Key takeaways:

- Keeping interest rates in their current range was largely a non-event at this week’s Fed meeting; the true story was seeking insight into how the central bank could react to a range of scenarios should energy prices remain elevated.

- With its relatively solid economy and energy independence, the U.S. finds itself in the enviable position of being able to exercise patience with respect to the war and its impact on prices and growth.

- Given the wide range of possible geopolitical – and thus economic – outcomes, we believe fixed income investors should use caution when considering adjusting duration and credit risk until the market gains greater clarity on how this crisis unfolds.

While reflections on how the duration and magnitude of higher energy prices may impact the Fed’s next policy action were at the center of this week’s meeting, an underlying – and perhaps understated – theme was the nature of the U.S. central bank’s monetary philosophy and approach to its dual mandate.

Evidence of this can be found in the lack of consensus among voting members in a continuing departure from Chairman Jerome Powell’s historical modus operandi of seeking to build consensus. On one side – as expected – was recent appointee Stephen Miran, who’s been anything but shy about his preference to cut rates. While not necessarily joining him, the majority of the Federal Open Market Committee voters did indicate a dovish bias. This seems to have become the central bank’s default in the absence of an obvious inflationary impulse – and as evidenced by 2022’s transitory call, sometimes not even then.

Three other dissenters did not want to go along with a dovish bias. We can categorize them as either adhering to the Fed’s historical data-dependent approach to setting policy or perhaps willing to send a salvo to presumptive incoming Chair Kevin Warsh, who has presented a case for secularly lower interest rates. And since Chairman Powell was understandably willing to go there, we will too by proposing that Fed members could be signaling that they view their independence from political influence as sacrosanct and that policy decisions are the result of a deliberative committee.

Giving energy prices the attention they deserve

As the curtain possibly closes on the era of forward guidance, the Fed – as it had telegraphed – held its overnight benchmark rate steady, in a range of 3.50% to 3.75%. The continuation of pause deviated from the dovish script that had been laid out in late 2025. At that time, labor market softness intimated that the overnight rate could dip below 3.0% by the end of this year, as gauged by futures markets. In the wake of this week’s meeting, those same markets see no cuts for the remainder of the year.

