Key takeaways:

- Private credit and broadly syndicated loans are often mistaken as being similar, but differ fundamentally in borrower characteristics, spread and credit profile, market structure, valuation and liquidity. These distinctions shape how risk is priced, monitored and ultimately experienced by investors.

- Continuous market pricing in broadly syndicated loans provides clearer signals of credit deterioration, while periodic valuations in some private credit strategies can delay visibility. This affects how quickly investors can assess and respond to changing credit conditions.

- For CLO investors, understanding these differences is critical. CLOs are built on broadly syndicated loans and deliver liquidity through traded liabilities and transparent pricing, avoiding the redemption pressures and valuation step-changes that can arise in some private credit.

Private credit and broadly syndicated loans are not interchangeable

Recent developments in private credit have brought two issues into sharper focus: liquidity and valuation. Redemption pressure has risen in semi-liquid private credit vehicles such as Business Development Companies (BDCs), while several abrupt individual private credit write-downs have highlighted how slow-moving valuations can obscure underlying credit deterioration.

This is why it is important to distinguish private credit from broadly syndicated loans (or BSL) rather than treating the two as interchangeable forms of leveraged finance. Both markets finance below-investment-grade companies, and both often fund sponsor-owned businesses, but they differ materially in borrower profile, market structure, valuation framework, funding and liquidity mechanisms (Figure 1).

That distinction is particularly important in the context of Collateralised Loan Obligations (CLOs). CLOs are built on broadly syndicated loans and funded through term liabilities, where a CLO issues tranches of debt and equity with defined maturities. This means the investor experience is fundamentally different from that of some private credit vehicles that offer periodic liquidity against inherently less liquid underlying assets.

Nevertheless, it is worth noting that private credit is not a homogeneous asset class. Asset-backed financing, for instance, is supported by a pool of assets, generally with more predictable cash flows and security. This segment is not part of current market concerns around private credit and is therefore outside the scope of this article.

Private credit versus broadly syndicated loans

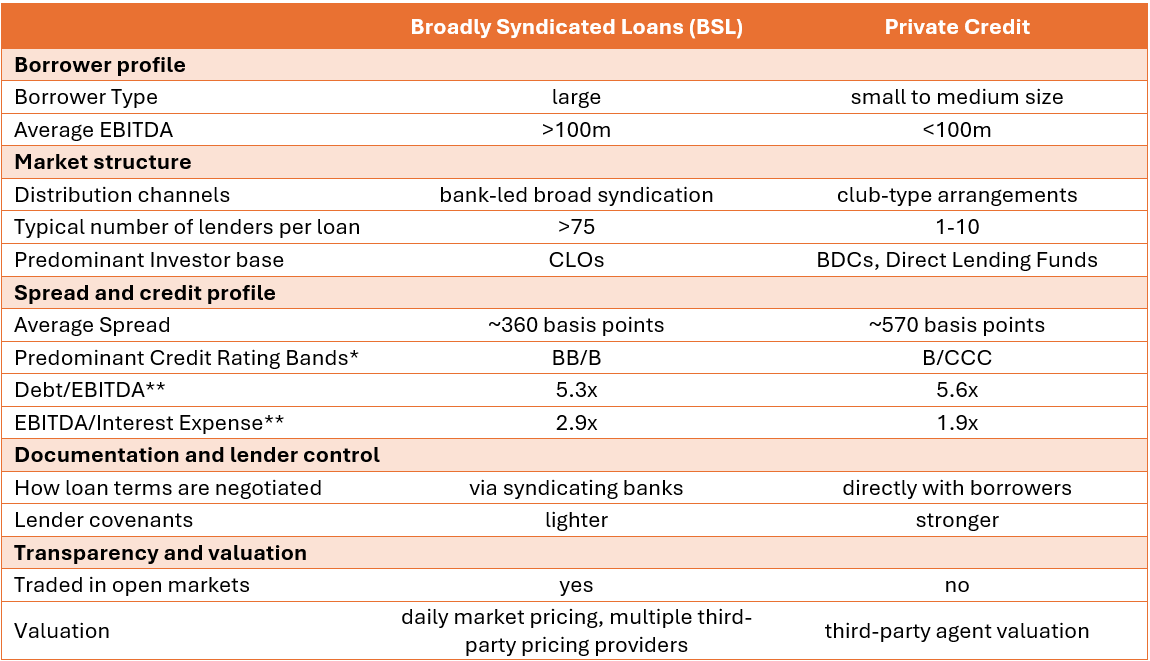

Figure 1: ‘At a glance’ summary of broadly syndicated loans compared to private credit

Source: Janus Henderson Investors, Morgan Stanley, as at 18 March 2026. Past performance does not predict future returns.

* Rating bands are intended as an indication of relative quality, noting that private credit is typically unrated or privately rated.

