Banking on European bank bonds

For credit investors, the banking sector is a crucial area to get right. Credit analysts Soline Poulain and Richard Thomson, and fixed income portfolio manager Tim Winstone, discuss the fundamental outlook for European bank bonds and which parts of this sector currently look the most attractive.

7 minute read

Key takeaways:

- For managers of investment grade credit, allocation decisions relating to the banking sector vis-a-vis other corporate bonds are typically crucial to achieving strong benchmark-relative performance.

- Despite the strong rally that began in the last quarter of 2023, we continue to see pockets of value among European banks and foresee further spread tightening. Solid fundamentals and a lower supply outlook for 2024 underpin our selective overweight position.

- Most European banks are in a strong position to face the muted economic outlook. Our focus within the sector is on banks with the best ability to withstand a macro downturn (e.g., those notable for the diversity of their loan books, stability of their earnings and solidity of their capital).

Most credit fund managers will agree that the allocation decision on banks versus corporate bonds is one of the most meaningful calls they can make to beat a particular benchmark. With that in mind, in this article we will look at the recent performance of European banks relative to their corporate counterparts, the fundamental outlook for the banking sector and which parts of the sector currently look the most attractive.

Banks have outperformed corporates in the credit rally

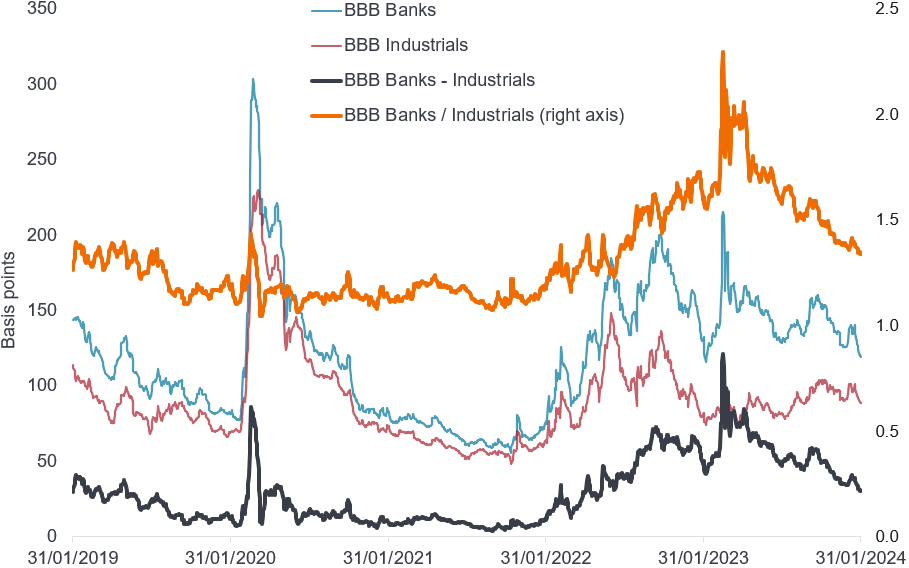

European bank bonds have been among the best performers in the credit market rally that began around mid-October 2023.1 On aggregate, BBB-rated bank bonds now (as of 31 January 2024) offer 1.3 times the spread of similar-rated corporate bonds, an impressive compression since March 2023, when – in the wake of the Credit Suisse’s collapse – the spread pick-up of bank bonds over corporate bonds peaked at a multiple of 2.3 times.2 At around 120 basis points (bps) over swap rates currently, bank bond spreads are on aggregate around the five-year average but they remain higher than they were in late 2021, when they reached a five-year tight below 60bps.3 The outperformance of bank bonds relative to corporate bonds in the second half of 2023 reflects returning investor confidence in banks as many bank results repeatedly beat consensus expectations and as the dust settled on the Credit Suisse event in March.

Figure 1: BBB-rated banks versus industrials bond spread

Source: Janus Henderson Investors based on Bloomberg (Euro-Aggregate Index, filtered by rating and by sector as per Bloomberg Fixed Income Classification System). Data as of 31 January 2024. Past performance does not predict future returns.

