Key takeaways:

- Healthcare rebounded strongly in the second half of 2025, led by innovation‑driven segments, while managed care was left behind amid persistent cost pressures and policy headwinds.

- We believe depressed valuations and improved visibility have shaped a more favorable setup for managed care through the remainder of 2026, reinforced by the April 6 final Medicare Advantage rate decision, even as longer‑term structural challenges remain.

- With innovation continuing to drive the sector, any incremental contribution from managed care would represent an additional tailwind to a constructive healthcare backdrop, though a selective approach remains key, in our view.

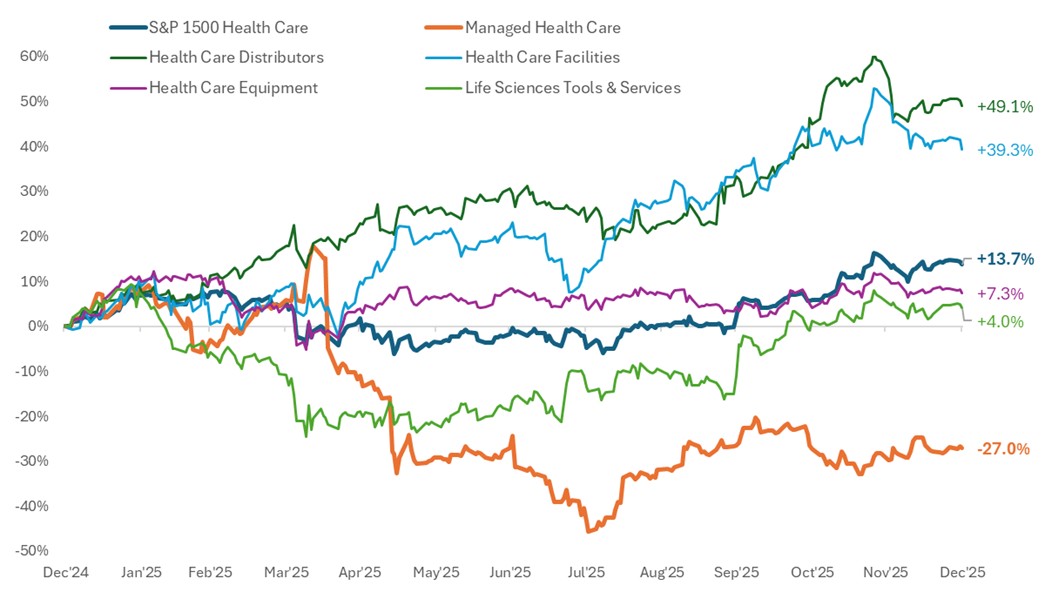

Healthcare stocks staged a strong rebound in the second half of last year, resulting in their best annual performance in four years. The recovery, however, was uneven across the sector.

Innovation-led areas drove the returns. Pharmaceuticals and biotechnology benefited from easing policy headwinds, lower interest rates, and resurgent merger and acquisition (M&A) activity, supporting a more constructive backdrop for healthcare overall. Other groups, including medical technology, life science tools, healthcare facilities, and distributors, also contributed meaningfully to the sector’s performance.

Managed care, on the other hand, stood out as the notable exception. Instead of participating in the broader recovery, managed care stocks languished amid margin pressures, rising medical costs, and continued uncertainty around federal reimbursement.

After an extraordinary period of underperformance for the traditionally defensive subsector, the key question now is whether expectations have fallen too far – particularly for 2026 – even as the industry may face a more challenging environment longer term.

S&P 1500 Health Care subsectors, total returns

Healthcare delivered strong 2025 returns despite the drag from managed care stocks.

Source: Bloomberg, data from 31 December 2024 to 31 December 2025. S&P 1500 Healthcare = S&P Composite 1500® Health Care, which comprises those companies included in the S&P Composite 1500 that are classified as members of the GICS® Health Care sector. Subsectors listed comprise those companies included in the S&P Composite 1500 classified as members of the respective GICS® Health Care sub-industry. Past performance is no guarantee of future results.

