Key takeaways:

- Stock-bond correlations are shifting, challenging the assumption that traditional portfolio building blocks provide consistent, reliable offsets across different market environments.

- As correlations rise, portfolios become more exposed to common macro drivers, increasing volatility and reducing the effectiveness of historically reliable sources of diversification.

- In a higher correlation environment introducing diversified, liquid alternatives with low correlation increases in importance and can help restore portfolio efficiency, offering additional resilience when traditional asset relationships become less dependable.

Some things feel permanent. Others only seem that way, shaped by the narrow window of time we observe. Earth’s magnetic field offers a useful illustration. Its poles appear constant, yet they have flipped repeatedly over geological history, typically every 200,000 to 300,000 years. What seems stable within human experience is, in reality, in motion, with the northern magnetic pole continuing to drift, most recently towards Siberia. What looks like a wobble will, in time, become a more enduring shift.

Similarly, for much of the 21st Century, investors have treated the negative correlation between equities and bonds as a near-constant. When growth faltered and equities fell, bonds more often rallied. This dynamic has underpinned portfolio construction, acting as a dependable source of diversification within portfolios.

Stock-bond correlations are not fixed

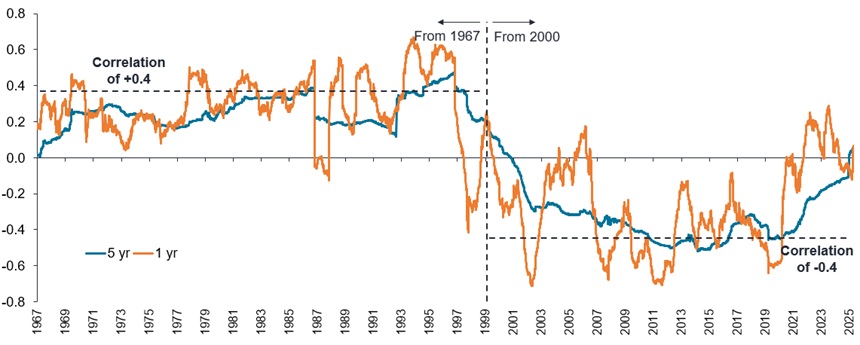

The negative correlation between equities and bonds is a familiar modern paradigm that has persisted through a period of low inflation and accommodative fiscal and monetary policy. But from the mid-1960s to the end of the 20th Century, equities and bonds were positively correlated, in a period characterised by persistently higher inflation and less government stimulus (Exhibit 1).

Exhibit 1: S&P 500/US 10-year bond correlation from 1967

Source: Janus Henderson Investors, as at 22 April 2026.

Note: There is no guarantee that past trends will continue, or forecasts will be realised. Past performance does not predict future returns.

The argument here is that correlations between asset classes can change, and that change can persist for sustained periods. If so, the recent shift towards a more consistently positive stock-bond correlation may be less an anomaly and more an early signal of deeper structural change, with implications for long-term capital market assumptions (LTCMAs) and asset allocation.

Yet most conversations around LTCMAs still gravitate toward familiar questions: are expected returns too low because growth could surprise to the upside, or too high because starting valuations leave less room for error? Far less attention is paid to how these building blocks interact, and how stable those relationships really are. For strategic asset allocation, those relationships can matter as much as the return and volatility assumptions.

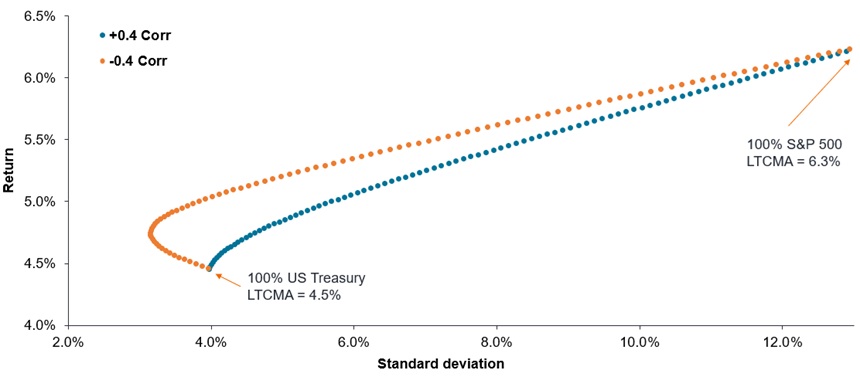

How correlations shape the efficient frontier

Consider a simple scenario. Rather than forecasting a new world of returns, yield curves, and volatilities, what if we hold long-term assumptions constant and change just one input: the correlation between equities and bonds?

