Chart to Watch: Monitoring low levels of systemic risk in U.S. equities

We view the lack of systemic risk priced into the market as the culprit for correlations among U.S. equities being near historic lows. An increase in systemic risk could result in investors demanding a higher risk premium.

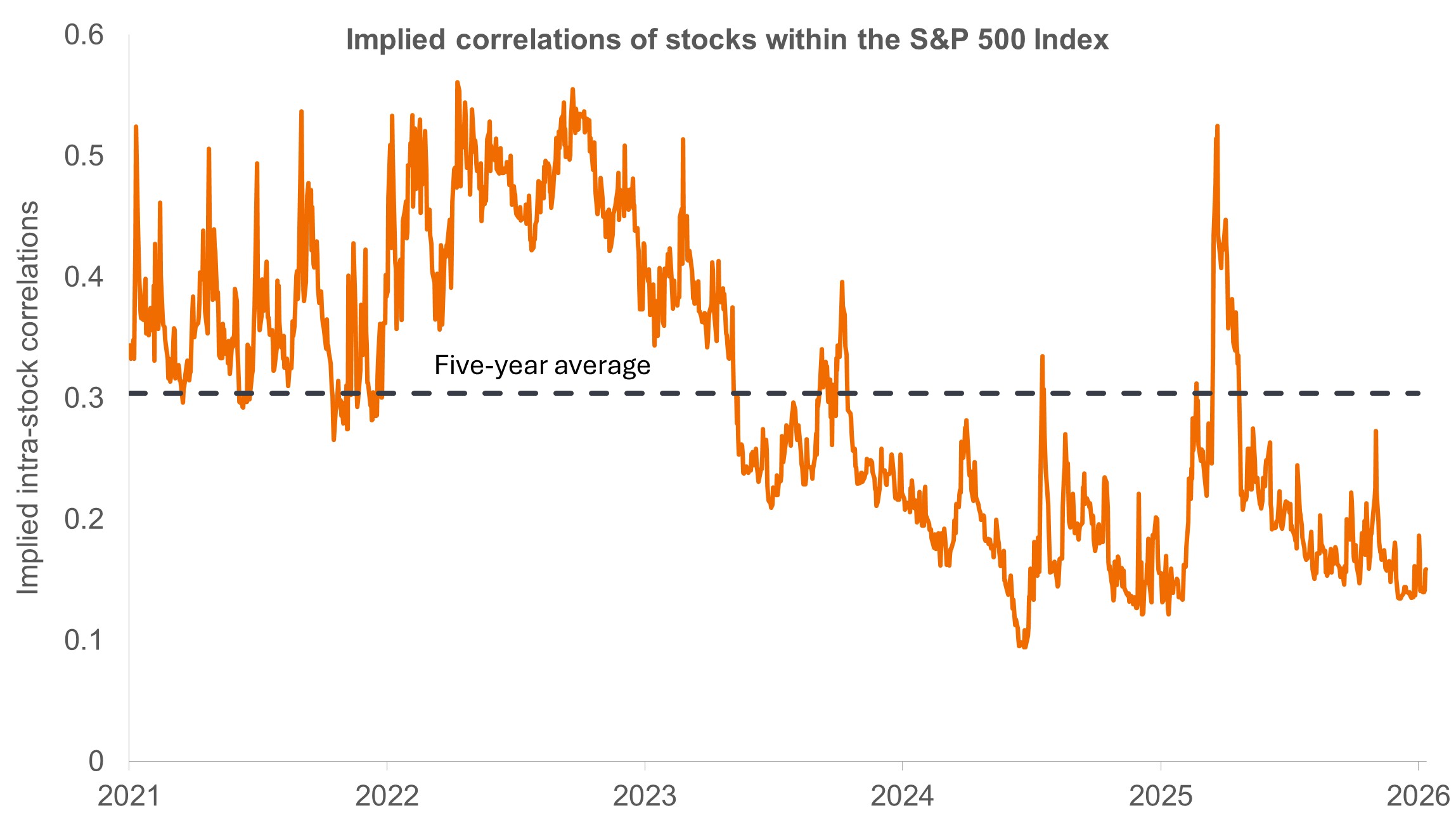

Given that it is widely accepted that correlations among individual stocks can only fall to 0, the current level of 0.17 is notable, as it resides well below its 5-year average of 0.30.

Source: Janus Henderson Investors, Bloomberg, as of 20 January 2026.

"Low correlations mean that U.S. equities are behaving like a ‘market of stocks’ rather than a ‘stock market’. Rising correlations – likely due to the market reflecting an increase in systemic risk – could put downward pressure on earnings multiples, thus becoming a catalyst for a market drawdown.” -Ashwin Alankar, Ph.D.

Key takeaways

- Implied correlations among U.S. equities are near historic lows, indicating a high level of idiosyncratic risk and, thus, peculiarly low levels of systemic risk.

- Mean reversion in systemic risk could lead to investors demanding additional compensation for being exposed to non-diversifiable risk.

- With much of 2025’s rally driven by multiple expansion, the demand for a higher equity risk premium could lead to an equities drawdown as valuations compress.

We view the lack of systemic risk priced into the market as the culprit for low correlations. Aware that rising systemic risk could impact a portfolio, investors would demand additional compensation in the form of a higher risk premium. In practical terms, this would likely be expressed through compressed price-earnings (P/E) ratios.

Equities follow earnings and the demand for risk premiums. Identifying changes in these variables – in this case, possibly higher levels of systemic risk – may help enable investors allocate accordingly, thus allowing them to stay invested while potentially reducing the risk of extreme drawdowns. Once systemic factors are accurately reflected, investors can then reallocate back to less-defensive stocks to potentially take advantage of more favorable risk premiums.

Systemic risk is a source of price volatility in financial markets that cannot be diversified away by holding a larger number of securities.

Idiosyncratic risk is a source of price volatility that is specific to an individual security meaning that much of this risk can be diversified away by holding a large number of securities that tend not to be correlated with each other.

Multiple expansion describes the valuation metric – e.g. the P/E ratio – of an equity increasing, meaning that an investor is willing to pay a higher amount to purchase a security.

Earnings Multiples are a category of valuations attached to security that indicate how much a buyer is willing to pay per a unit of earnings. For example, a P/E ratio of 14 means the market assigns a value of $14 dollars $1 of earnings.

Correlation measures the degree to which two variables move in relation to each other. A value of 1.0 implies movement in parallel, -1.0 implies movement in opposite directions, and 0.0 implies no relationship.

Price-to-Earnings (P/E) Ratio measures share price compared to earnings per share for a stock or stocks in a portfolio.

S&P 500® Index reflects U.S. large-cap equity performance and represents broad U.S. equity market performance.

Past performance is no guarantee of future results.

These are the views of the author at the time of publication and may differ from the views of other individuals/teams at Janus Henderson Investors. References made to individual securities do not constitute a recommendation to buy, sell or hold any security, investment strategy or market sector, and should not be assumed to be profitable. Janus Henderson Investors, its affiliated advisor, or its employees, may have a position in the securities mentioned.

Past performance does not predict future returns. The value of an investment and the income from it can fall as well as rise and you may not get back the amount originally invested.

The information in this article does not qualify as an investment recommendation.

There is no guarantee that past trends will continue, or forecasts will be realised.

Marketing Communication.