Key takeaways:

- As was the case with food delivery, short-form videos, and livestreaming, Chinese consumers and businesses are early adopters of integrating AI into their daily activities.

- Although China largely lacks access to the most powerful chips to develop AI, the country has become adept at distilling western models and have aggressively deployed AI across the economy.

- China has taken the lead in physical AI, building on its previous success in factory automation and electric vehicles.

In April, a team from Janus Henderson’s Global Technology and Innovation Team attended Morgan Stanley’s China Summit in Shenzhen. For some of us, it was our first time visiting the country since the COVID-19 pandemic.

As a global asset manager, we benefit greatly from having investment professionals based in the region. For those of us in the United States, the instantaneous flow of corporate and economic information has never made it easier to analyze companies from a distance. Still, there is no substitute for periodically traveling to meet companies’ management teams, visit their factories, and see their products deployed across the local economy.

Our agenda was packed with topics that one would expect in an era of exceptionally rapid technological innovation. One of the highest priorities was assessing the progress of home-grown AI models for both domestic hyperscalers and smaller labs, seeing how Chinese companies are navigating the “chips challenge” posed by geopolitical factors and evaluating the health of Internet companies’ core businesses of e-commerce, payments, and social media. We also carved out time to explore progress in physical AI, including factory automation and robotaxis.

Getting situated … finally

Even in our travels to China prior to the pandemic, we were astounded by the degree to which Chinese consumers live their lives digitally. E-commerce, payments, and social media engagement all seemed years ahead of what American or European consumers were comfortable with. If anything, the pandemic accelerated those trends. In the same vein, Chinese companies and consumers appear more willing to embrace AI. In a telling example, over 50% of independently released songs in China last year were AI generated.

The Shenzhen skyline – barely a generation old

Source: Janus Henderson Investors.

The wholesale adoption of a digital economy was brought home upon one team member’s arrival in the country. After assiduously seeking to exchange U.S. dollars for renminbi, we soon learned that no one accepts cash – not taxis, not coffee shops, no one. Downloading Alipay and Weixin Pay – the dominant Chinese payment apps – is complicated, as many Western companies restrict corporate phone usage within certain countries, thus requiring a loaner phone for temporary use.

Having recreated our digital identities to access payment functionality, we quickly learned that still more apps – e.g., maps and search – must be downloaded, as their western counterparts are inaccessible and are only available in Chinese.

It was a good reminder that, from a digital perspective, China largely operates as a closed economy – a fact that has investment implications we’ll discuss below.

Chinese Internet: A bruising competitive landscape

Having innovative products and a willing customer base doesn’t necessarily translate to resilient business models. Heavy investment and fierce competition are bringing that reality home to China’s major Internet platforms. The upshot is compressed operating margins across cloud, food delivery, and e-commerce businesses. And as AI has the potential to further disrupt these segments, companies have little choice but to continue the investment cycle to keep up with the competition. Ultimately, we found the current state of Internet companies not conducive for generating return on invested capital – a metric we follow closely as a gauge for long-term investment success.

Another obstacle for international investors is the aforementioned closed nature of China’s digital economy. A question for consideration is whether it’s worth the effort to gain exposure to a roughly 1.4 billion-person market where noneconomic priorities such as national service can potentially influence corporate strategy, or instead focus on Western Internet platforms that can access billions of customers across all continents.

A rejoinder to this argument, however, is that the central government in China has reverted to a more accepting stance toward private technology companies than it had exhibited over the past few years. Behind this promotion of national champions is the government’s recognition that an innovative private sector can be useful in achieving national priorities. This extends across the tech sector. At stake is not only national prestige but also geopolitical considerations, including military power and dominating ascendant industries such as electric vehicles.

Also welcoming is a stabilizing economic backdrop after years of significant headwinds for consumers, largely due to a precipitous decline in property values.

The (new) commanding heights

As is the case in the United States, China’s Internet behemoths (e.g., Alibaba, Tencent, Bytedance) are leading the charge in AI investment. Yet there are several scrappy labs developing their own AI models.

Both categories largely depend on distilling more advanced Western models. This approach is owed to restrictions placed on the export of advanced U.S.-designed graphics processing units (GPUs). China’s need for creativity has yielded some impressive results, with DeepSeek’s 2025 splash the most telling example. Also helping the cause is much AI research likely circumventing GPU restrictions by accessing offshore data centers.

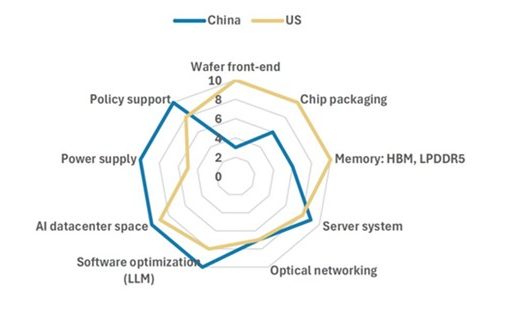

A comparison of U.S. and China AI infrastructure

While the U.S. has the resources to advance frontier models, China has extensive power supply and policy support to more rapidly deploy AI across the economy.

Source: Janus Henderson Investors.

Not only does a lack of access to the most advanced GPUs inhibit China’s ability to develop frontier AI models, but it also presents a challenge with respect to energy efficiency. Alibaba, for example, expects to generate $100 billion in AI-related revenue on its cloud within five years. Achieving this will require 25 gigawatts of electricity – translating to roughly $4 billion in revenue per gigawatt.