In a representative ‘negative correlation’ world (modelling a long-term average around -0.4) the efficient frontier (the highest expected return for a defined level of risk, in this case for a portfolio split between equities and bonds) tends to bow outward. Having the right blend of equities and high-quality bonds may deliver a smoother path than either asset class can achieve alone. However, if we shift that to an equivalent positive correlation environment, the frontier visibly flattens. In other words, equity/bond portfolios behave differently in different correlation regimes (Exhibit 2).

Exhibit 2: Correlations matter to efficient frontiers

Source: Janus Henderson Investors, as at 14 April 2026. Shows efficient frontiers for equities and bonds at -0.4 and +0.4 correlation. There is no guarantee that past trends will continue, or forecasts will be realised. Past performance does not predict future returns.

What this shift from negative equity-bond correlation to positive shows us is that the benefit of holding both assets does not vanish, but it becomes less potent. With everything else unchanged, volatility can rise meaningfully because both sides of the portfolio are responding to the same macro impulse.

The point here is not to argue that +0.4 is the new ‘normal’, but to show that a plausible regime shift changes what is achievable through traditional diversification, even before you adjust any return assumptions.

Reshaping the efficient frontier

If that is the challenge, the response is not to abandon strategic asset allocation, but to recognise that the efficient frontier is not fixed. It can be reshaped by introducing alternative assets that provide real diversification when equities and bonds are less dependable offsets.

This is where the idea of an ‘effective alternative’ becomes useful. Alternatives are a broad church: some are simply different wrappers around familiar premia, while others can provide genuinely distinct sources of potential return.

For portfolio construction purposes, we believe an effective alternative could be one that is built with three core attributes:

- Attractive Sharpe ratio: An effective alternative should stand on its own merits, with a risk-adjusted profile that is additive, rather than a drag on portfolio efficiency.

- Low correlations to traditional risk assets: Diversification should be observable in real time, rather than a consequence of delayed or opaque pricing.

- Complementary distribution: It is not enough to be ‘uncorrelated on average’; the pattern of returns should be helpful in areas that address risk management.

This intentionally emphasises the importance of real diversification. Some assets can show limited correlation to public markets while still being economically exposed to the same underlying premia (eg. private equity strategies where values are typically updated quarterly, creating a lag in observed pricing). This can make returns appear smoother and correlations lower over shorter horizons, rather than exhibiting real structural differentiation.

Restoring efficiency in a higher correlation regime

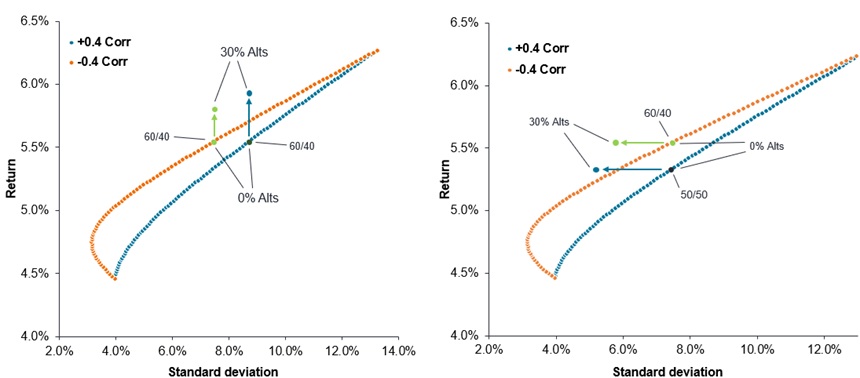

To illustrate the mechanics, let us consider a model liquid alternative with a mid-single-digit expected return (5.5% per annum), modest volatility (4.5%), and zero correlation to both equities and fixed income.