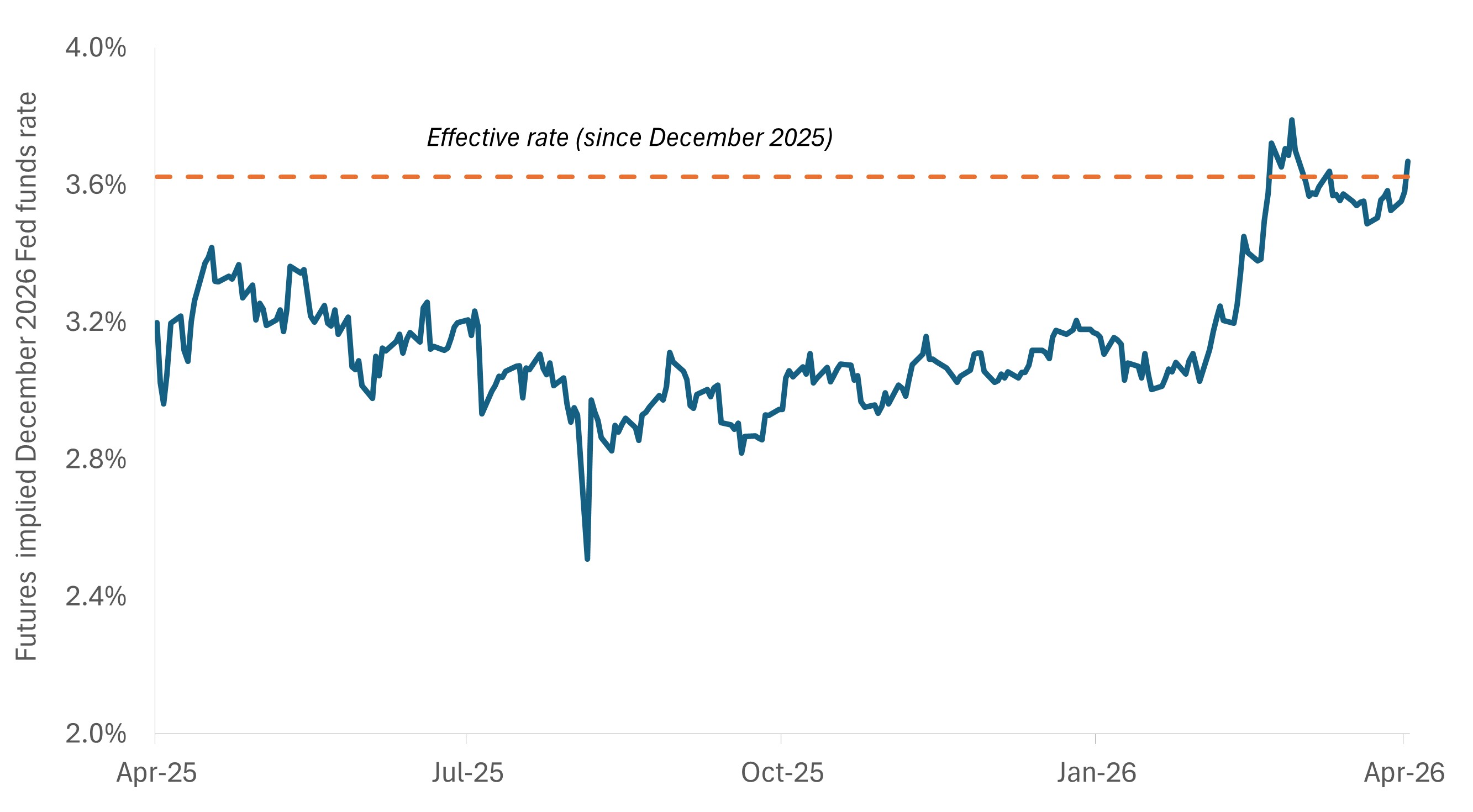

Exhibit 1: Market implied effective fed funds rate for December 2026

In the wake of the Iran War, futures markets have removed expectations for any rate cuts in 2026.

Source: Bloomberg, as of 29 April 2026.

Two developments drove this change: The labor market has largely stabilized, and energy prices have surged in the wake of hostilities between the U.S. and Iran and the subsequent closure of the Strait of Hormuz. The market’s – and indeed the Fed’s – initial response was to look through higher oil prices, focusing instead on broader economic conditions.

The duration of the conflict and seemingly no easy resolution have broken those sanguine assumptions. Acutely aware of its botched transitory call four years ago, the Fed cannot dismiss the risk posed by higher energy prices leaching into core prices or, worse, impacting inflation expectations.