Valuations are supported by solid fundamentals

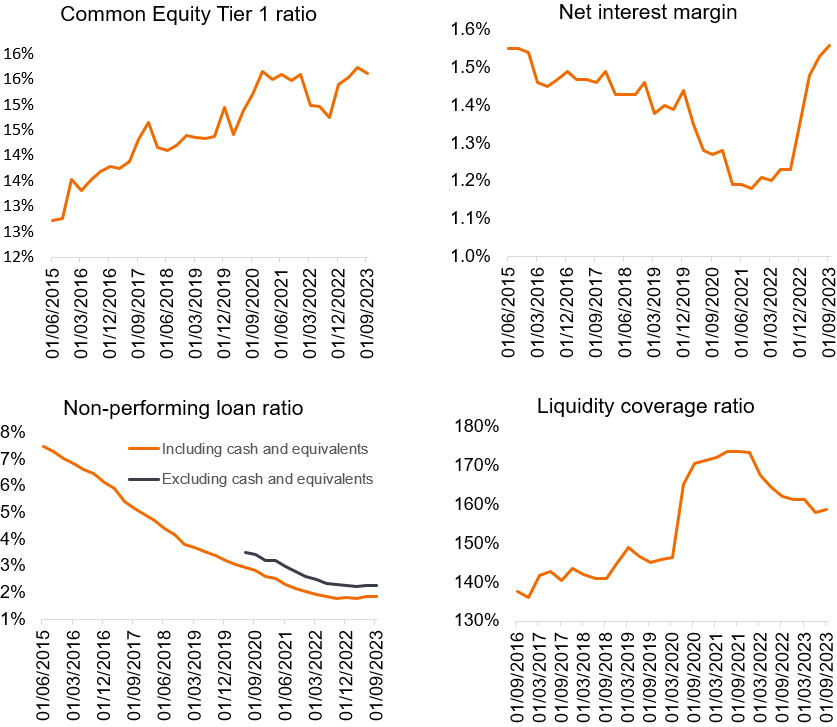

European banks’ fundamentals currently look very solid. In fact, fundamentals are the most solid they have been since the Global Financial Crisis (GFC). As of 30 September 2023, the Common Equity Tier 1 ratio for European banks stood at 15.6% on aggregate – offering a substantial buffer over and above regulatory requirements despite the rapid pace of capital distributions over the past couple of years.4

Profitability is the highest it has been in many years as banks have seen a remarkable rebound in net interest income – typically their greatest source of revenue – as net interest margins have expanded on the back of the tighter monetary policy and low deposit betas (the sensitivity of deposit rates to higher interest rates).

Asset quality has gradually improved over the past years, with non-performing loans at record low levels since the GFC. European banks also booked precautionary provisions during the COVID crisis, which they have often recycled into provisions for macro risk. There is little doubt that asset quality will deteriorate as borrowers suffer from weaker growth, sustained inflation and higher borrowing costs, but we believe most banks are in a solid position to face the muted economic outlook, and that the deterioration will be gradual and manageable overall.

Figure 2: Snapshot of European banks’ fundamentals

Source: European Central Bank, Supervisory Banking Statistics. Data as of 30 September 2023. Note: Charts show aggregate data for banks in countries participating in the Single Supervisory Mechanism (changing composition over years).

Supply likely to be lower in 2024

We don’t expect supply to weigh on bank bond performance to the same extent as it did in 2023. In 2023, European bank bond supply was particularly heavy, totalling around €400 billion across currencies (up from €359 billion in 2022). This large amount was largely driven by the issuance of eligible senior debt bonds to build the required bail-in debt buffers (MREL – minimum requirement for own funds and eligible liabilities) ahead of the deadline on 1 January 2024. Banks also came to the market to refinance Targeted Longer-Term Refinancing Operations (TLTRO – funds from the European Central Bank) funding. There is further TLTRO funding maturing in 2024, but substantially less so than in 2023. Issuance volumes in 2023 were also likely further affected by an overhang from 2022 when issuance windows were limited.

With those factors largely behind us and loan growth expected to be sluggish, we expect supply to be lower in 2024 – also noting that most banks have the option to use covered bonds as an alternative source of funding.