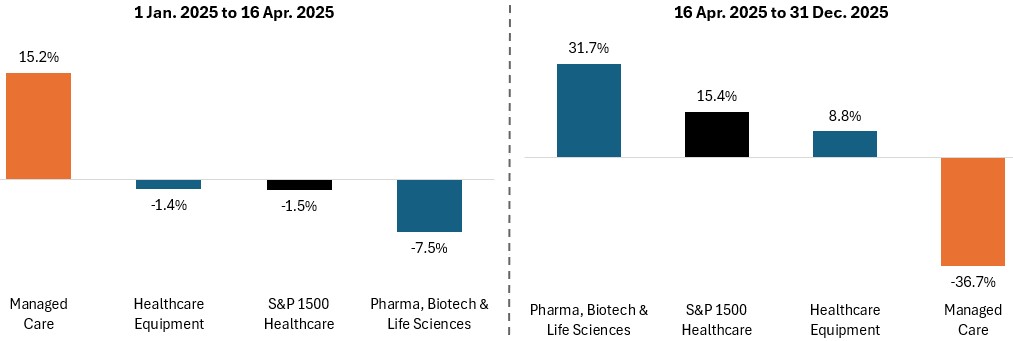

Why managed care fell out of favor: A series of resets

Looking back at early 2025, managed care stocks initially benefited from defensive investor positioning amid tariff concerns and heightened policy uncertainty, alongside tentative expectations that industry pressures might begin to stabilize.

That optimism faded in mid‑April when UnitedHealth Group lowered its earnings outlook. The guidance cut marked a turning point for sentiment, raising concerns that margin pressures across the industry could prove more persistent than previously anticipated.

Ultimately, managed care’s underperformance reflected a confluence of four forces: unprecedented regulatory change, higher‑than‑normal medical utilization and cost trends, irrational behavior that saw companies prioritize enrollment growth over profitability, and insurance premiums that failed to keep pace with rising costs.

S&P 1500 Healthcare sub-sector performance, total returns

(Pre- and post-April 2025 selloff)

Source: Bloomberg, data as of 31 December 2025. S&P 1500 Healthcare = S&P Composite 1500® Health Care, which comprises those companies included in the S&P Composite 1500 that are classified as members of the GICS Health Care sector. Sub-sectors listed comprise those companies included in the S&P Composite 1500 classified as members of the respective GICS Health Care sub-industry. Past performance is no guarantee of future results.

Then entering this year, sentiment took another hit in late January when the Centers for Medicare & Medicaid Services (CMS) released a disappointing preliminary reimbursement rate for privately run Medicare plans, adding to concerns around profitability. Managed care stocks sold off sharply, recording their largest one‑day decline since the Global Financial Crisis.

