Key takeaways:

- Despite heightened geopolitical risk, corporate credit spreads have moved largely in line with rates rather than experiencing a material deterioration. This reflects an environment where shocks are being treated as volatility events, with no clear significant transmission yet into corporate fundamentals or economic stress.

- With spreads remaining contained and credit behaving in an orderly manner, markets suggest limited near‑term downside from geopolitical risks alone. For investors, this reduces the urgency to de‑risk, instead favouring a measured approach that recognises stability driven by both market dynamics and behaviour as well as fundamentals.

- This suggests an opportunity to exploit rising dispersion through active security selection in credit. Given the ongoing uncertainty, this environment therefore favours adding risk selectively in attractive issuers, rather than indiscriminately increasing risk, as idiosyncratic outcomes increasingly drive returns.

Credit markets sanguine amid geopolitical risk

The conflict in the Middle East has drawn parallels with the outbreak of the Russia-Ukraine War, with concerns that an oil-induced supply and inflation shock could harm the global economy. So far, credit markets have reacted in a sanguine manner, with changes in credit spreads not dissimilar to the rates impact from rising government bond yields.

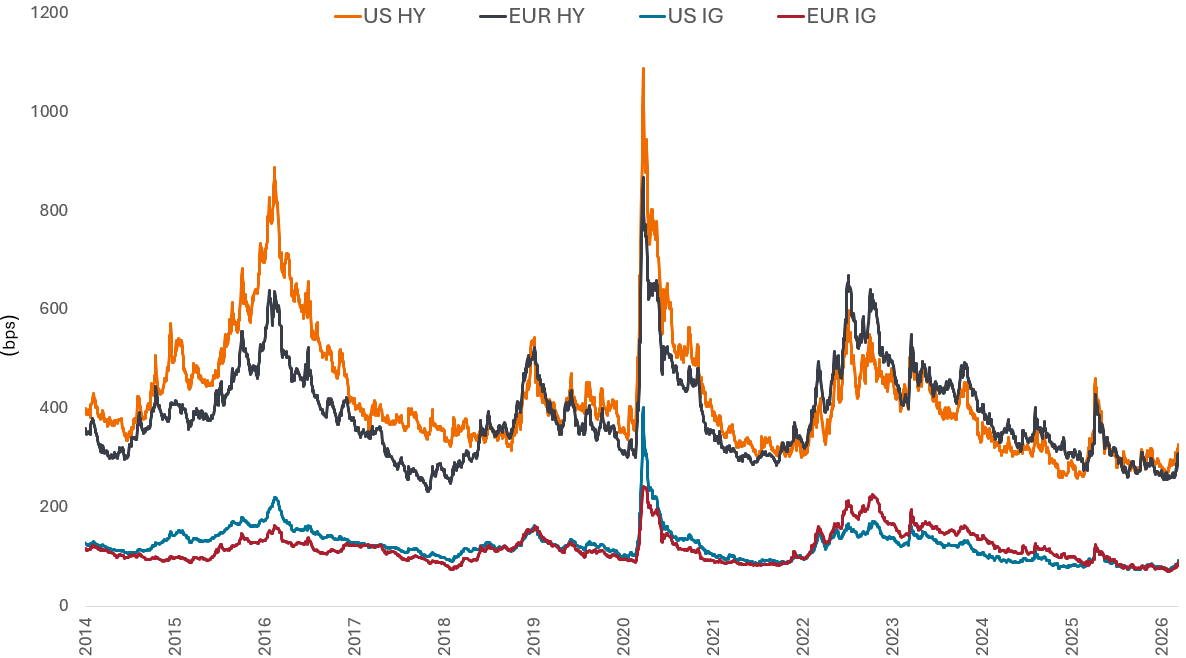

As the chart below shows, the recent tick-up in credit spreads is muted when compared to last year’s Liberation Day sell-off, let alone the 2015 energy sell-off after oil prices collapsed or the Covid spike.

