Key takeaways:

- Geopolitics, policy shifts and higher rates have reconnected markets with real-world events, increasing stock market dispersion and challenging long-held diversification assumptions.

- Policy unpredictability and supply chain risks are exposing fragile business models and crowded trades, increasing the risk of sharp reversals for investors relying on consensus positioning.

- Flexible long-short approaches that combine fundamental stock selection with tactical positioning could exploit inefficiencies on both sides, adjusting exposure as conditions change, and aiming to deliver consistent absolute returns.

Over the past year, the gap between global events and market outcomes has narrowed. The news cycle has started to feel more relevant to investors’ portfolios, not because everyone has become a geopolitical expert, but because fast-changing politics and policy are increasingly feeding through to company earnings, valuations, and returns.

In this kind of environment, where it can be almost impossible to predict the next twist in rhetoric or policy, can equity long/short ‘absolute return’ strategies help investors to potentially exploit market efficiencies?

The world feels less predictable

A big shift has been the steady move away from ‘just in time’ globalisation towards something more cautious. Companies have been rethinking where they make things, where they store inventory, and who they partner with for critical components. Terms like repatriation, onshoring and near‑shoring have moved from boardroom jargon to practical decisions in response to concerns over tariffs and supply chain risks. Companies have sought to reduce dependency on a single region or supplier, leading to higher capital spending demands, potentially more complex logistics, and tougher trade-offs between resilience and efficiency.

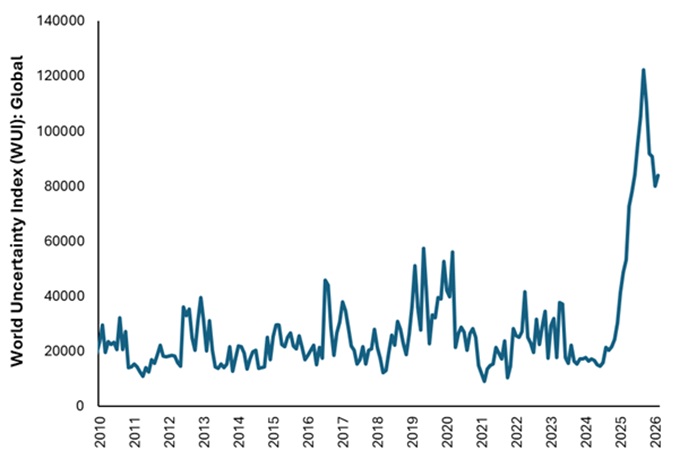

At the same time, uncertainty has also broadened (Exhibit 1). Not as a single risk to monitor, but rather a patchwork of concerns over elections, international alliances and treaties, regional conflicts and populist policy responses.

Exhibit 1: Today’s uncertainty seems broader and more persistent than before

Source: World Uncertainty Index, GDP-weighted average, 1 January 2010 to 31 March 2026.

Note: The WUI is computed by counting the percent of word “uncertain” (or its variants) in the Economist Intelligence Unit country reports, spanning 143 countries, before multiplying by 1,000,000. A higher number indicates higher uncertainty and vice versa. For example, an index of 200 corresponds to the word uncertainty accounting for 0.02 percent of all words.

This has aligned with a renewed focus from governments spanning from security and defence to technology and energy independence, which is changing the economics of whole industries. Artificial intelligence (AI) has arrived as a tangible force across industries, raising questions about its potential impact, and driving both opportunity and disruption.

A wider gap in market outcomes

Alongside the rise in geopolitical uncertainty, there has been a more structural shift in how markets behave. One of the most important changes has been the move away from the era of near-zero interest rates. For years, cheap and abundant capital lifted valuations across markets and gave many businesses room to breathe, without immediate pressure to optimise spending, or to generate sustainable profits. That environment has now changed.

Today, valuations have become more grounded in reality (with exceptions), and investors have become more selective in where they allocate money, reflected in higher stock price dispersion than we have seen since 2009[1]. Companies are under greater pressure to demonstrate real earnings and cash flow. The result is a more disciplined and rational backdrop, where analysis of underlying fundamentals becomes more important.

What this means is that company-specific factors are once again shaping outcomes. Businesses with strong competitive positions, sensible balance sheets, and reliable cash generation seem well positioned to gain traction. Meanwhile, companies with weaker fundamentals or overly optimistic growth assumptions are likely to face greater scrutiny. This environment prioritises the importance of good stock selection, while it augments the value of real diversification.

A consistent way of investing through the noise

While the world has changed, one practical factor has stayed consistent for absolute return investing utilising a long/short approach. Focus on companies, stay flexible, and avoid being forced into a single market outcome.

At its heart is a straightforward idea: rather than relying on markets going up, the objective is to build a portfolio that can find opportunities on both the long and short sides. That typically involves two complementary mindsets working together:

- A fundamental core book, on the long side looking for businesses that can stand up over time, characterised by resilient models, sensible balance sheets, and dependable cash flows. Similarly, on the short side, companies where the outlook is already priced in, where there are structural weaknesses or poor management.

- A tactical overlay, designed to respond when the environment changes, adopting a more trading-oriented mindset to deal with volatility, market anomalies, or fast-moving shifts in market environments, allocating to both long and short positions as suitable.