Figure 3. European bank supply, all currencies (Euro equivalent)

Source: Société Générale Flow Strategy & Solutions – Credit based on Bloomberg data. Data as of 31 January 2024. Numbers include bonds with a minimum size of €300m.

We see pockets of value in the sector

The solid fundamental position and the expectation of lower supply-driven heaviness compared to 2023 are grounds for a selective overweight position. Valuations have come a long way in the later part of last year, but we expect further tightening supported by these factors.

The biggest risk in our view is an external shock or an idiosyncratic event at a weak entity that would erode market confidence; such a shock could come from macroeconomic or monetary policy indicators, increased geopolitical tensions or political agendas. Bank bonds typically underperform in a market sell-off as the typically superior liquidity of bank paper means investors are often able to offload bank bonds first, pushing bank spreads wider.

To express our confidence in banks’ fundamentals whilst acknowledging the downside risk of an external shock, our focus has been on banks with the best ability to withstand a macro downturn, focusing notably on the diversity of their loan books, the stability of their earnings and the solidity of their capital. We have also participated in primary issues, which we believe can be an attractive way to add bank bond risk if the bond is issued with a new issue premium (NIP). We estimate such NIP on bank bonds issued in January have been on average 10bps over our estimated fair value and, in rare occasions, substantially more than that.

We have complemented our core bank holdings with a modest position in a very selective basket of Additional Tier 1 (AT1) bonds in the second half of last year. We believe certain AT1 bonds have an attractive risk-reward profile as they offer a meaningful pick-up to the most senior parts of bank debt stacks. We have not only selected AT1 bonds issued by banks we see as solid, but also focused on bonds which have calls in the short term (2024 and 2025) and have a high reset after call, which means it makes economic sense for these banks to call, or bonds with a regulatory incentive to redeem. Several of these bonds have already been redeemed, which has yielded a significant upside, and we expect the remaining AT1s we invested in to be called at their first call date.

1 Source: Bloomberg, as of 31 January 2024.

2 Source: Bloomberg, as of 31 January 2024.

3 Source: Bloomberg Euro-Aggregate Index, as of 31 January 2024.

4 Source: Janus Henderson and European Central Bank

Additional Tier 1 (AT1) bonds. Deeply subordinated bonds issued by banks that contribute to the total level of capital they are required to hold by regulators. Created after the Global Financial Crisis of 2007-09 with the intention to reduce the need for government-funded bank bailouts, AT1 bonds absorb losses when the issuing bank’s regulatory capital ratio falls below a certain level.

Asset allocation. The allocation of a portfolio between different asset classes, sectors, geographical regions, or types of security, to meet specific objectives of risk, performance or time horizon.

Basis point (bp). One basis point equals 1/100 of a percentage point. 1 bp = 0.01%, 100 bps = 1%.

Benchmark. A standard (usually an index) against which an investment portfolio’s performance can be measured.

Common Equity Tier 1 (CET1) capital ratio. An indication of a bank’s financial strength; a gauge of a bank’s ability to absorb losses without disruption to its regular operations. The ratio compares a bank’s core equity capital (primarily common stock) with its total risk-weighted assets.

Covered bonds. Debt instruments secured by a cover pool of mortgage loans to which investors have a preferential claim in the event of default.

Credit spread. The difference in yield between a corporate bond and a benchmark rate (e.g., yield on a government bond). It gives an indication of the additional risk that lenders take when they buy corporate debt versus government debt of the same maturity. Widening spreads generally indicate a deteriorating creditworthiness of corporate borrowers, while narrowing indicate improving.

Fundamental analysis. The analysis of information that contributes to the valuation of a security, such as a company’s earnings or the evaluation of its management team, as well as wider economic factors.

Holdco / Opco bond. Debt issued by a bank’s holding company (Holdco) or one of its operating entities (Opco).

Investment grade. A bond typically issued by governments or companies perceived to have a relatively low risk of defaulting on their payments, reflected in the higher rating given to them by credit ratings agencies.