For now, the market assumption is that the conflict remains regional, although high oil and gas prices – caused by Iran’s choke hold on ships transiting the Strait of Hormuz – could have a material impact on inflation and consumption were they to be sustained beyond the short term. For the time being, geopolitical shocks have not yet translated into a material deterioration in key economic data. So far, we see this as a volatility event rather than an economic event impacting inflation and consumption.

Figure 1: Credit spread on high yield and investment grade corporate bonds

Source: Bloomberg, US HY = US High Yield:ICE BofA US High Yield Index; EUR HY = Euro High Yield: ICE BofA Euro High Yield Index, US IG = US investment grade: ICE BofA US Corporate Index, EUR IG = Euro Investment Grade: ICE BofA Euro Corporate Index, Govt OAS (option adjusted spreads over governments), 01 January 2014 to 13 March 2026. Bps= basis points. Spreads may vary and are not guaranteed. Past performance does not predict future returns.

The forces behind corporate credit’s resilience

We believe there are several reasons why the corporate bond markets have responded in such an orderly way.

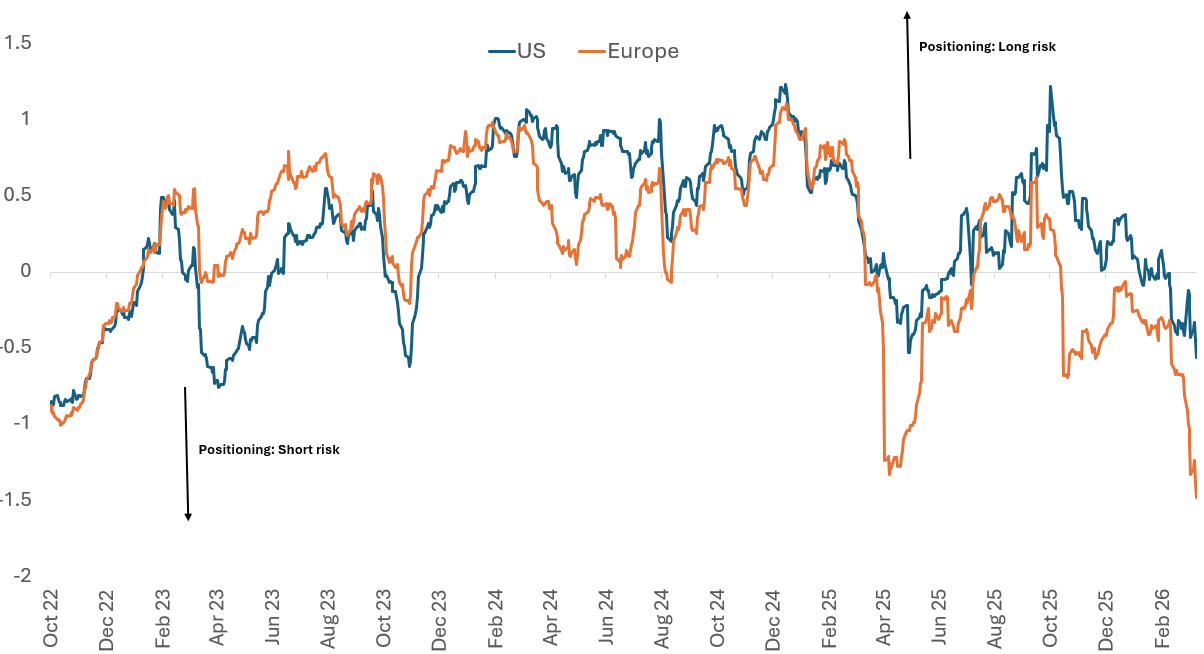

First, investor positioning is light given credit spreads are at the tighter end of historical ranges (Figure 2). Anecdotally, most investors were neutrally positioned heading into this conflict and waiting for more attractive valuations to add risk. Recall that there had been nervousness around artificial intelligence (AI) disruption and private credit fears earlier in the year.