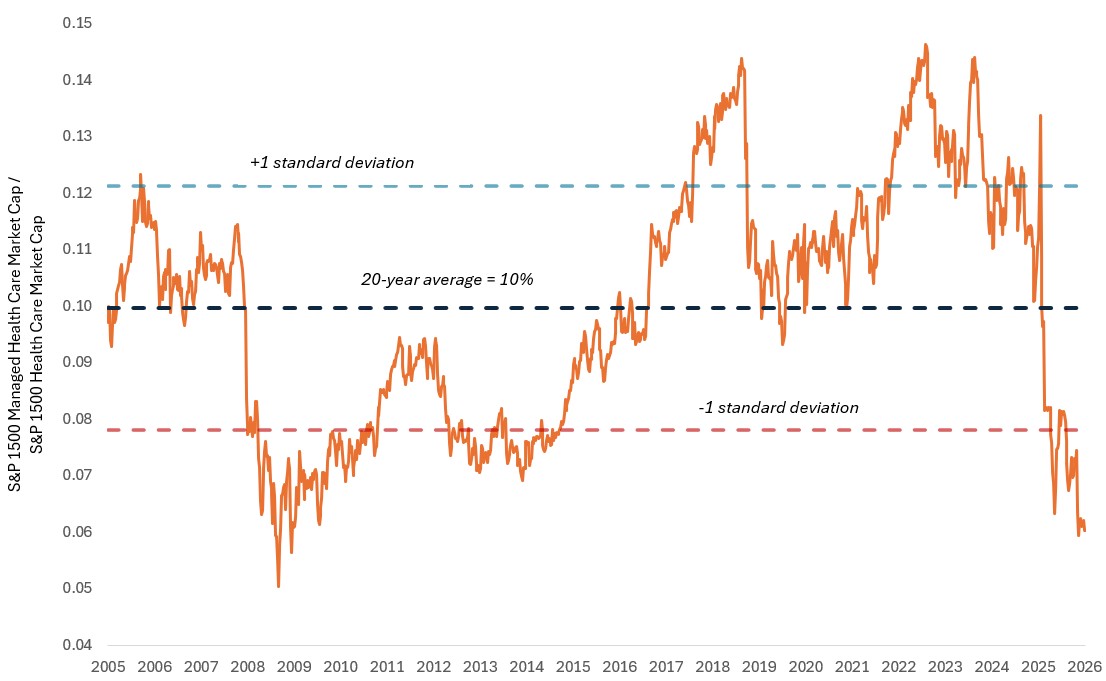

Valuations, expectations, and an improved 2026 setup

After a prolonged reset, managed care stocks trade at meaningfully lower valuation multiples in 2026 than they did in years past, with earnings estimates reflecting trough-level growth assumptions. Meanwhile, the subsector’s market capitalization as a share of the broader healthcare sector has fallen to its lowest level since 2009, at roughly 6% compared with a long-term average closer to 10% (and down from more than 14% just a few years ago), as shown in the chart below.

Managed care market cap as a percentage of S&P 1500 Healthcare

Managed care now represents the smallest share of the broader U.S. healthcare sector since 2009.

Source: Bloomberg, data as of 31 March 2026. S&P 1500 Healthcare = S&P Composite 1500® Health Care, which comprises those companies included in the S&P Composite 1500 that are classified as members of the GICS Health Care sector. S&P 1500 Managed Health Care comprises those companies within the S&P Composite 1500 classified as members of the GICS Managed Health Care sub-industry. Past performance is no guarantee of future results.

In our view, the setup for the remainder of 2026 appears more constructive than current sentiment suggests, for several reasons.

We believe earnings expectations are conservative, cost trends appear more stable, and plan behavior during enrollment has become more disciplined, with insurers reducing benefits to protect margins rather than chasing enrollment growth. Furthermore, many of the difficult decisions that had weighed on the subsector, such as cutting benefits or pulling back from unprofitable markets, have already been made.

Managed care could also gain appeal in a volatile macro environment. The group’s low multiples and U.S.‑centric exposure may resonate with investors seeking more defensive positioning. Health insurers historically tend to benefit from higher interest rates through investment income on their portfolios and are generally more insulated from inflation than many other healthcare segments given their ability to reprice premiums over time.

With expectations already depressed, even modest improvement in fundamentals or policy visibility could have an outsized influence on sentiment and valuations.

April CMS final rate decision: A near-term clearing event

Unlike 2025, when managed care stocks outperformed heading into April only to quickly reverse course, we believe the opposite scenario may be taking shape this year.

Following the January 2026 selloff tied to CMS’s preliminary rate proposal, investor focus shifted to the final rate decision scheduled for early April, the primary question being whether discussions with insurers during the notice period would yield any changes with less severe implications for industry economics.

On April 6, CMS released its final rate announcement, delivering a more favorable outcome than many expected. The agency finalized a 2.48% average increase in Medicare Advantage payments for 2027, or a 239 basis-point improvement from the near-flat rate proposed in January, translating to more than $13 billion in additional payments to plans next year.

Importantly, the improvement was driven largely by technical adjustments. In addition to the headline rate increase, CMS paused a risk‑adjustment change that would have been a headwind for many plans, while retaining other elements that effectively boost reimbursement. Taken together, these factors should bring effective payment growth much closer to medical cost trends, potentially reducing the need for aggressive benefit cuts and possibly making it easier for companies to protect or expand margins.

