Income opportunity amid the rates volatility

James Briggs, fixed income portfolio manager, considers the recent volatility in rates expectations and why now may be a good time to lock in short-dated bond yields before they potentially fall.

5 minute read

Key takeaways:

- Volatility in interest rate expectations has caused a near-term spike in bond yields as markets have been focused on economic data in the US.

- Several central banks have already started to cut interest rates, however, including the central banks of Switzerland and Sweden and there are growing expectations that the European Central Bank will cut soon.

- Short-dated investment grade corporate bonds are currently offering yields that are not only high historically but are also materially above current inflation.

“Prediction is difficult, especially about the future,” a quote often ascribed to Neils Bohr, the Nobel prize-winning physicist, but can equally be applied to financial markets. Recent weeks have seen market participants rapidly re-adjusting their forecasts for interest rates.

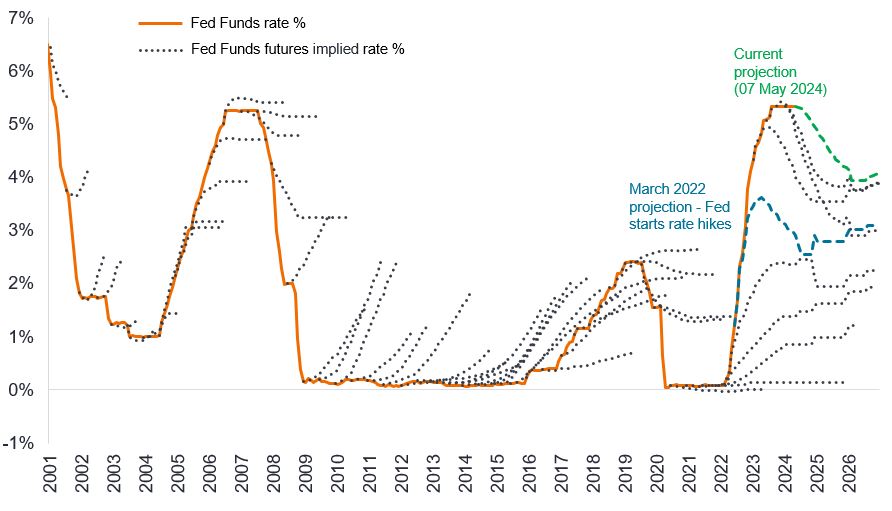

The truth is that the market has a patchy record when it comes to forecasting as Figure 1 shows. The dotted lines reflect the futures market’s expectation of where the US Federal Reserve’s (Fed) funds rate would be. Invariably, the market over- or under-estimates the actual moves in the Fed’s policy rate.

Figure 1: Market expectations versus actual interest rate direction

Source: Bloomberg, Federal Funds rate, Fed funds futures 30 day rates, six month intervals, 2001 to 2024. There is no guarantee that past trends will continue, or forecasts will be realised. Past performance does not predict future returns.

Rates divergence

Furthermore, amid all the focus on the Fed, it is easy to miss what is happening elsewhere. The Swiss National Bank, with its cut in March, fired the starting gun on cutting interest rates in developed markets. In early May, Sweden’s Riksbank followed with its first rate cut of the cycle. Meanwhile many emerging markets have been reducing rates since late last year. Even the notion that the European Central Bank (ECB) has historically followed the Fed is not strictly true. In 2011, the ECB raised rates, although this was an episode it may prefer to forget as it rapidly unwound the short-lived tightening in response to fresh economic weakness.

Fast forward to today and we should probably expect a decoupling in policy between the ECB and the Fed, not least because a relatively weaker Eurozone economy and firmer progress on reducing inflation offers a clearer path for the ECB to begin cutting rates before the Fed.

It was always likely that Europe’s economy would respond more forcefully to the rate hikes that have taken place over the past couple of years. This is because European companies operate with shorter-term debt that needs refinancing more regularly and on average have more floating-rate debt. In addition, European households typically have mortgages on shorter fixed-rate periods than in the US, creating a more rapid transmission effect for monetary policy.