Figure 2: Positioning in credit is light, as market trades short

Source: ICI, Bloomberg, DTCC, BNP Paribas. The BNPP Positioning Indicator (BNPPIUS, BNPPIEU) reflects data on dealer inventories, funds’ cash balances, Commodity Trading Advisors (CTA) positioning, Credit Default Swap (CDS) market positioning and option hedging, as at 12 March 2026. The BNPP Credit Positioning Indicator shows how long (positive number) or short (negative number) investors are positioned in credit markets, indicating whether exposure to credit risk is extended, neutral or defensive.

Second, there has already been a reasonable amount of corporate bond issuance so far this year. US investment grade issuance was US$474 billion in the first 10 weeks of the year, up 6% compared to the same period in 2025, and US high yield and loans (leveraged finance) issuance was US$64 billion, up 34% compared with the same period in 2025. Over the same period European investment grade issuance is €170 billion, down a marginal 3%, but European high yield is €23 billion, up 40% year- on-year.1

A key concern has been the scale of tech-related issuance, particularly for the investment grade market. However, the hyperscalers have made good progress with their capital raising, with Oracle claiming they do not expect to issue any additional bonds for the remainder of the calendar year 2026.2 Taken together, companies have been successful in borrowing earlier in the year which should take some pressure off needing to come to the market in the very near term. The strong technical (market dynamics) picture that has been in place should remain intact.

Third, turning to demand, higher yields are already attracting yield sensitive buyers, such as insurance companies stepping in as we have heard anecdotally. Yields on US high yield are back above 7% and are at 5.7% in European high yield. US investment grade is above 5% and European investment grade at 3.5%.3 As explained earlier, a portion of the yield change has been due to the rise in government yields reflecting higher inflation expectations. This has led to a moment of positive correlation between rates and credit spreads, which tends to be temporary.

Credit fundamentals resilient

Another backstop to credit spreads is that corporate fundamentals generally remain supportive. Earnings expectations have not rolled over and continue to underpin credit quality. Near‑term earnings face a relatively low hurdle, as Q1 results last year were depressed by tariff speculation, limiting downside risk as we move through the upcoming earnings season. Consensus expectations point to a healthy 20% earnings-per-share growth by Q4 versus Q1, consistent with the typical second‑half earnings catch‑up seen in prior years. Even if those forecasts ultimately prove optimistic, interest rate coverage – earnings covering interest expenses – are broadly stable across investment grade and leveraged finance (high yield and loans).

With macro growth still resilient – particularly in the US – credit quality is expected to remain robust enough to absorb market volatility. This provides a supportive macro backdrop for sufficient cashflows to service generally stable and manageable leverage levels. With all‑in yields at attractive levels, fundamentals and earnings serve as the anchor to allow investors to lean into wider spreads where attractive risk-adjusted potential can be captured. This is rather than idiosyncratic risk or geopolitical volatility spooking investors as signalling the start of a more adverse credit cycle.

Idiosyncratic stress is rising – but is not systemic

To take a step back then, there is no evidence of a broad earnings downgrade cycle emerging across investment grade or high yield credit. Recent market volatility is increasingly being driven by idiosyncratic rather than broad‑based credit risk, with stress emerging unevenly across sectors and issuers.

One area this surfaced in is software, where dispersion widened sharply and price action was severe in specific names as AI-related concerns dominated around revenue displacement. While software is a small component of high-yield indices, the volatility emerged more in the loans market, which has become increasingly bifurcated and private credit. For loans, selective mispriced opportunities have emerged, while CLOs, the main buyer of loans, continue to launch, with many warehouses looking for loans, supporting demand in the near term. This is important as leveraged finance does well in environments where readily available refinancing is present.

Private credit, on the other hand, is facing rising redemption pressure. We are seeing headlines around the gating of funds and increased scrutiny of asset values, alongside banks reassessing collateral valuations and pulling back from certain lending relationships. Nevertheless, this adjustment appears to be gradual and uneven, unfolding over time rather than triggering an immediate spillover into public markets.

