Key takeaways:

- Oil prices are likely to remain volatile in the near term as markets assess whether the U.S.-Iran ceasefire translates into sustained improvements in shipping security and energy flows through the Strait of Hormuz.

- Even if flows resume, oil prices are unlikely to return to pre‑conflict levels, with lingering geopolitical risk and inventory restocking supporting a higher medium‑term price floor.

- For the energy sector, near-term headline noise does not diminish the longer‑term opportunity, in our view, as strong cash flows and improved balance sheets continue to support the fundamental backdrop.

News of a two‑week ceasefire between Iran and the United States was welcomed by markets, fueling optimism that energy flows through the Strait of Hormuz could begin to normalize. The truce, however, appears fragile at best, as evidenced by events in the immediate aftermath, including reports of continued attacks in the Gulf and Iranian claims that ceasefire conditions had already been violated. Beyond that, questions remain around enforcement, shipping security, and the durability of any relief to supply disruptions.

In the near term, news flow is likely to remain volatile, making the market impact difficult to assess with any degree of accuracy. Over the medium and long term, the episode carries important implications for oil prices, supply dynamics, and the broader energy sector.

Oil prices likely to remain volatile after the knee-jerk pullback

Unsurprisingly, front-month crude prices fell sharply in the wake of the news. If the Strait reopens, even temporarily, a meaningful amount of trapped crude oil and refined products could resume flowing out of the region. That would ease pressure on prices and enable customers to begin restocking inventories that have been drawn down during the disruption.

Directionally, a reopening should mean lower global oil and gas prices. But markets need to see ships actually passing through the Strait safely, and participants need confidence that traffic will not be disrupted again in a matter of days or weeks. Until those conditions are met, oil prices are likely to remain volatile as they react to incremental headlines.