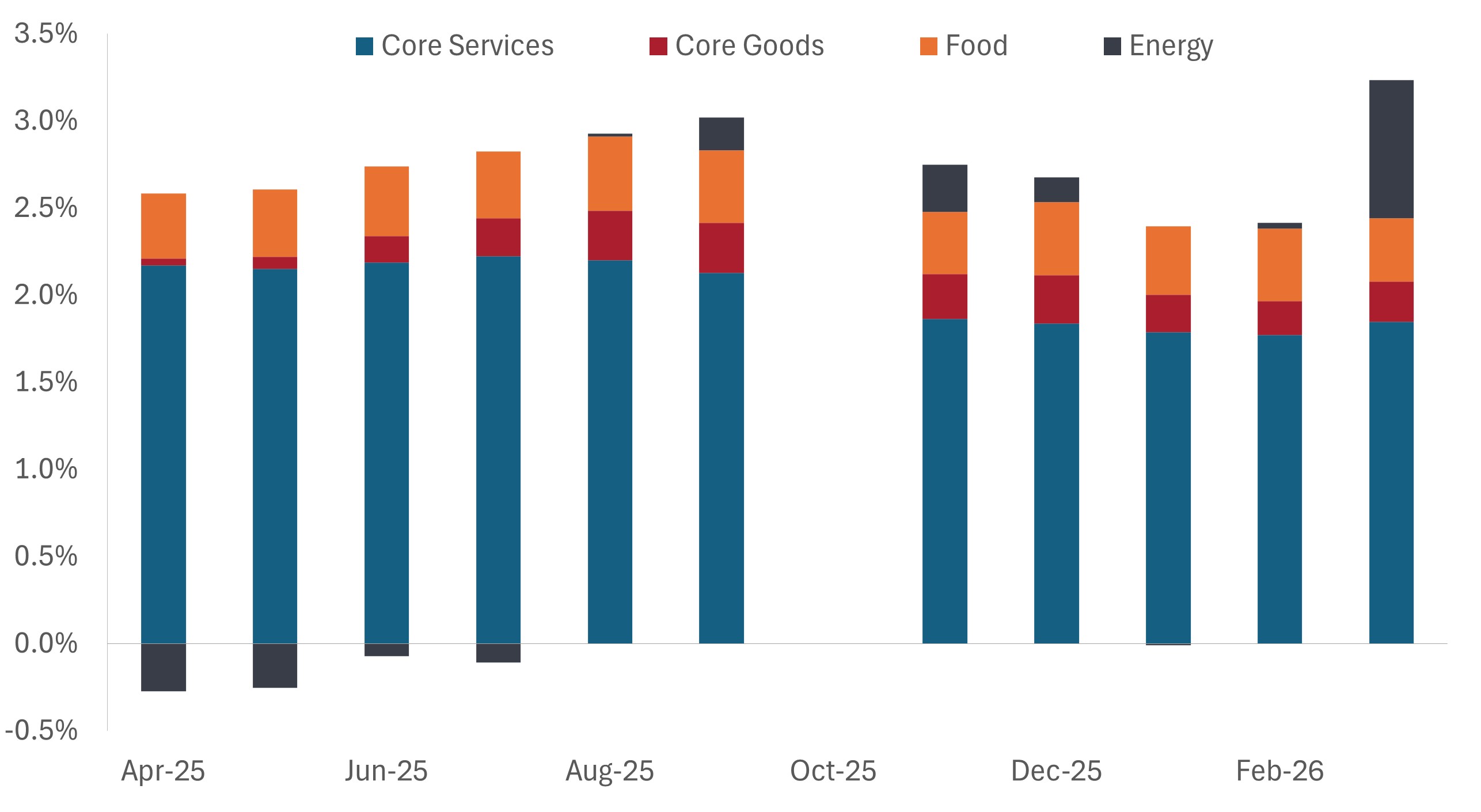

Exhibit 2: Components of U.S. Consumer Price Index (CPI)

Energy alone is behind March’s spike in headline CPI, and the Fed is likely closely monitoring how it may impact inflation expectations should it remain elevated and leach into other consumption categories.

Source: Bloomberg, as of 29 April 2026. October 2025 did not have a CPI report due to the government shutdown.

Fortunately for the Fed, solid economic expansion diminishes the tension that would have been otherwise felt in balancing the pillars of its dual mandate. Similarly, a stabilized labor market should lower the risk of a stagflationary environment that would force the Fed to make a difficult choice. We view current conditions as having bought time for the Fed as three possible scenarios play out:

- The conflict is resolved sooner than later, and energy prices revert to what had been a largely bearish environment of oversupply. This scenario would allow the Fed to look through a discrete inflationary surge.

- A prolonged period of energy prices seeps into broader inflation expectations, further pushing out what had been a bias to cut rates.

- Economic growth weakens as companies and households alter purchasing decisions in the wake of sustained higher prices. But even in this scenario, a rate cut is not guaranteed – likely owing to the Fed’s concern about allowing expectations to become unanchored.

Complicating matters for the Fed is that central banks are not in the business of managing supply-driven inflation. That said, the relative health of the U.S. economy and its energy independence should enable the Fed to be patient in seeing how these scenarios unfold, whereas other central banks may be forced to make tough decisions between containing prices and supporting growth. In fact, we believe the market has largely glossed over the risk to ex-U.S. growth posed by an extended military engagement and continued disruption of essential industrial and agricultural inputs.

But even in the U.S., tension between growth and inflation exists. And the longer this crisis plays out, the more that tension increases. Accordingly, we believe the bar has risen materially for any move: hike or cut.

