Key takeaways:

- Hong Kong’s residential property market bottomed in mid‑2025, with secondary prices now around 10% above the Q2 2025 trough and momentum accelerating across both rents and transactions.

- Structural drivers—interest rate cuts, strong equity market wealth effects, immigration schemes, and declining supply—have materially improved demand, pushing some rentals to record highs and reviving primary market sales.

- Residential developers’ share prices have re‑rated sharply, but despite this rebound, valuations remain broadly in line with long‑term averages and well below pre‑2018 levels, signaling further upside potential.

Snaking immigration queues and bustling crowds in hotels, malls and restaurants, in part drawn to the Blackpink concert, greeted us on our recent visit to Hong Kong. The renewed vibrancy was reminiscent of the pre-pandemic Hong Kong, which has been sorely missed. At the heart of this reversal in sentiment is property, particularly the residential sector, where momentum is visibly building.

What is driving the current rebound in Hong Kong residential?

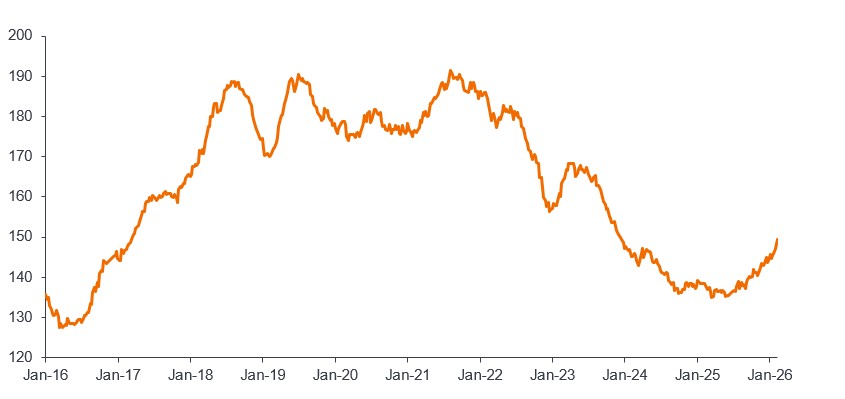

The wealth effect has certainly been a key catalyst for the renewed interest in property. Strong Hong Kong equity gains, particularly from the booming initial public offering (IPO) market, are flowing through to the real estate market. Talent schemes, like the Top Talent Pass Scheme (offering visas to high-income earners and graduates from top-ranked universities across the world to work or set up businesses) have brought in new residents who have driven rentals to record highs in many locations. Meanwhile, rate cuts have pushed mortgage rates lower, making buying more attractive than renting given positive carry (higher rental yield compared to mortgage rate). Coupled with supportive policy measures and declining inventory and supply, the residential market has seen a rebound with secondary market property prices now up around 10% from the bottom in Q2 2025 (Figure 1).

Figure 1: Hong Kong secondary residential market is in recovery

Centaline Property Centa-City Leading Index

Source: Bloomberg, Janus Henderson Investors. Centaline Property Centa-City Leading Index (CENLCCL), 2 February 2016 to 8 February 2026. The weekly updated Centa-City Leading Index measures the secondary private residential property prices in Hong Kong. Past performance does not predict future returns.

Early recovery mode – our visit to Wong Chuk Hang

Wong Chuk Hang was historically an industrial area on Hong Kong island but with the opening of the Mass Transit Railway (MTR) South Island Line in 2016, it has undergone significant development. Six land parcels were tendered out to major developers between 2017 to 2021, adding nearly 5,000 residential units. Proximity to the city and several international schools in the vicinity makes Wong Chuk Hang a prime location. The first launch in May 2021 coincided with the peak in the residential market. When wider market prices fell about 30% from the peak, many developers held back on their launches.

We visited La Montagne, phase four of the development, which is jointly managed by three of Hong Kong’s leading developers – Sino Land, Kerry Properties and Swire Properties. The first phase of units was launched in July 2023 when we saw a slight rebound in the market at around HK$28,000 per square foot (psf), but sales paused when the market took another leg down. Testing the market again in early 2025 upon completion of the project, by offering prices cuts of around 20% was met with lukewarm response. But this changed in mid-2025 when interest and momentum began to accelerate. While there has not been another official new launch since, units have continued to sell via tender and prices have been steadily climbing. Today, an 800 square foot three-bedroom unit with views of Brick Hill (the location of theme park Ocean Park) and the surrounding bays has a sales tag of circa HK$30 million.