In the U.S., with its more energy-efficient chips, the industry benchmark is $10 billion to $12 billion of revenue per installed gigawatt. Over time this friction could act as an opportunity cost that diminishes China’s returns on its sizeable AI investment.

What China may lack in cutting-edge AI model training, it makes up for with a customer base more willing to adopt AI in their personal and professional lives, compared to varying levels of skepticism in North America and Europe. China, after all, has been on the forefront of other digital innovations, including livestreaming, short-form videos, and quick commerce. This trend has continued in the AI era, as illustrated by the music example and rise of AI-generated microdramas.

Such adoption could have ramifications far beyond China. Should Western consumers adjust their behaviors in a similar manner by accepting artificially generated content, it could represent another attractive earnings stream for AI platform providers – but a potential threat that legacy entertainment services would have to address.

In some respects, China’s lack of access to the most advanced GPUs could yield unexpected benefits. Rather than fully participating in the (expensive) arms race of developing the most sophisticated frontier models, China is instead concentrating its efforts on distilling others’ models and seeking practical applications for them – hence the country’s rapid adoption of the technology. Put more succinctly, what China lacks in high-end AI capabilities, it more than compensates for in deployment. And as AI moves from the training phase toward inference, access to the most powerful GPUs could be less of a headwind, as AI agents lean more heavily on central processing units and memory chips when executing tasks.

In a similar vein, we expect that China will attempt to leverage its AI models on the back of its massive advantage in cheap power generation to export tokens – the fundamental units of data processed by models – on an industrial scale for various use cases and applications across the world. This would be the latest chapter in the playbook China has used over the past 25 years when it became the low-cost manufacturer across myriad industries.

Physical AI: The rise of humanoids?

The subject that made the greatest impression on us – and where China has a clear lead over the West in both innovation and adoption – is physical AI. The rather shocking advancements are the result of a marriage between existing automation and AI models. The presence of physical AI is most evident on factory floors. Albeit methodical, progress is also being made with humanoid robotics. Across applications, locomotion has come a long way, but manipulation – e.g., executing specific tasks typically done with hands – is still in its early stages.

An AI-enabled surveillance humanoid taking a stroll through a park

Source: Janus Henderson Investors.

Physical AI also lacks the massive data catalog that has propelled large language models (LLMs) in recent years. But as with LLMs, the deployment of AI robotics should create a feedback loop where wider usage creates additional data which can then be utilized to improve models and expand use cases, thus driving scale.

The area where we see physical AI likely magnifying an existing competitive advantage for China is robotaxis. A combination of innovation and policy support has resulted in China becoming the world leader in electric vehicles (EVs). Should trade barriers be lowered, global domination would likely not be far behind.

The second derivative of China’s embrace of EVs is innovative automakers integrating AI throughout the vehicle, thus improving the functionality of driverless vehicles. This reflects the segmentation of broader physical AI that we noticed during our visit. EV producers represent an existing hardware lane, but physical AI is also being developed across ecosystems and model-first companies charting their own path.

Attractively priced Chinese EVs are plausible platforms for a fleet of robotaxis

Source: Janus Henderson Investors.

Closing words

In summary, our visit to China left us with two indelible impressions. First, the country’s tech sector is a case study of what’s next, not only in the field of physical AI but also in terms of how AI can be deployed across the consumer and corporate economy. But it also reminded us that, as investors, we cannot simply become enamored with the shiny new object – there must be an acceptable return on investment behind it. A heavy investment cycle, fierce competition, and margin compression all represent headwinds on this front.

Even in a world where economic decoupling seems inevitable, technologies and their application tend to spread across borders. For this reason, we foresee many more trips to China as the country charts a unique – and in many instances, groundbreaking – path in the AI era.

IMPORTANT INFORMATION

Artificial intelligence (“AI”) focused companies, including those that develop or utilize AI technologies, may face rapid product obsolescence, intense competition, and increased regulatory scrutiny. These companies often rely heavily on intellectual property, invest significantly in research and development, and depend on maintaining and growing consumer demand. Their securities may be more volatile than those of companies offering more established technologies and may be affected by risks tied to the use of AI in business operations, including legal liability or reputational harm.

Technology industries can be significantly affected by obsolescence of existing technology, short product cycles, falling prices and profits, competition from new market entrants, and general economic conditions. A concentrated investment in a single industry could be more volatile than the performance of less concentrated investments and the market as a whole.

Foreign securities are subject to additional risks including currency fluctuations, political and economic uncertainty, increased volatility, lower liquidity and differing financial and information reporting standards, all of which are magnified in emerging markets.

Return On Invested Capital (ROIC) is a measure of how effectively a company used the money invested in its operations.

These are the views of the author at the time of publication and may differ from the views of other individuals/teams at Janus Henderson Investors. References made to individual securities do not constitute a recommendation to buy, sell or hold any security, investment strategy or market sector, and should not be assumed to be profitable. Janus Henderson Investors, its affiliated advisor, or its employees, may have a position in the securities mentioned.

Past performance does not predict future returns. The value of an investment and the income from it can fall as well as rise and you may not get back the amount originally invested.

The information in this article does not qualify as an investment recommendation.

There is no guarantee that past trends will continue, or forecasts will be realised.

Marketing Communication.