What is the impact of introducing an allocation between 5% and 30% of this model liquid alternative to a balanced portfolio? An uncorrelated return stream can bend the efficient frontier outward again, partially restoring the efficiency that is lost when equity-bond correlations rise (Exhibit 3).

Exhibit 3: Diversifying assets are more important in an increasingly correlated world

Source: Janus Henderson, as at 14 April 2026.

Note: Model portfolios are used here for illustrative purposes only and do not represent actual performance of any client account. There is no guarantee that past trends will continue, or forecasts will be realised. Past performance does not predict future returns.

Any factor that helps to regain efficiency can give allocators choices about how to use it, reducing volatility for a given return objective, improving expected return for a given risk budget, or some combination of the two.

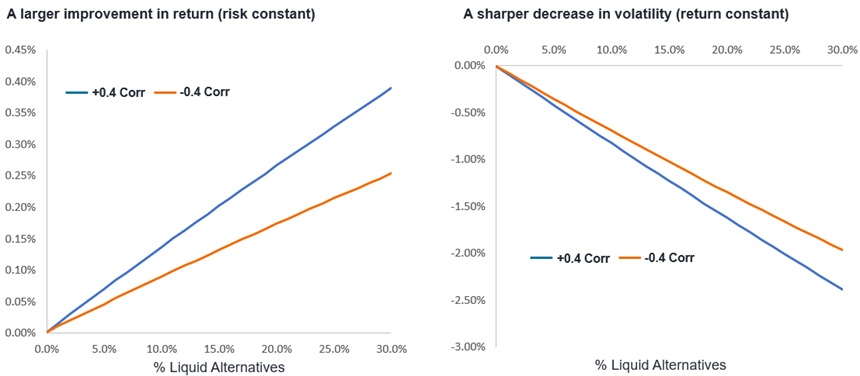

Crucially, the more correlated a core portfolio becomes, the more valuable that diversifying sleeve tends to be. When equities and bonds already diversify each other strongly, adding another diversifier can still help, but the marginal gain is naturally smaller. But when equities and bonds move together more often in a more closely correlated environment, the same allocation has greater capacity to provide diversification, and its impact on portfolio outcomes becomes more pronounced (Exhibit 4).

Exhibit 4: Diversifying assets improve the risk and volatility profile in periods of higher correlation

Source: Janus Henderson Investors, as at 14 April 2026. This is a theoretical model that introduces a liquid alternative to a ‘balanced’ portfolio split with 60% exposure to equities (S&P 500 Index), and 40% US Treasuries, using LTCMAs. For illustrative purposes only. There is no guarantee that past trends will continue, or forecasts will be realised. Past performance does not predict future returns.

Conclusion

If the recent shift towards more positive stock–bond correlations marks the start of a more persistent regime, then the assumptions embedded in many portfolios may be less robust than they appear. Diversification, long treated as a given, becomes conditional on the environment in which it is applied.

What appears stable may simply reflect the conditions of a particular period. Relationships that come to feel constant can shift, sometimes abruptly, in ways that materially alter portfolio outcomes. The implication is not simply to revisit long-term capital market assumptions, but to challenge the role that correlation plays within them.

This, in turn, puts pressure on investors to adapt, to reassess how diversification is constructed, and to reconsider the role of allocations that can provide resilience when traditional relationships break down. As the environment evolves, so too must the toolkit for how portfolio diversification is built.

—–

Important information:

Diversification neither assures a profit nor eliminates the risk of experiencing investment losses.

These are the views of the author at the time of publication and may differ from the views of other individuals/teams at Janus Henderson Investors. References made to individual securities do not constitute a recommendation to buy, sell or hold any security, investment strategy or market sector, and should not be assumed to be profitable. Janus Henderson Investors, its affiliated advisor, or its employees, may have a position in the securities mentioned.

Past performance does not predict future returns. The value of an investment and the income from it can fall as well as rise and you may not get back the amount originally invested.

The information in this article does not qualify as an investment recommendation.

There is no guarantee that past trends will continue, or forecasts will be realised.

Marketing Communication.