** Private credit reflects the Fitch average across sectors reported by Morgan Stanley Research; BSL reflects generic single‑B rated credit reported by Morgan Stanley Research, as at Q4 2025.

The differences and why they matter

Borrower profile

Leveraged loan issuers are materially larger than private credit borrowers, which matters as scale affects everything from market access to financial flexibility.

Market structure

The two markets also differ in how loans are originated and distributed. Broadly syndicated loans are arranged for placement across a wide institutional investor base, often involving a large syndicate of lenders, typically over 100 institutional investors. Private credit loans are typically bilateral (or club) transactions provided by only a few lenders. That gives private credit lenders greater control over documentation and amendments, but it also means the loan is not supported by the same depth of market participation and scrutiny. By design, broadly syndicated loans are market instruments whereas private credit loans are negotiated financings.

Spread and credit profile

Private credit generally offers wider spreads than broadly syndicated loans, but that additional spread reflects a different risk and liquidity profile, and lower credit quality (on average), rather than a pricing anomaly (Figure 1). The spread premium therefore offers compensation for these characteristics.

Documentation and lender control

As transactions in private credit are negotiated among a small number of lenders, typically one to ten, covenant packages are somewhat stronger, and amendments can be managed more directly than in the syndicated market. That can be beneficial when a borrower comes under pressure, but it comes with a trade-off. A privately negotiated loan may offer stronger contractual control, yet it remains less transparent and less continuously scrutinised than a broadly syndicated loan.

Transparency and valuation

This leads to the most important distinction of all: price discovery. Broadly syndicated loans benefit from a developed market infrastructure, with independent pricing, dealer contributions and regular price evaluations. Private credit loans, on the other hand, are typically valued periodically through manager- or valuation-agent-led processes. In stressed conditions, this becomes central to how investors experience risk.

Valuation and price discovery: What distressed situations reveal

A stressed credit is often the clearest way to understand how the leveraged finance market functions. The First Brands situation is a useful case study. Sharp price declines were reported in the First Brands’ loans as financing concerns intensified in September 2025 and the prospect of bankruptcy loomed.

As shown in Figure 2, the First Brands broadly syndicated loan traded in the mid-90s in early August 2025, fell to 85 on 15 September, 76.5 on 17 September, 60 on 22 September, 42.5 on 24 September, before temporarily stabilising in the 30s and ultimately marking close to zero by the start of 2026. That sequence is important because it shows the market incorporating new information as the situation deteriorated, rather than in a single valuation event.

Figure 2: First Brands Group market price evolution

Source: Bloomberg, as at 5 January 2026.

The point is not that broadly syndicated loans avoid distress. It is that when credit conditions weaken, the market provides a visible price path through which investors can assess deterioration as it unfolds. Investors can therefore re-evaluate the terminal value of the company and adjust their exposure based on their individual credit rationale.

This contrasts with recent private credit write-downs, where some loans were reportedly marked from par to zero within a single quarter. Rather than evidence of private credit as uniquely risky, these episodes highlight that in private credit markets that receive periodical valuations, changes in valuation can appear in discrete steps rather than through a continuous sequence of market prices.

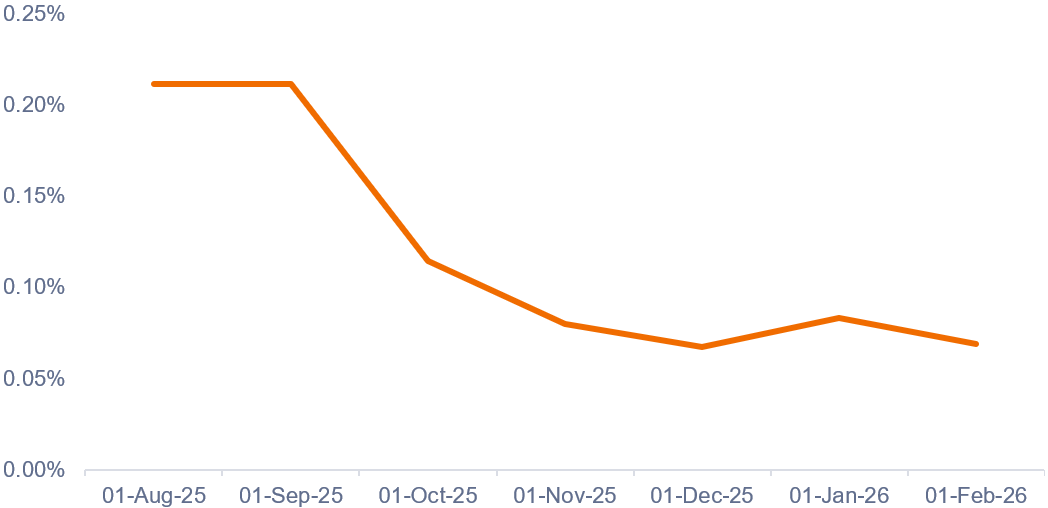

It is also important to separate individual companies’ idiosyncratic credit events from the CLO investor outcome. As shown in Figure 3, average First Brands holdings across European CLOs peaked at approximately 0.2% in mid-2025 and then declined thereafter. CLO exposure to an individual borrower is limited by design, as CLOs benefit from highly diversified portfolios holding around 100-300 loans, depending on jurisdiction. Exposure to any single loan is set by concentration limits within the CLO (around 3% in the US and 2% for European CLOs), which limits the impact of any one default.