In this context, stress in private markets need not be destabilising for public credit. As capital becomes more cautious it tends to be redeployed conservatively, such as into short-dated bonds or liquid investment grade credit. This may present a modest but constructive technical (demand) for public markets, particularly at a time when yields have become more attractive and markets are sensitive to reward the winners.

Rising dispersion from a K-shaped economy

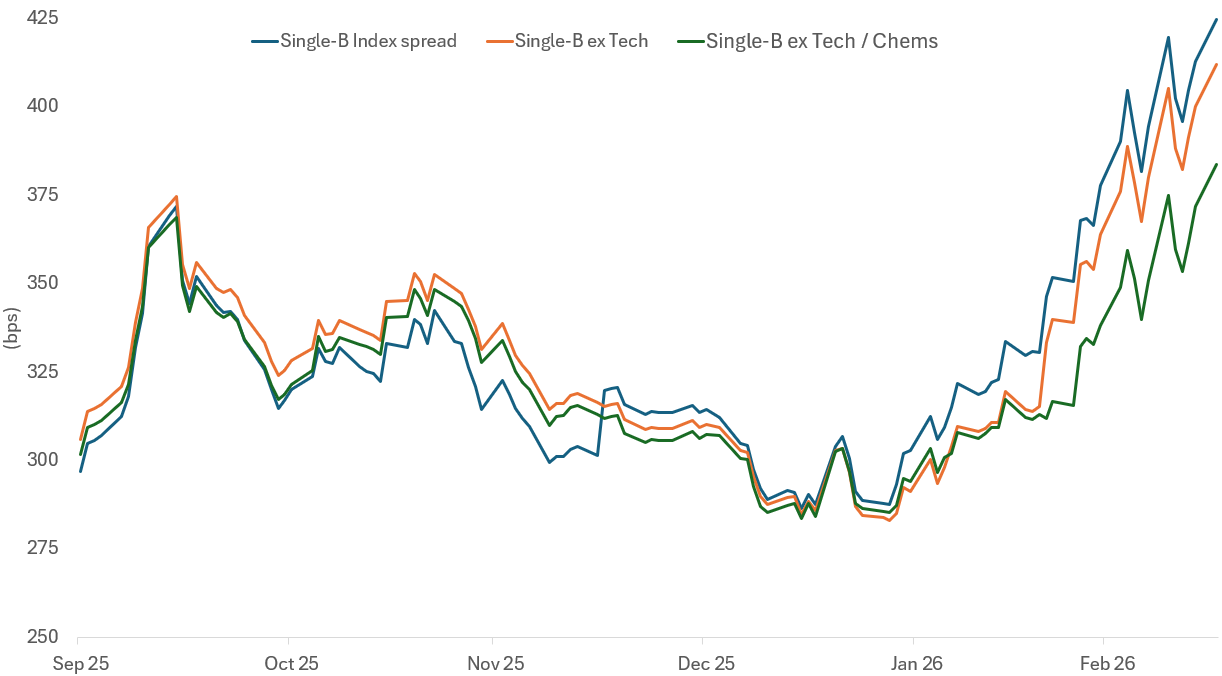

The credit market is increasingly characterised as resembling a K-shaped economy, with deepening dispersion between higher-quality issuers and weaker credits. Stronger issuers continue to trade with resilience, while weaker credits are being repriced more sharply. This is notably apparently in Europe for example in single‑B rated names, where spreads have moved much wider with weakness seen in technology and chemicals, even as index‑level moves remain modest (Figure 3). The widening gap between B-rated bonds and BB-rated bonds underscores how risk is being priced idiosyncratically, not indiscriminately across credit markets.

Figure 3: Single Bs are tighter excluding technology and chemicals

Source: Barclays, as 16 March 2026. Spreads may vary and are not guaranteed. Past performance does not predict future returns.

For credit investors, this creates an opportunity that is incremental rather than wholesale. Valuations have moved off their tightest levels, but remain far from historic stress points, suggesting scope to add risk selectively. With spreads still tight in aggregate and macro uncertainty elevated, timing and discrimination matter. After all, historical analysis suggests that oil price shocks typically take months to mean-revert once conflicts stabilise.