View from a luxury unit at the La Montagne development. Image credit: Global Property Equities Team.

More room for Hong Kong residential stocks to re-rate?

Mid-2025 marked the bottom of the Hong Kong residential market. While other commercial sectors have not seen the same magnitude of recovery, activity has picked up – transactions are increasing, leasing momentum is improving, while selective pockets of positive rental growth are emerging. Hong Kong property stocks were one of the best performers globally over the last 12 months as renewed interest has driven a significant multiple re-rating.

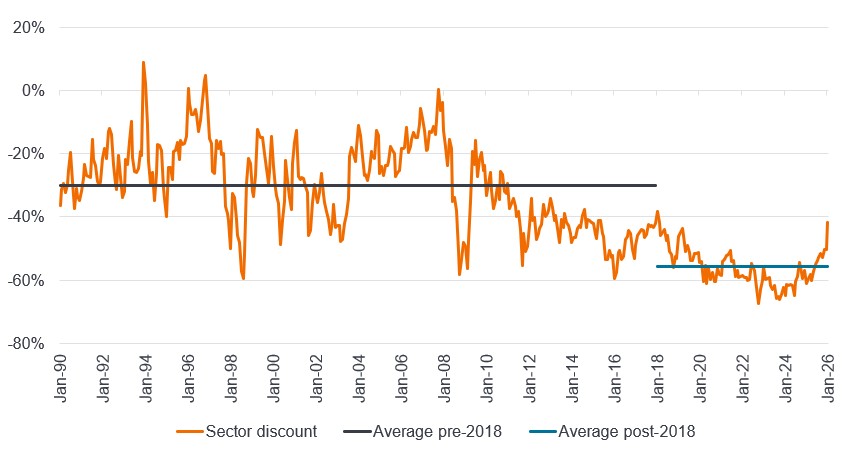

We remain constructive on the sector, so long as key drivers to stronger fundamentals remain on track. Hong Kong developers are now trading at 40% discount to NAV (Net Asset Value) versus the troughs of 70% discount to NAV and may look expensive particularly against historical levels since 2018. However, whilst some developers’ stock prices have doubled since the lows in April 2025, they are still flat versus 2018, reflecting Hong Kong’s lost decade. It has been an exceptionally difficult period with the significant de-rating a reflection of multiple blows dealt to the city from the 2018 protests to the pandemic, China’s zero-COVID policies and the rapid rate hike cycle in 2022. As property prices and rentals rebound, developers are more likely to regain bargaining power, supporting higher profitability. Growth in earnings and asset values will in turn drive the next leg of share price performance.

Figure 2: Hong Kong developers discount to Net Asset Value (NAV)

Source: Bank of America Merrill Lynch, Janus Henderson Investors. 31 January 1990 to 31 January 2026. Past performance does not predict future returns.

Real estate is at the very core of the economy; as Hong Kong works to regain its formal glory, we believe the property sector stands to be a key beneficiary.

Balance sheet: An indicator of financial strength; in the context of a company, it is a financial statement that summarises a company’s assets, liabilities, and shareholders’ equity at a particular point in time. Each segment gives investors an idea as to what the company owns and owes, as well as the amount invested by shareholders

Discount to NAV: Net asset value (NAV). measures the underlying value of the REIT’s holdings by taking the market value and subtracting any debts, such as mortgage liabilities. When an investment’s market price is higher than its NAV, it is said to be trading at a premium. Conversely, when an investment’s market price is lower than its NAV, it is said to be trading at a discount.

Multiple de-rating: Multiples are financial tools used to assess a company’s valuation by helping to compare companies’ valuations within the same industry. In the case of equities, a de-rating refers to the downward adjustment of a company’s multiples (financial ratios), such as the price-to-earnings (P/E) ratio, in response to business or market uncertainty. A re-rating occurs when investors are willing to pay a higher price for shares, usually in anticipation of higher future earnings.

These are the views of the author at the time of publication and may differ from the views of other individuals/teams at Janus Henderson Investors. References made to individual securities do not constitute a recommendation to buy, sell or hold any security, investment strategy or market sector, and should not be assumed to be profitable. Janus Henderson Investors, its affiliated advisor, or its employees, may have a position in the securities mentioned.

Past performance does not predict future returns. The value of an investment and the income from it can fall as well as rise and you may not get back the amount originally invested.

The information in this article does not qualify as an investment recommendation.

There is no guarantee that past trends will continue, or forecasts will be realised.

Marketing Communication.