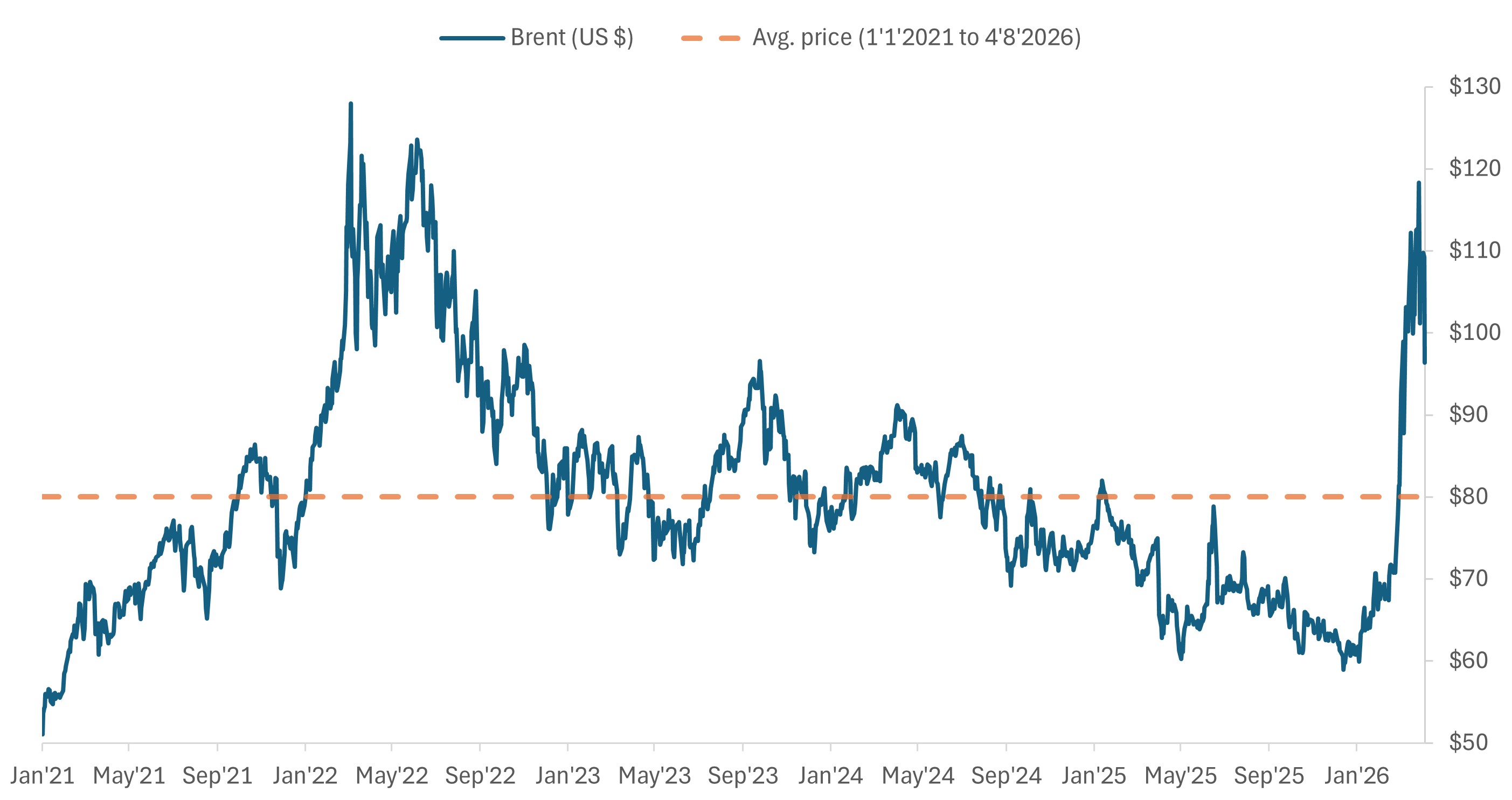

Both Brent and West Texas Intermediate (WTI) crude prices remain well above pre-conflict levels, with the pullback reflecting some easing in immediate supply fears but not a belief that geopolitical risks have been fully resolved.

Even if flows resume, supply normalization will take time

The return to pre‑conflict supply levels in the Middle East will likely be a multi‑month process. Once production restarts, it needs to be done in a controlled manner, and the pace will also vary across the region depending on the extent of damage to key infrastructure. While some countries could be back close to full production in a matter of weeks, others could take more than two months. And even where producing reservoirs themselves are intact, damaged pipelines, processing facilities, or export terminals could delay full resumption.

As for liquefied natural gas (LNG), restoring supply will take longer. LNG production ramps more slowly, given the technical demands of liquefaction facilities. On top of that, damage to key LNG assets is material and could take several years to fully repair.

Assessing the medium-term outlook for oil prices

When considering the outlook for oil prices, it’s important to put recent swings in perspective. We entered the year with an oversupplied market and crude prices at their lowest levels in five years. This provided a buffer to absorb some of the supply shock. That said, we have already worked down much of that surplus.

Even when the Strait of Hormuz reopens, the market is likely to apply a higher supply-risk premium relative to pre-conflict levels. At the same time, a ramp in demand from the necessary restocking of inventories will be an offsetting force to the return of supply.

All of this makes it less likely that oil prices will fall back to the $65 per barrel range anytime soon. In our view, a more realistic medium-term assumption would be something closer to the $80 level, with $70-75 a reasonable floor.

Brent crude prices, front-month future

2026 began with an oversupplied market and oil prices at their lowest since 2021.

Source: Bloomberg, data from 1 January 2021 to 8 April 2026. Past performance is not a guarantee of future results.