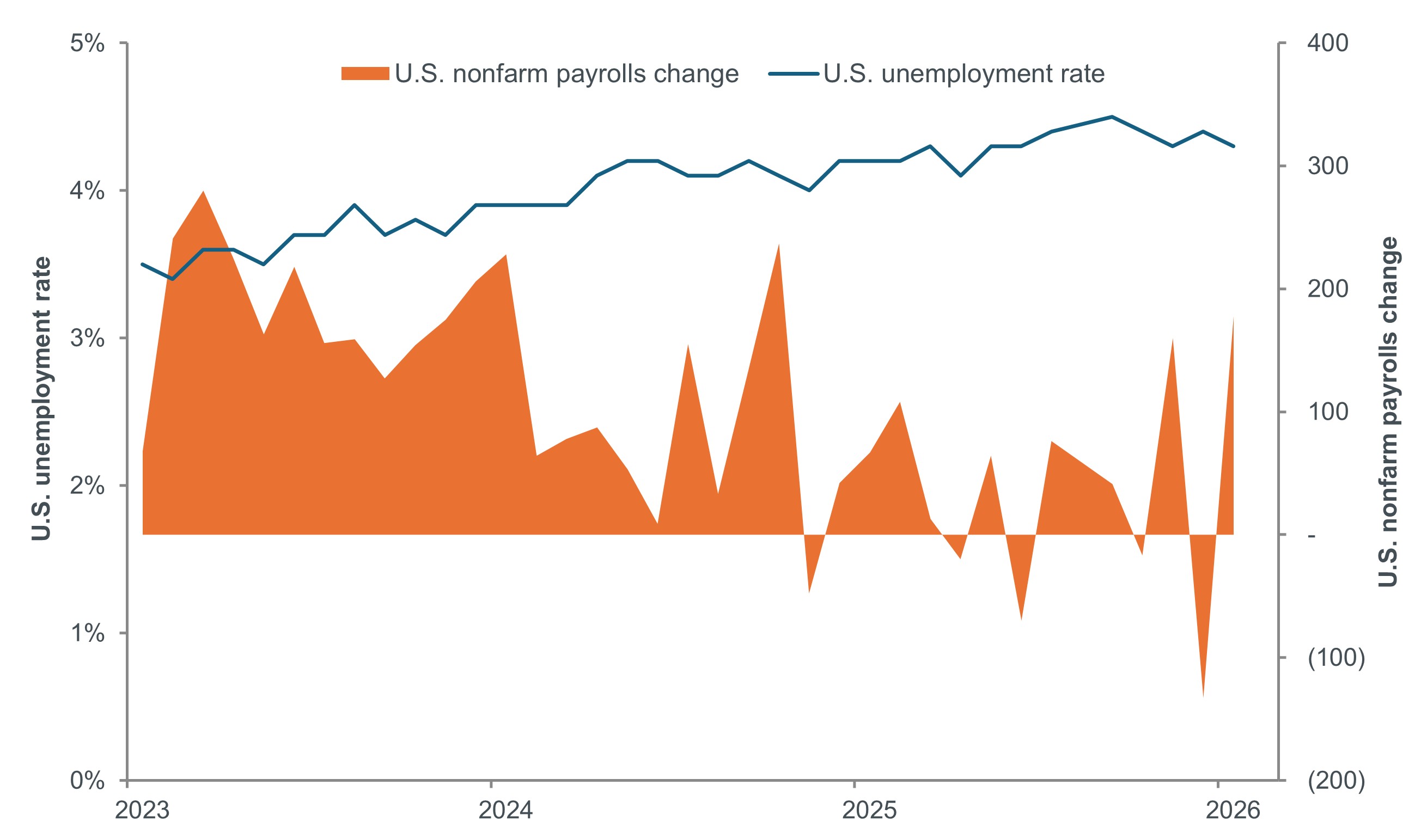

Exhibit 3: U.S. Labor market stabilizing

After a weak 2025, where monthly job gains were barely positive, two of 2026’s readings have signaled resilience, giving the Fed latitude to monitor the upside risk of inflation while placing less emphasis on a potentially stagnating economy.

Source: Bloomberg, as of 29 April 2026.

Standing pat as the range of outcomes remains wide

Positioning portfolios to account for a geopolitical event with a wide range of possible outcomes is a challenge. As illustrated by shifting deadlines, a series of ultimatums, and the intransigence of the opposing sides, we believe investors, especially within fixed income, should be cautious about increasing risk – either duration or credit – at present. Certain jurisdictions may have no choice but to react to higher energy prices with rate hikes, especially if their central bank’s mandate prioritizes price stability. But as stated, the longer this crisis extends, the greater risk it presents to growth, especially in regions heavily dependent upon energy and other commodities imports.

Looking forward

With respect to U.S. monetary policy, we believe it’s too early to call a regime change at the Fed. Even if voting members shy away from forward guidance under a Chairman Warsh, we expect that voting members representing a range of views will continue to prioritize data dependence.

Implicit in that, however, should be the absence of a secular dovish or hawkish bias. In our view, holding fast to a 2.0% inflation target – which hasn’t been achievable in five years – may represent a dovish worldview that is hard to square with a $6.7 trillion balance sheet that would take significant time to wind down and in a period of deglobalization.