Figure 3: First Brands average exposure across European CLOs

Source: Janus Henderson Investors analysis, as at 28 February 2026.

In addition to this diversification in CLOs, investors benefit from embedded protections in the form of subordination and other forms credit enhancement and structural safeguards, such as overcollateralisation (OC) and interest coverage tests.1 Consequently, thus far there has never been a default among A, AA, or AAA-rated CLOs in Europe, even during the Global Financial Crisis. Even in environments of high default rates, structural protections in CLOs have helped to materially reduce losses to BBB and BB-rated tranches.

Liquidity: The key misconception

The most common misunderstanding is to assume that CLO investors rely on underlying loan sales to obtain liquidity. In private credit vehicles that offer periodic liquidity, investors ultimately depend on generating cash from an illiquid underlying portfolio, or from a designated liquidity sleeve; hence why redemption mechanics come under pressure when sentiment weakens.

CLOs are different (as detailed in our Case for CLOs). They are not subject to the same forced-selling dynamics associated with redemption-based structures. CLO liabilities are long term, the structure is match funded, and investor liquidity is therefore provided through the CLO bond market, rather than through sales of the underlying broadly syndicated loans. That distinction is fundamental. It means investors can access and trade their CLO exposure through a well-established and efficiently functioning secondary market, while the underlying loans collateral remains financed within a locked-in capital structure.

Distinction matters

While both private credit and broadly syndicated loans finance leveraged companies, they remain distinct. Broadly syndicated loans sit within a broad institutional market with independent pricing and continuous price discovery, while private credit remains more bespoke, less transparent and less frequently marked-to-market.

That distinction is particularly important in CLOs. These investments finance diversified portfolios of broadly syndicated loans through stable term liabilities. Investor liquidity is delivered through the CLO bond market rather than through redemptions from the underlying collateral pool.

In our view, recent private credit market developments have reinforced rather than weakened the case for making this distinction clear. Broadly syndicated loans may finance privately-owned companies, but in how they are structured or priced, and how investors access liquidity through CLOs, they remain fundamentally different from private credit.

1Mechanisms that ensure that if underlying loans deteriorate, cash flows are redirected to protect senior tranches.

Business Development Companies (BDCs) are regulated investment vehicles that provide private credit to small and mid-sized US businesses, offering investors high-yield income through floating-rate debt.

Club transactions involve multiple non-bank lenders collaborating to provide a loan to a single borrower, offering increased deal certainty, speed, and tailored financing compared to traditional syndicated loans. Popular in large-cap and leveraged buyouts, these deals often feature unified covenants and lower liquidity.

Credit enhancement is used in securitisation to improve the credit quality and ratings of the debt tranches.

Fund sponsor-owned businesses: This refers to companies that are owned and controlled by private equity (PE) firms, rather than being publicly listed or family‑owned.

Manager or valuation agent-led processes: In private credit, manager‑ or valuation agent‑led processes refer to the way loans are periodically valued using internal models and third‑party inputs, rather than through continuous market pricing.

Match funded: CLOs are match‑funded in the sense that stable, long‑term liabilities are aligned with the cashflow profile of broadly syndicated loans, eliminating short‑term funding and redemption risk.

A syndicated loan is a large-scale financing arrangement where a group of lenders (a syndicate), led by one or more lead arrangers, jointly provide funds to a single borrower under a unified loan agreement.

Term liabilities refer to the long‑dated, contractual funding structure used by CLOs to finance their loan portfolios. In practice, CLOs issue tranches of debt and equity with defined maturities, typically ranging from several years to over a decade, rather than relying on short‑term or callable funding.

These are the views of the author at the time of publication and may differ from the views of other individuals/teams at Janus Henderson Investors. References made to individual securities do not constitute a recommendation to buy, sell or hold any security, investment strategy or market sector, and should not be assumed to be profitable. Janus Henderson Investors, its affiliated advisor, or its employees, may have a position in the securities mentioned.

Past performance does not predict future returns. The value of an investment and the income from it can fall as well as rise and you may not get back the amount originally invested.

The information in this article does not qualify as an investment recommendation.

There is no guarantee that past trends will continue, or forecasts will be realised.

Marketing Communication.