That said, the decision does not eliminate longer‑term policy risk. Looking ahead, CMS is likely to revisit risk‑adjustment changes in the January 2027 proposal (for 2028 rates). And with policymakers facing pressure to identify budget offsets, Medicare Advantage overpayments remain a potential target outside of an election year.

In that context, we are more inclined to view the April CMS decision as a near‑term clearing event that improves the 2026-2027 setup, rather than an “all clear” signal on the policy front.

Longer‑term industry backdrop remains challenging

Beyond 2026, the outlook for managed care stocks is more complex. Heightened regulatory scrutiny and an insufficient pricing environment – premiums not keeping pace with medical costs – could elongate the path back to normalized earnings and keep a lid on valuations.

Medicare Advantage growth could slow as benefit reductions make the program less attractive for those seeking coverage. Medicaid work requirements beginning in 2027 have the potential to pressure enrollment and risk mix, echoing adverse selection dynamics seen after the unwinding of pandemic-era protections. In addition, a series of changes that would negatively impact pharmacy benefit manager economics could pose another headwind for integrated managed care companies.

Together, these factors argue for structurally lower multiples and a selective investment approach, rather than a broad-based return to the higher valuations seen under prior regulatory regimes.

Managed care in the context of a more constructive healthcare backdrop

Managed care’s challenges have been real and more persistent than many anticipated, but we believe much of that reality is now reflected in prices. For 2026, a combination of more stable cost trends, improved reimbursement rates, and proactive benefit actions taken by companies may help ease some of the near-term headwinds, even as longer-term industry challenges remain.

Across the healthcare landscape, artificial intelligence (AI) is also emerging as a powerful force, with applications spanning drug development, medical devices, diagnostics, and operational efficiency. While much of the focus has centered on pharma, biotech, and medtech, managed care is another area where AI could have meaningful long‑term benefits that are not yet reflected in valuations.

Over time, we think health insurers could emerge as under-the-radar AI winners, given their low-margin, people-intensive business models and large data sets – all of which lend themselves to AI-driven efficiencies. In the near term, however, insurers may face reimbursement pressure from the growing use of AI-assisted medical coding tools by providers, which can influence reported patient severity and increase claim costs.

More broadly, the secular trends supporting the healthcare sector remain as strong as ever. Across pharma and biotech, advancements in drug development, increasingly targeted therapies, and new treatment paradigms continue to reshape standards of care, while medtech innovation is improving patient outcomes through less invasive procedures, better diagnostics, and the integration of digital tools into care delivery.

The sector’s strong performance in 2025 demonstrated that healthcare may not require managed care’s participation to drive returns. That said, if managed care begins to stabilize, we believe it would ultimately be supportive for the broader healthcare ecosystem. In our view, any incremental contribution from managed care would represent an additional tailwind to a constructive healthcare backdrop.

Basis point (bp) equals 1/100 of a percentage point. 1 bp = 0.01%, 100 bps = 1%.

S&P MidCap 400® Index reflects U.S. mid-cap equity performance and is an unmanaged group of 400 domestic stocks chosen for their market size, liquidity and industry group representation.

S&P 500® Index reflects U.S. large-cap equity performance and represents broad U.S. equity market performance.

S&P SmallCap 600® Index reflects U.S. small-cap equity performance and is an unmanaged group of 600 domestic stocks chosen for their market size, liquidity and industry group representation.

S&P Composite 1500® combines three indices, the S&P 500®, the S&P MidCap 400®, and the S&P SmallCap 600®, to cover approximately 90% of U.S. market capitalization.

Standard deviation measures the dispersion of data around the mean, representing the average distance between data points and their mean. In a normal distribution, approximately 68% of data points fall within one standard deviation above or below the mean.

IMPORTANT INFORMATION

Equity securities are subject to risks including market risk. Returns will fluctuate in response to issuer, political and economic developments.

Health care industries are subject to government regulation and reimbursement rates, as well as government approval of products and services, which could have a significant effect on price and availability, and can be significantly affected by rapid obsolescence and patent expirations.