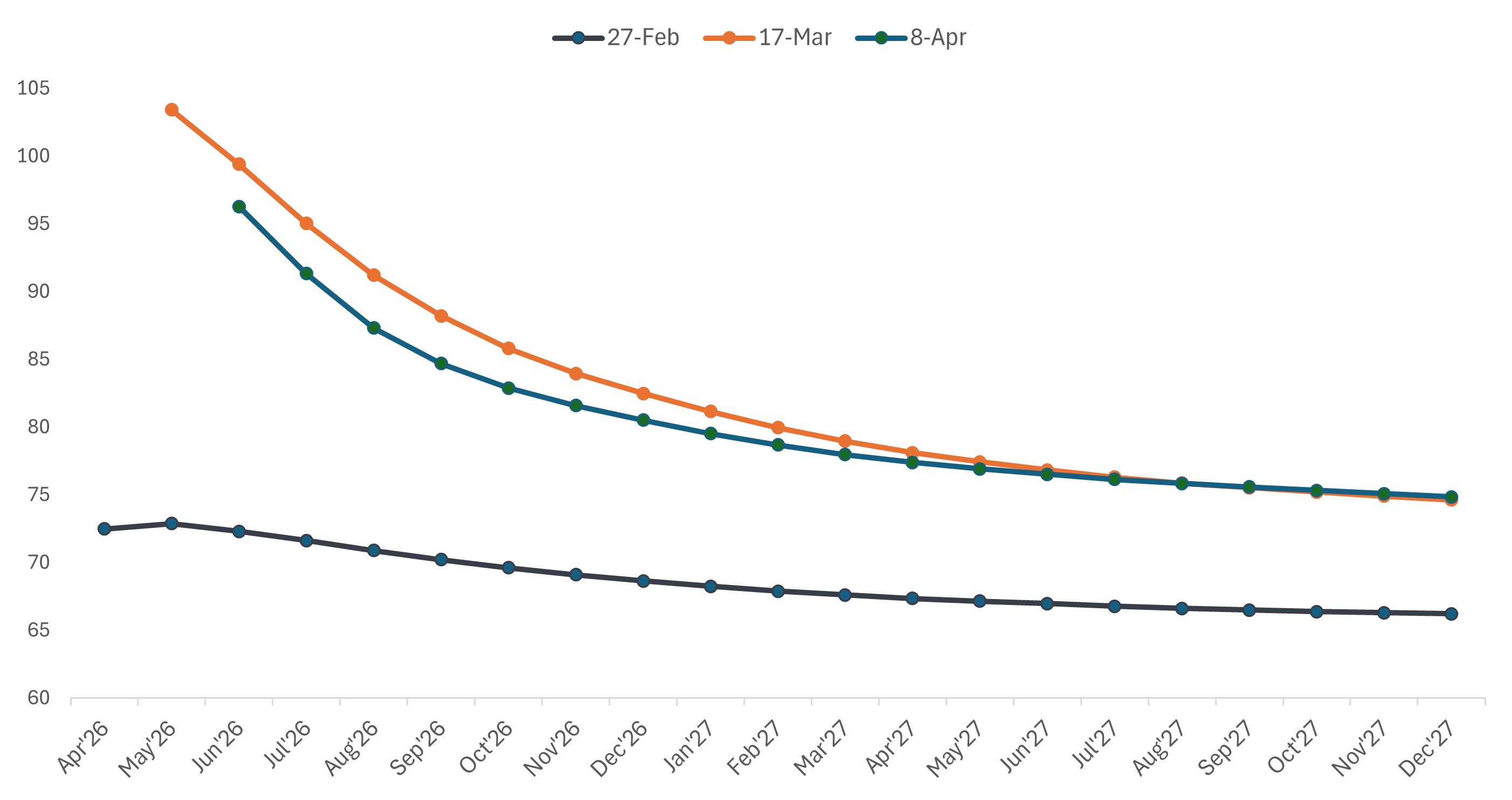

What the futures curve is telling us

The futures curve offers a useful window into how markets are thinking beyond the headlines. While near‑term contracts have been volatile, longer‑dated prices have moved up more modestly. The 2027 portion of the curve has shifted higher, but it still implies prices settling back toward the mid-$70s over time.

It’s worth noting that U.S. producers have not responded with an increase in activity. While the back end of the curve has risen, it remains too low – and too uncertain – to prompt a widespread shift toward investment. That said, the longer prices remain elevated, the more likely we are to start seeing some rig and frac fleet additions.

Brent crude futures curve

While the 2027 curve has shifted higher, prices are seen gradually easing back to the mid-$70s.

Source: Bloomberg, Brent crude futures curve. Data as of 8 April 2026.

Source: Bloomberg, Brent crude futures curve. Data as of 8 April 2026.

Further out, the magnitude of disruption from this episode could have more lasting effects on supply and demand dynamics. Supply shocks undermine confidence in the reliance on foreign energy, and countries will be looking to prioritize domestic energy security. We would expect those without domestic hydrocarbon resources to increasingly prioritize alternatives, including a combination of renewables-plus-battery storage and nuclear – all of which could eventually weigh on demand and put downward pressure on prices.

What the current environment means for the energy sector

The energy sector has done a great job reducing leverage, but some companies are still running at above-target debt levels. Every day oil is priced above pre-conflict planning assumptions, that incremental cash can be used to strengthen balance sheets, transferring value to equity. For firms already at target leverage, that excess cash may flow toward increased share repurchases or, to a lesser extent, special dividends.

Despite the recent rise in share prices across the sector, companies selectively buying back stock at attractive cash‑flow yields can be a sensible use of excess capital, particularly given the uncertain path of oil and gas prices. It could also turn out to be meaningfully accretive to earnings if commodity prices stay elevated.

Energy stocks have had a strong run, and after a stretch of meaningful outperformance through March (when other sectors were broadly lower), it’s reasonable to think that a reopening of the Strait could contribute to a temporary period of adjustment. However, while headline-driven noise may hold sway in the short term, we continue to see selective opportunities across the sector for investors taking a longer-term view.

BRENT – A blended crude stream oil sourced from the North Sea, known for its consistent quality and global trading price, which serves as a reference or “marker” for pricing a number of other crude streams.

Crude futures curve (or forward curve) is a graph mapping the prices of crude oil futures contracts for different delivery dates, plotted against their respective maturity dates.

Volatility measures risk using the dispersion of returns for a given investment.

West Texas Intermediate (WTI) is a high-quality North American crude oil and one of the three main global benchmarks of oil pricing. It is the second-most-traded oil benchmark, behind Brent crude, and is traded on the New York Mercantile Exchange.

IMPORTANT INFORMATION

Commodities (such as oil, metals and agricultural products) and commodity-linked securities are subject to greater volatility and risk and may not be appropriate for all investors. Commodities are speculative and may be affected by factors including market movements, economic and political developments, supply and demand disruptions, weather, disease and embargoes.

Diversification neither assures a profit nor eliminates the risk of experiencing investment losses.

Energy industries can be significantly affected by fluctuations in energy prices and supply and demand of fuels, conservation, the success of exploration projects, and tax and other government regulations.

Equity securities are subject to risks including market risk. Returns will fluctuate in response to issuer, political and economic developments.

These are the views of the author at the time of publication and may differ from the views of other individuals/teams at Janus Henderson Investors. References made to individual securities do not constitute a recommendation to buy, sell or hold any security, investment strategy or market sector, and should not be assumed to be profitable. Janus Henderson Investors, its affiliated advisor, or its employees, may have a position in the securities mentioned.

Past performance does not predict future returns. The value of an investment and the income from it can fall as well as rise and you may not get back the amount originally invested.

The information in this article does not qualify as an investment recommendation.

There is no guarantee that past trends will continue, or forecasts will be realised.

Marketing Communication.