Key takeaways:

- Europe’s economy is stabilising, as stronger data, fiscal and monetary support, easing tariff risks, and potential Ukraine peace underpin recovery.

- Economic stabilisation is driving revenue growth, supporting organic deleveraging and stronger free cash flow. Credit fundamentals are therefore improving.

- European loans offer attractive yields and can exhibit lower default risk versus high yield (HY). Disciplined security selection and a focus on fundamentals, in our view, can enhance returns.

Stabilisation and support in Europe

The Eurozone is holding its ground: GDP grew by +0.1% in Q2 2025, extending year-on-year gains of 1.4%. Composite PMI readings are hovering near 50, signalling stabilisation across sectors and a platform for renewed momentum.

Monetary policy remains supportive. The European Central Bank (ECB) has delivered eight consecutive rate cuts totalling 200 bps since mid-2024, bringing the deposit rate to 2% before pausing in July. Inflation is now aligned with the ECB’s 2% target, and ECB President Lagarde insists Europe is in a “good place”. On the fiscal side, anticipated fiscal stimulus in Germany could deliver a powerful boost, given its weight as the region’s largest economy. These developments have helped stabilise corporate revenues and cash flows, laying a stronger foundation for growth.

Trump tariff uncertainty abated

Trade uncertainty has eased after the US–EU trade deal capped tariffs at 15% on key sectors such as autos, pharmaceuticals, and semiconductors – well below the 100%+ levels once threatened. This clarity gives businesses confidence to plan and invest, strengthening Europe’s recovery prospects.

Potential upside from peace in Ukraine

While the conflict in Ukraine persists, peace would unlock significant upside through reconstruction and trade, reopening markets for goods and services and lifting investor confidence. According to BNP Paribas, a ceasefire could boost European GDP by 0.9–1.5%[1]. Though timing remains uncertain, this represents meaningful upside for the European economy.

Relative value exists in European fixed income

The challenge for fixed income investors is uncovering relative value in an environment where credit spreads are trading in the tightest percentiles. Uncertainty remains with risks from across the Atlantic and Europe itself, such as the instability in the French government. Tight spreads are more susceptible to widening in the event of any shock or development that rattles market sentiment. So capturing better relative value feels prudent to provide a buffer against any potential volatility-driven spread widening.

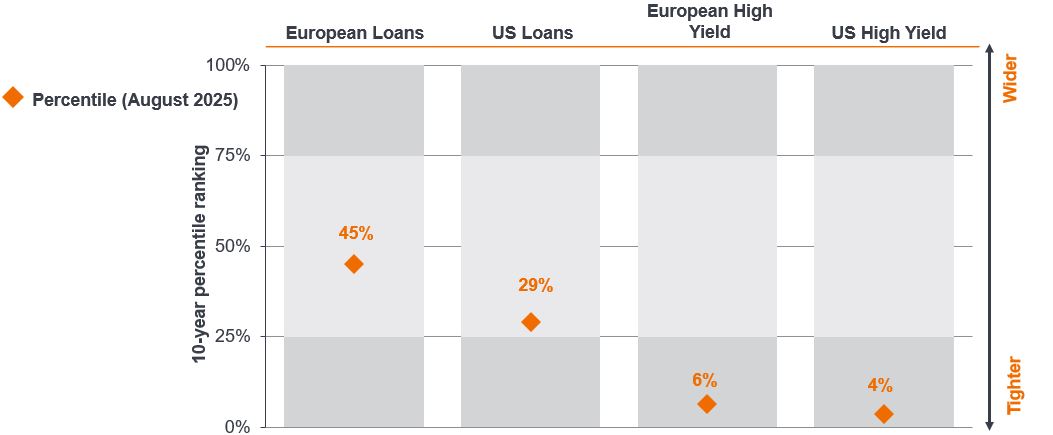

Figure 1: Relative value stands out in loans as shown by percentiles

Source: Bloomberg, Janus Henderson Investors, as at 26 August 2025. European loans: The JP Morgan European Leveraged Loan Index; US loans: The JP Morgan Leveraged Loan Index; European High Yield: Bloomberg European High Yield Index; US High Yield: Bloomberg US High Yield Index.

Comparing percentiles for European high yield (HY), US HY, US loans, and European loans, European loans appear to be the cheapest (Figure 1). This suggests a more attractive entry point for investors, as do absolute spread or discount margin (DM)[2] levels. Spreads of US HY and European HY alongside the 3-year DMs of US and European Loans further evidence that European loans currently offer the best compensation for credit risk in the leveraged finance space (Figure 2).