The opportunity therefore lies not in chasing beta, but in leaning into dispersion and adding risk where repricing has been meaningful and fundamentals remain intact, while remaining cautious where valuations have yet to adjust. In that sense, the current environment rewards patience and selectivity, allowing credit investors to engage constructively and with confidence that the forces underpinning resilience remain firmly in place, and in some cases appear to have strengthened.

IMPORTANT INFORMATION:

Fixed income securities are subject to interest rate, inflation, credit and default risk. The bond market is volatile. As interest rates rise, bond prices usually fall, and vice versa. The return of principal is not guaranteed, and prices may decline if an issuer fails to make timely payments or its credit strength weakens.

High-yield or “junk” bonds involve a greater risk of default and price volatility and can experience sudden and sharp price swings.

Private Credit refers to direct lending or debt financing outside of traditional banking, typically involving non-publicly traded companies, and comes with increased risk including limited liquidity, reliance on the borrower’s financial health, and less regulatory oversight compared to traditional bank lending.

Volatility measures risk using the dispersion of returns for a given investment

References made to individual securities do not constitute a recommendation to buy, sell or hold any security, investment strategy or market sector, and should not be assumed to be profitable.

1Source: Morgan Stanley, 9 March 2026.

2Source: Oracle, Fiscal Year 2026 Third Quarter Financial Results, 10 March 2026.

3Source: Bloomberg, ICE BofA indices, as at 13 March 2026.

4 Source: Source: FactSet, Bloomberg, S&P Capital IQ, company data, Morgan Stanley Research, 9 March 2026. Both gross leverage and interest coverage is median levels across US IG, US HY, US loans, EU IG, EU HY.

Balance sheet: A financial statement that summarises a company’s assets, liabilities, and shareholders’ equity at a particular point in time. Each segment gives investors an idea as to what the company owns and owes, as well as the amount invested by shareholders. It is called a balance sheet because of the accounting equation: assets = liabilities + shareholders’ equity.

Balance sheet strength: A company’s financial position.

Beta: This is the measure of the relationship that a portfolio or security has with the overall market. The beta of a market is always 1. A portfolio with a beta of 1 means that if the market rises 10%, so should the portfolio. A portfolio with a beta of more than 1 means it will likely move more than the market average (i.e., more volatility). A beta of less than 1 means that a security is theoretically less volatile than the market.

Cash flow: The net balance of cash that moves in and out of a company. Positive cash flow shows more money is moving in than out, while negative cash flow means more money is moving out than into the company.

Corporate fundamentals refer to the underlying financial and operating health of a company, used by investors—especially credit investors—to assess its ability to generate cash, service debt and withstand economic stress.

Collateralised Loan Obligation (CLO): A bundle of generally lower-quality leveraged loans to companies that are grouped together into a single security which generates income (debt payments) from underlying loans. The regulated nature of bonds that CLOs hold means that in the event of default, the investor is near the front of the queue to claim on a borrower’s assets.

Credit: Credit is typically defined as an agreement between a lender and a borrower. It is often narrowly used to describe corporate borrowings, which can take the form of corporate bonds, loans, or other fixed-interest asset classes.

Credit default swap (CDS): A form of derivative contract between two parties used to manage the credit risk of a bond. The buyer makes regular payments to the seller, while the seller agrees to pay off the underlying debt if there is a default on the bond. A CDS is considered insurance against non-payment and is also a tradable security. This allows a fund manager to take positions on a particular issuer or index without owning the underlying security or securities.

Credit rating: An independent assessment of the creditworthiness of a borrower by a recognised agency such as Standard & Poors, Moody’s, or Fitch. Standardised scores such as ‘AAA’ (a high credit rating) or ‘B’ (a low credit rating) are used, although other agencies may present their ratings in different formats.

Credit risk: The risk that a borrower will default on its contractual obligations to make the required interest payments or repay the loan. Anything that improves conditions for a company can help to lower credit risk.