Fundamental attractions

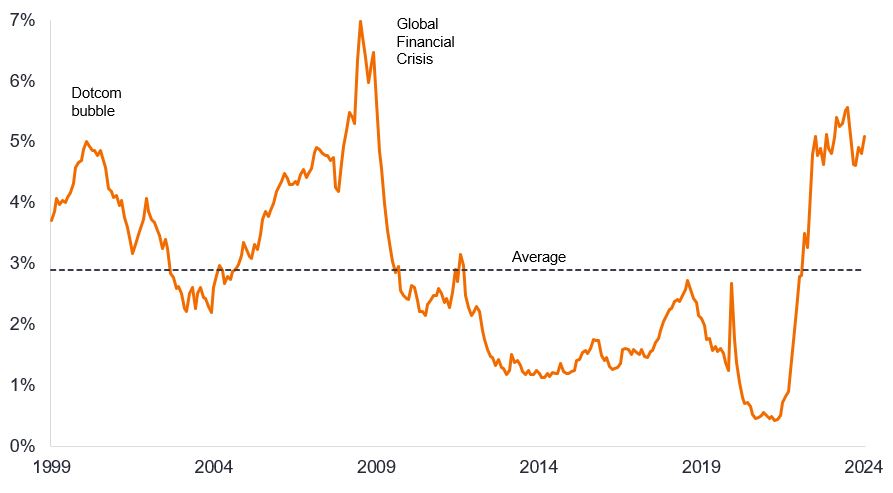

Second guessing the timing of central banks’ moves can, however, become a distraction to the fundamental attractiveness of assets. The irony is that the rates uncertainty has created an opportunity. Yields on short-term investment grade corporate bonds are hovering around their most attractive levels in more than a decade. In fact, yields are at levels which – since the turn of the millennium – would be more typically associated with crises (Figure 2).

Figure 2: Yield on global short-dated investment grade corporate bonds

Source: Bloomberg, ICE BofA 1-3 year Global Corporate Index, yield to worst, 30 April 1999 to 30 April 2024. Yields may vary over time and are not guaranteed. Past performance does not predict future returns.

What is particularly powerful today is the level of real yield (yield adjusted for inflation) that an investor can achieve from short-dated corporate bonds. In Europe, short-dated investment grade corporate bonds are currently yielding more than 1.6% above the rate of Eurozone inflation. This compares with a real yield that was typically negative over the past decade (Figure 3).

Figure 3: Real yields are well above the historical average

Source: Bloomberg, ICE BofA 1-3 year Euro Corporate Index, yield to worst, CPI shown is Euro Area Consumer Price Index (MUICP), year-on-year (yoy) percentage change, 30 April 2014 to 30 April 2024. IG = Investment Grade. There is no guarantee that past trends will continue, or forecasts will be realised. Yields may vary over time and are not guaranteed. Past performance does not predict future returns.

We cannot say for certain that the ECB will embark on rate cuts in June. What we do know, however, is that today an investor in short-dated corporate bonds can achieve a level of yield that is not only relatively high historically, but is also offering a yield that provides ample compensation for current inflation.

The message from the most recent Fed policy meeting on 1 May was that even in their “wait and see” data-dependent mode, the bar to a rate hike is high. The subsequent weaker-than-expected non-farm US payrolls data covering the month of April was in keeping with recent softening in US purchasing manager survey data, hinting that the strength in US economic data in the previous six months may be waning. Meanwhile, comments from members of the ECB governing council lean towards rate cuts coming closer. In our view, this creates an asymmetric opportunity: limited risk that rates move higher, but the prospect that shorter-dated bond yields could respond (decline) quickly to any weakness in the economic data and/or confirmation that rate cuts are commencing.

As a result, we believe that investors sitting in cash should be alert to the fact that rates on cash are likely to head lower in the coming months. In our view, short-dated investment grade corporate bonds offer an opportunity to lock in attractive yields without taking on excessive duration or credit risk.