Figure 2: Absolute spread levels are also attractive in loans

| Metric | European Loans | US Loans | European High Yield | US High Yield |

| Current spread | 485 | 435 | 275 | 279 |

Source: Bloomberg, Janus Henderson Investors, as at 26 August 2025. European loans: The JP Morgan European Leveraged Loan Index; US loans: The JP Morgan Leveraged Loan Index; European High Yield: Bloomberg European High Yield Index; US High Yield: Bloomberg US High Yield Index.

Selectiveness amid optimism

The European economy has stabilised, supported by fiscal loosening and easier monetary policy. Germany’s €500 billion infrastructure fund, defence push and the EU’s broader Readiness programme, which aims to boost European defence spending by over €800 billion, mark a decisive shift that Citi estimates could add 0.4% to GDP in 2027, with 0.2% to be added in 2025–2026[3]. Meanwhile, as explained earlier, the ECB has paused cutting rates, with inflation around target – creating a more benign funding backdrop.

For investors, European loans stand out. Spreads tightened after the April (President Trump’s ‘Liberation Day’) wobble but continue to screen attractive versus HY. Over the past 12 months, loans have had a lower default rate than HY and we believe defaults in loans will remain contained in general in the proceeding months. EU loan default rate is calculated at 1.9%[4] versus ~3.9% for European speculative grade or HY bonds[5]. This combination keeps European loans compelling for risk-adjusted returns with a measure of downside protection, as most leveraged loans are secured by the borrower’s assets.

Security selection remains paramount

Under the surface, quality is being rewarded. Performing, low‑beta loans (>80% of the market) are holding near par (average price ~100.03)[6], signalling confidence in Europe’s stabilisation. But leverage is still elevated (median first lien Net Debt/EBITDA 4.5-5.5x)[7], and highly levered pockets – particularly petrochemicals and labs/diagnostics – have lagged through thin summer liquidity. As the primary market reopens in September, we expect dispersion to stay high, hence security selection and sector resilience remain key.

IMPORTANT INFORMATION

Fixed income securities are subject to interest rate, inflation, credit and default risk. The bond market is volatile. As interest rates rise, bond prices usually fall, and vice versa. The return of principal is not guaranteed, and prices may decline if an issuer fails to make timely payments or its credit strength weakens.

Bank loans often involve borrowers with low credit ratings whose financial conditions are troubled or uncertain, including companies that are highly leveraged or in bankruptcy proceedings.

[1] Source: BNP Paribas estimates, as at 24 February 2025.

[2] Discount margin (DM) represents the average expected return of a floating rate security over and above the reference rate (such as LIBOR, EURIBOR, or any other benchmark rate) throughout the life of the instrument. It is comparable to credit spreads on other fixed income instruments, such as corporate credit.

[3] Source: Citi estimates, as at 18 July 2025.

[4] Source: UBS, July 2025. Default rate calculated over a 12-month period.

[5] Source: S&P, June 2025. Default rate calculated over a 12-month period.

[6] Source: Bloomberg, custom Credit Suisse Western European Leveraged Loan Index (CS WELLI), as at 26 August 2025.

[7] Source: Janus Henderson estimates, as at 26 August 2025.

Low beta loans: In the context of “low beta loans,” this would refer to loans that are less sensitive to broader market movements. These loans would typically exhibit smaller fluctuations in their value in response to market changes, making them potentially less risky compared to high beta loans.

Net Debt/EBITDA: The ratio of net debt to EBITDA (Earnings Before Interest, Taxes, Depreciation, and Amortization) is a financial metric used to measure a company’s ability to pay off its debt. It provides insight into how many years it would take for a company to pay back its debt if net debt and EBITDA are held constant.

First lien: In the context of a loan, “first lien” refers to the legal right granted to a lender to be the first to claim repayment from the assets of a borrower in the event of default, before any other creditors are paid.

Free cash flow: This is a financial metric that represents the amount of cash a company generates after accounting for cash outflows to support operations and maintain its capital assets. It is an important indicator of a company’s financial health and its ability to generate cash that can be used for expansion, stock dividends, debt repayment, and other purposes.

These are the views of the author at the time of publication and may differ from the views of other individuals/teams at Janus Henderson Investors. References made to individual securities do not constitute a recommendation to buy, sell or hold any security, investment strategy or market sector, and should not be assumed to be profitable. Janus Henderson Investors, its affiliated advisor, or its employees, may have a position in the securities mentioned.

Past performance does not predict future returns. The value of an investment and the income from it can fall as well as rise and you may not get back the amount originally invested.

The information in this article does not qualify as an investment recommendation.

There is no guarantee that past trends will continue, or forecasts will be realised.

Marketing Communication.