CLO warehouse is a temporary, short-term financing arrangement where a bank provides capital to a Collateralised Loan Obligation (CLO) manager to accumulate a portfolio of loans before the CLO formally launches.

Credit spread: The difference in yield between securities with similar maturity but different credit quality, often used to describe the difference in yield between corporate bonds and government bonds. Widening spreads generally indicate a deteriorating creditworthiness of corporate borrowers, while narrowing indicates improving.

Dispersion: The extent to which a distribution of data points is stretched or squeezed. If the data points cluster around certain values, then dispersion is low, whereas if they are more spread out, then dispersion is high. For example, dispersion in stocks measures the range of returns for a group of stocks. Higher dispersion opens up opportunities for stock pickers to outperform by selecting the winners and avoiding the losers, given that stock returns are spread more widely on either side of the benchmark.

Earnings per share (EPS): EPS is the bottom-line measure of a company’s profitability, defined as net income (profit after tax) divided by the number of outstanding shares.

High-yield bond: A bond with a lower credit rating than an investment-grade bond, also known as a sub-investment grade bond, or ‘junk’ bond. These bonds usually carry a higher risk of the issuer defaulting on their payments, so they are typically issued with a higher-interest rate (coupon ) to compensate for the additional risk.

Hyperscalers: Companies that provide infrastructure for cloud, networking, and internet services at scale. Examples include Google Cloud, Microsoft Azure, Facebook Infrastructure, Alibaba Cloud, and Amazon Web Services.

A K‑shaped economy describes a recovery or growth phase in which different parts of the economy diverge sharply, rather than improving or weakening together.

Idiosyncratic risk: Factors that are specific to a particular company and have little or no correlation with market risk.

Inflation: The rate at which the prices of goods and services are rising in an economy. The consumer price index (CPI) and retail price index (RPI) are two common measures; the opposite of deflation.

Leverage: Leverage is also an interchangeable term for gearing : the ratio of a company’s loan capital (debt) to the value of its ordinary shares (equity). It can also be expressed in other ways, such as net debt as a multiple of earnings, typically net debt/EBITDA. Higher leverage equates to higher debt levels.

Leveraged loan: Privately-issued debt from non-investment grade (lower quality) companies that is secured against company assets, and that ranks first in priority of payment in the event of default. These types of loans generally offer a higher interest rate to offset the perception of higher risk.

Private credit: An asset defined by non-bank lending where the debt is not issued or traded on the public markets.

Re-rating: Occurs when investors are willing to pay a higher price for shares, usually in anticipation of higher future earnings. In terms of bonds, a re-rating can be assigned when the bond issuer’s ability to service and repay its debt improves (credit quality). Also see de-rating.

Relative valuation: Comparing the price of an asset to the market value of similar assets.

Risk-adjusted return: A calculation of an investment’s return or potential return that takes into account the amount of risk required to achieve it. Typical risk measures include alpha, beta, volatility, Sharpe ratio, and R2.

Systemic risk: The risk of a critical or harmful change in the financial system as a whole which would affect all markets and asset classes.

Volatility: The rate and extent at which the price of a portfolio, security, or index, moves up and down. If the price swings up and down with large movements, it has high volatility. If the price moves more slowly and to a lesser extent, it has lower volatility. The higher the volatility, the higher the risk of the investment.

Yield: The level of income on a security over a set period, typically expressed as a percentage rate. For a bond, this is calculated as the coupon payment divided by the current bond price.

These are the views of the author at the time of publication and may differ from the views of other individuals/teams at Janus Henderson Investors. References made to individual securities do not constitute a recommendation to buy, sell or hold any security, investment strategy or market sector, and should not be assumed to be profitable. Janus Henderson Investors, its affiliated advisor, or its employees, may have a position in the securities mentioned.

Past performance does not predict future returns. The value of an investment and the income from it can fall as well as rise and you may not get back the amount originally invested.

The information in this article does not qualify as an investment recommendation.

There is no guarantee that past trends will continue, or forecasts will be realised.

Marketing Communication.