Importantly, investors must recognize that even subtle policy shifts would have meaningful ramifications for regional and global growth, inflation expectations, the yield curve, and the pricing of risk-free and risky assets.

IMPORTANT INFORMATION

Energy industries can be significantly affected by fluctuations in energy prices and supply and demand of fuels, conservation, the success of exploration projects, and tax and other government regulations.

Fixed income securities are subject to interest rate, inflation, credit and default risk. The bond market is volatile. As interest rates rise, bond prices usually fall, and vice versa. The return of principal is not guaranteed, and prices may decline if an issuer fails to make timely payments or its credit strength weakens.

Consumer Price Index (CPI) is an unmanaged index representing the rate of inflation of the U.S. consumer prices as determined by the U.S. Department of Labor Statistics.

Duration measures the sensitivity of a bond’s or fixed income portfolio’s price to changes in interest rates. The longer a bond’s duration, the higher its sensitivity to changes in interest rates and vice versa.

Monetary Policy refers to the policies of a central bank, aimed at influencing the level of inflation and growth in an economy. It includes controlling interest rates and the supply of money.

Stagflation is an economic cycle characterized by slow growth and a high unemployment rate accompanied by inflation.

Volatility measures risk using the dispersion of returns for a given investment. The rate and extent at which the price of a portfolio, security or index moves up and down.

A yield curve plots the yields (interest rate) of bonds with equal credit quality but differing maturity dates. Typically bonds with longer maturities have higher yields.

These are the views of the author at the time of publication and may differ from the views of other individuals/teams at Janus Henderson Investors. References made to individual securities do not constitute a recommendation to buy, sell or hold any security, investment strategy or market sector, and should not be assumed to be profitable. Janus Henderson Investors, its affiliated advisor, or its employees, may have a position in the securities mentioned.

Past performance does not predict future returns. The value of an investment and the income from it can fall as well as rise and you may not get back the amount originally invested.

The information in this article does not qualify as an investment recommendation.

There is no guarantee that past trends will continue, or forecasts will be realised.

Marketing Communication.

Important information

Please read the following important information regarding funds related to this article.

- An issuer of a bond (or money market instrument) may become unable or unwilling to pay interest or repay capital to the Fund. If this happens or the market perceives this may happen, the value of the bond will fall.

- When interest rates rise (or fall), the prices of different securities will be affected differently. In particular, bond values generally fall when interest rates rise (or are expected to rise). This risk is typically greater the longer the maturity of a bond investment.

- The Fund invests in high yield (non-investment grade) bonds and while these generally offer higher rates of interest than investment grade bonds, they are more speculative and more sensitive to adverse changes in market conditions.

- Some bonds (callable bonds) allow their issuers the right to repay capital early or to extend the maturity. Issuers may exercise these rights when favourable to them and as a result the value of the Fund may be impacted.

- The Fund may use derivatives to help achieve its investment objective. This can result in leverage (higher levels of debt), which can magnify an investment outcome. Gains or losses to the Fund may therefore be greater than the cost of the derivative. Derivatives also introduce other risks, in particular, that a derivative counterparty may not meet its contractual obligations.

- If the Fund holds assets in currencies other than the base currency of the Fund, or you invest in a share/unit class of a different currency to the Fund (unless hedged, i.e. mitigated by taking an offsetting position in a related security), the value of your investment may be impacted by changes in exchange rates.

- When the Fund, or a share/unit class, seeks to mitigate exchange rate movements of a currency relative to the base currency (hedge), the hedging strategy itself may positively or negatively impact the value of the Fund due to differences in short-term interest rates between the currencies.

- Securities within the Fund could become hard to value or to sell at a desired time and price, especially in extreme market conditions when asset prices may be falling, increasing the risk of investment losses.

- The Fund could lose money if a counterparty with which the Fund trades becomes unwilling or unable to meet its obligations, or as a result of failure or delay in operational processes or the failure of a third party provider.

- In addition to income, this share class may distribute realised and unrealised capital gains and original capital invested. Fees, charges and expenses are also deducted from capital. Both factors may result in capital erosion and reduced potential for capital growth. Investors should also note that distributions of this nature may be treated (and taxable) as income depending on local tax legislation.

- The Fund invests in Asset-Backed Securities (ABS) and other forms of securitised investments, which may be subject to greater credit / default, liquidity, interest rate and prepayment and extension risks, compared to other investments such as government or corporate issued bonds and this may negatively impact the realised return on investment in the securities.