We believe that this flexibility is extended for those strategies that can adjust net or gross exposure. When visibility is better, investors can lean in, expanding gross exposure to increase market sensitivity. When uncertainty spikes, exposure can be reduced to help mitigate the risk of potential losses, without stepping entirely out of markets.

Absolute return strategies with this kind of built-in adaptability, constructed around a disciplined stock-level process, can help investors to stay engaged without feeling they must make an all-or-nothing call. With the added benefit of low sensitivity to both equities and bonds that characterises a well-managed absolute return strategy.

A long/short, absolute return mindset is designed for a world where outcomes are uneven and surprises are common.

Luke Newman, Portfolio Manager

Riding uncertainty through the cycle

If the past year has taught investors anything, it is that uncertainty does not arrive in neat packages. One month the risks are focused on geopolitics; the next it might be domestic policy, then supply chains, energy prices, or shifting trade relationships. A year ago, we were discussing the risks of trade protectionism (led by US tariffs), and an increasingly fractured international order. Today, a central topic is the consequences to the global economy of the conflict in the Middle East and the winners/losers of AI.

The details change, but the experience is familiar: markets move quickly, narratives swing, and it can feel uncomfortable to stay invested.

That is why consistency of process matters. A long/short, absolute return mindset is designed for a world where outcomes are uneven and surprises are common. It does not depend on a single forecast being right. Instead, it tries to do something more practical: keep decisions anchored in company fundamentals, keep risk adjustable, and keep options open, seeking to exploit market inefficiencies to try and generate positive absolute returns.

No approach removes uncertainty, but a flexible, fundamentals-led, long/short approach aims to make uncertainty more manageable, identifying opportunities on both sides of the market and adjusting exposure when risks rise. The world has changed quickly. The discipline required to navigate it is, if anything, more timeless.

—–

[1] Source: Bloomberg, Janus Henderson Investors, as at 28 November 2025. Dispersion calculated by taking the annual returns of each stock in the MSCI Europe Index and then measuring the standard deviation across all the individual stock returns. Past performance does not predict future returns. There is no guarantee that past trends will continue, or forecasts will be realised.

Absolute return: A type of investment strategy that seeks to generate a positive return over time, regardless of market conditions or the direction of financial markets, typically with a low level of volatility.

Balance sheet: A financial statement that summarises a company’s assets, liabilities and shareholders’ equity at a particular point in time. Each segment gives investors an idea as to what the company owns and owes, as well as the amount invested by shareholders.

Cash flow: The net balance of cash that moves in and out of a company. Positive cash flow shows more money is moving in than out, while negative cash flow means more money is moving out than into the company.

Dispersion: The extent to which a distribution of data points is stretched or squeezed. If the data points cluster around certain values, then dispersion is low, whereas if they are more spread out, then dispersion is high. For example, dispersion in stocks measures the range of returns for a group of stocks. Higher dispersion opens up opportunities for stock pickers to outperform by selecting the winners and avoiding the losers, given that stock returns are spread more widely on either side of the benchmark.

Economic cycle (cycle): The fluctuation of the economy between expansion (growth) and contraction (recession), commonly measured in terms of gross domestic product (GDP). It is influenced by many factors, including household, government and business spending, trade, technology, and central bank policy.

Interest rates: The amount charged for borrowing money, shown as a percentage of the amount owed. Base interest rates (the Bank Rate) are generally set by central banks, such as the Federal Reserve in the US or Bank of England in the UK, and influence the interest rates that lenders charge to access their own lending or saving.

Long: position: A security that is bought with the intention of holding over a long period in the expectation that it will rise in value.

Long/short: A portfolio that can invest in both long and short positions. The intention is to profit from combining long positions in assets in the expectation that they will rise in value, with short positions in assets expected to fall in value. This type of investment strategy has the potential to generate returns regardless of moves in the wider market, although returns are not guaranteed.

Portfolios: A grouping of financial assets such as equities, bonds, commodities, properties, or cash.

Net/gross exposure: The amount of a portfolio’s exposure to the market. Net exposure is calculated by subtracting the amount of short exposure as a percentage of a portfolio from the amount of long exposure. For example, if a portfolio is 100% long and 20% short, net exposure is 80%. Gross exposure is calculated by combining the total value of both long and short positions as a percentage of a portfolio. For example, if a portfolio is 100% long and 20% short, gross exposure is 120%.

Short position (shorting): Fund managers use this technique to borrow then sell what they believe are overvalued assets, with the intention of buying them back for less when the price falls. The position profits if the security falls in value.

Volatility: The rate and extent at which the price of a portfolio, security, or index, moves up and down. If the price swings up and down with large movements, it has high volatility. If the price moves more slowly and to a lesser extent, it has lower volatility. The higher the volatility, the higher the risk of the investment.

These are the views of the author at the time of publication and may differ from the views of other individuals/teams at Janus Henderson Investors. References made to individual securities do not constitute a recommendation to buy, sell or hold any security, investment strategy or market sector, and should not be assumed to be profitable. Janus Henderson Investors, its affiliated advisor, or its employees, may have a position in the securities mentioned.

Past performance does not predict future returns. The value of an investment and the income from it can fall as well as rise and you may not get back the amount originally invested.

The information in this article does not qualify as an investment recommendation.

There is no guarantee that past trends will continue, or forecasts will be realised.

Marketing Communication.

Important information

Please read the following important information regarding funds related to this article.