These are the views of the author at the time of publication and may differ from the views of other individuals/teams at Janus Henderson Investors. References made to individual securities do not constitute a recommendation to buy, sell or hold any security, investment strategy or market sector, and should not be assumed to be profitable. Janus Henderson Investors, its affiliated advisor, or its employees, may have a position in the securities mentioned.

Past performance does not predict future returns. The value of an investment and the income from it can fall as well as rise and you may not get back the amount originally invested.

The information in this article does not qualify as an investment recommendation.

There is no guarantee that past trends will continue, or forecasts will be realised.

Marketing Communication.

Important information

Please read the following important information regarding funds related to this article.

- Shares/Units can lose value rapidly, and typically involve higher risks than bonds or money market instruments. The value of your investment may fall as a result.

- Shares of small and mid-size companies can be more volatile than shares of larger companies, and at times it may be difficult to value or to sell shares at desired times and prices, increasing the risk of losses.

- If a Fund has a high exposure to a particular country or geographical region it carries a higher level of risk than a Fund which is more broadly diversified.

- The Fund is focused towards particular industries or investment themes and may be heavily impacted by factors such as changes in government regulation, increased price competition, technological advancements and other adverse events.

- The Fund may use derivatives to help achieve its investment objective. This can result in leverage (higher levels of debt), which can magnify an investment outcome. Gains or losses to the Fund may therefore be greater than the cost of the derivative. Derivatives also introduce other risks, in particular, that a derivative counterparty may not meet its contractual obligations.

- If the Fund holds assets in currencies other than the base currency of the Fund, or you invest in a share/unit class of a different currency to the Fund (unless hedged, i.e. mitigated by taking an offsetting position in a related security), the value of your investment may be impacted by changes in exchange rates.

- When the Fund, or a share/unit class, seeks to mitigate exchange rate movements of a currency relative to the base currency (hedge), the hedging strategy itself may positively or negatively impact the value of the Fund due to differences in short-term interest rates between the currencies.

- Securities within the Fund could become hard to value or to sell at a desired time and price, especially in extreme market conditions when asset prices may be falling, increasing the risk of investment losses.

- The Fund could lose money if a counterparty with which the Fund trades becomes unwilling or unable to meet its obligations, or as a result of failure or delay in operational processes or the failure of a third party provider.

Specific risks

- Shares/Units can lose value rapidly, and typically involve higher risks than bonds or money market instruments. The value of your investment may fall as a result.

- Shares of small and mid-size companies can be more volatile than shares of larger companies, and at times it may be difficult to value or to sell shares at desired times and prices, increasing the risk of losses.

- If a Fund has a high exposure to a particular country or geographical region it carries a higher level of risk than a Fund which is more broadly diversified.

- The Fund is focused towards particular industries or investment themes and may be heavily impacted by factors such as changes in government regulation, increased price competition, technological advancements and other adverse events.

- The Fund may use derivatives to help achieve its investment objective. This can result in leverage (higher levels of debt), which can magnify an investment outcome. Gains or losses to the Fund may therefore be greater than the cost of the derivative. Derivatives also introduce other risks, in particular, that a derivative counterparty may not meet its contractual obligations.

- If the Fund holds assets in currencies other than the base currency of the Fund, or you invest in a share/unit class of a different currency to the Fund (unless hedged, i.e. mitigated by taking an offsetting position in a related security), the value of your investment may be impacted by changes in exchange rates.

- When the Fund, or a share/unit class, seeks to mitigate exchange rate movements of a currency relative to the base currency (hedge), the hedging strategy itself may positively or negatively impact the value of the Fund due to differences in short-term interest rates between the currencies.

- Securities within the Fund could become hard to value or to sell at a desired time and price, especially in extreme market conditions when asset prices may be falling, increasing the risk of investment losses.

- The Fund may incur a higher level of transaction costs as a result of investing in less actively traded or less developed markets compared to a fund that invests in more active/developed markets.

- The Fund could lose money if a counterparty with which the Fund trades becomes unwilling or unable to meet its obligations, or as a result of failure or delay in operational processes or the failure of a third party provider.