Minimum requirement for own funds and eligible liabilities (MREL). Banks established in the European Union are required to maintain at all times a minimum requirement for own funds and eligible liabilities (MREL) to facilitate the implementation of a resolution strategy that does not depend on the provision of public financial support. MREL targets are set by EU resolution authorities in consultation with prudential supervisors and tailored to bank-specific features.

Monetary policy. The policies of a central bank, aimed at influencing the level of inflation and growth in an economy. It includes controlling interest rates and the supply of money. Monetary stimulus refers to a central bank increasing the supply of money and lowering borrowing costs. Monetary tightening refers to central bank activity aimed at curbing inflation and slowing down growth in the economy by raising interest rates and reducing the supply of money.

Net interest margin (NIM). An indicator of a bank’s profitability. It compares the amount of money the bank is earning in interest on loans and other interest-bearing securities relative to interest paid on funding.

New-issue premium. The new-issue premium is the positive difference between the spread at which the new bond is issued and the estimated fair value of that bond based on the issuer’s curve, comparable secondary transactions and the analyst’s fundamental credit view.

Non-performing loan (NPL). A loan where the borrower is failing to make scheduled payments for a specified period of time.

Primary bond issues. In primary markets, issuers first sell bonds to investors to raise capital. In secondary markets, existing bonds are subsequently traded among investors.

Provisions. Funds set aside by a business to cover specific anticipated future charges or, more specifically for banks, losses on loans.

Swap spread. A swap spread is the basis point spread over the interest-rate swap curve and is a measure of the credit risk of a bond.

Targeted Longer-Term Refinancing Operations (TLTRO). The targeted longer-term refinancing operations (TLTROs) are Eurosystem operations that provide financing to credit institutions. By offering banks long-term funding at attractive conditions, they preserve favourable borrowing conditions for banks and stimulate bank lending to the real economy. The TLTROs, therefore, reinforce the European Central Bank’s current accommodative monetary policy stance and strengthen the transmission of monetary policy by further incentivising bank lending to the real economy.

Tier 2 bonds. Tier 2 bonds form an essential component of the second layer of banking capital known as Tier 2 capital. They are categorised as subordinated debt, meaning they are paid back only after higher-ranking debts have been settled in the event of a bank’s liquidation or bankruptcy.

Important information

Volatility measures risk using the dispersion of returns for a given investment.

Credit Spread is the difference in yield between securities with similar maturity but different credit quality. Widening spreads generally indicate deteriorating creditworthiness of corporate borrowers and narrowing indicate improving.

Swaps, if any, are reported based on notional exposure.

There is no guarantee that past trends will continue, or forecasts will be realised.

Fixed income securities are subject to interest rate, inflation, credit and default risk. The bond market is volatile. As interest rates rise, bond prices usually fall, and vice versa. The return of principal is not guaranteed, and prices may decline if an issuer fails to make timely payments or its credit strength weakens.

High-yield or “junk” bonds involve a greater risk of default and price volatility and can experience sudden and sharp price swings.

Beta measures the volatility of a security or portfolio relative to an index. Less than one means lower volatility than the index; more than one means greater volatility.

These are the views of the author at the time of publication and may differ from the views of other individuals/teams at Janus Henderson Investors. References made to individual securities do not constitute a recommendation to buy, sell or hold any security, investment strategy or market sector, and should not be assumed to be profitable. Janus Henderson Investors, its affiliated advisor, or its employees, may have a position in the securities mentioned.

Past performance does not predict future returns. The value of an investment and the income from it can fall as well as rise and you may not get back the amount originally invested.

The information in this article does not qualify as an investment recommendation.

Marketing Communication.

7 minute read

Key takeaways:

- For managers of investment grade credit, allocation decisions relating to the banking sector vis-a-vis other corporate bonds are typically crucial to achieving strong benchmark-relative performance.

- Despite the strong rally that began in the last quarter of 2023, we continue to see pockets of value among European banks and foresee further spread tightening. Solid fundamentals and a lower supply outlook for 2024 underpin our selective overweight position.

- Most European banks are in a strong position to face the muted economic outlook. Our focus within the sector is on banks with the best ability to withstand a macro downturn (e.g., those notable for the diversity of their loan books, stability of their earnings and solidity of their capital).