell at a desired time and price, especially in extreme market conditions when asset prices may be falling, increasing the risk of investment losses.

- The Fund could lose money if a counterparty with which the Fund trades becomes unwilling or unable to meet its obligations, or as a result of failure or delay in operational processes or the failure of a third party provider.

Specific risks

- Shares/Units can lose value rapidly, and typically involve higher risks than bonds or money market instruments. The value of your investment may fall as a result.

- If a Fund has a high exposure to a particular country or geographical region it carries a higher level of risk than a Fund which is more broadly diversified.

- The Fund is focused towards particular industries or investment themes and may be heavily impacted by factors such as changes in government regulation, increased price competition, technological advancements and other adverse events.

- This Fund may have a particularly concentrated portfolio relative to its investment universe or other funds in its sector. An adverse event impacting even a small number of holdings could create significant volatility or losses for the Fund.

- The Fund may use derivatives with the aim of reducing risk or managing the portfolio more efficiently. However this introduces other risks, in particular, that a derivative counterparty may not meet its contractual obligations.

- If the Fund holds assets in currencies other than the base currency of the Fund, or you invest in a share/unit class of a different currency to the Fund (unless hedged, i.e. mitigated by taking an offsetting position in a related security), the value of your investment may be impacted by changes in exchange rates.

- When the Fund, or a share/unit class, seeks to mitigate exchange rate movements of a currency relative to the base currency (hedge), the hedging strategy itself may positively or negatively impact the value of the Fund due to differences in short-term interest rates between the currencies.

- Securities within the Fund could become hard to value or to sell at a desired time and price, especially in extreme market conditions when asset prices may be falling, increasing the risk of investment losses.

- The Fund could lose money if a counterparty with which the Fund trades becomes unwilling or unable to meet its obligations, or as a result of failure or delay in operational processes or the failure of a third party provider.