ICE BofA 1-3 year Euro Corporate Index tracks EUR denominated investment grade corporate debt publicly issued in the eurobond or Euro member domestic markets, with a remaining term to final maturity less than 3 years

ICE BofA 1-3 year Global Corporate Index tracks investment grade corporate debt publicly issued in the major domestic and eurobond markets, with a remaining term to final maturity less than 3 years.

Credit risk: The risk that a borrower will default on its contractual obligations to investors, by failing to make the required debt payments. Anything that improves conditions for a company can help to lower credit risk.

Corporate bonds: A debt security issued by a company. Bonds offer a return to investors in the form of periodic payments and the eventual return of the original money invested at issue on the maturity date.

Default: The failure of a debtor (such as a bond issuer) to pay interest or to return an original amount loaned when due.

Duration: The sensitivity of a bond’s price to a change in interest rates.

Floating rate debt: Debt that is on a variable interest rate.

High yield: A bond that has a lower credit rating than an investment grade bond. Sometimes known as a sub-investment grade bond. These bonds carry a higher risk of the issuer defaulting on their payments, so they are typically issued with a higher coupon to compensate for the additional risk.

Inflation: The rate at which prices of goods and services are rising in the economy.

Interest rate future: A contract that allows buyers and sellers to lock in rates on an interest-bearing asset.

Investment grade: A bond typically issued by governments or companies perceived to have a relatively low risk of defaulting on their payments. The higher quality of these bonds is reflected in their higher credit ratings.

Maturity: The maturity date of a bond is the date when the principal investment (and any final coupon) is paid to investors. Shorter-dated bonds generally mature within 5 years, medium-term bonds within 5 to 10 years, and longer-dated bonds after 10+ years.

Volatility: The rate and extent at which the price of a portfolio, security or index, moves up and down. If the price swings up and down with large movements, it has high volatility. If the price moves more slowly and to a lesser extent, it has lower volatility. The higher the volatility the higher the risk of the investment.

Yield: The level of income on a security, typically expressed as a percentage rate. For a bond, at its most simple, this is calculated as the annual coupon payment divided by the current bond price.

Yield to worst: The lowest yield a bond with a special feature (such as a call option) can achieve provided the issuer does not default. When used to describe a portfolio, this statistic represents the weighted average across all the underlying bonds held.

IMPORTANT INFORMATION

Fixed income securities are subject to interest rate, inflation, credit and default risk. The bond market is volatile. As interest rates rise, bond prices usually fall, and vice versa. The return of principal is not guaranteed, and prices may decline if an issuer fails to make timely payments or its credit strength weakens.

High-yield or “junk” bonds involve a greater risk of default and price volatility and can experience sudden and sharp price swings.

These are the views of the author at the time of publication and may differ from the views of other individuals/teams at Janus Henderson Investors. References made to individual securities do not constitute a recommendation to buy, sell or hold any security, investment strategy or market sector, and should not be assumed to be profitable. Janus Henderson Investors, its affiliated advisor, or its employees, may have a position in the securities mentioned.

Past performance does not predict future returns. The value of an investment and the income from it can fall as well as rise and you may not get back the amount originally invested.

The information in this article does not qualify as an investment recommendation.

Marketing Communication.

Important information

Please read the following important information regarding funds related to this article.

- An issuer of a bond (or money market instrument) may become unable or unwilling to pay interest or repay capital to the Fund. If this happens or the market perceives this may happen, the value of the bond will fall.

- When interest rates rise (or fall), the prices of different securities will be affected differently. In particular, bond values generally fall when interest rates rise (or are expected to rise). This risk is typically greater the longer the maturity of a bond investment.

- The Fund invests in high yield (non-investment grade) bonds and while these generally offer higher rates of interest than investment grade bonds, they are more speculative and more sensitive to adverse changes in market conditions.

- Some bonds (callable bonds) allow their issuers the right to repay capital early or to extend the maturity. Issuers may exercise these rights when favourable to them and as a result the value of the Fund may be impacted.

- The Fund may use derivatives to help achieve its investment objective. This can result in leverage (higher levels of debt), which can magnify an investment outcome. Gains or losses to the Fund may therefore be greater than the cost of the derivative. Derivatives also introduce other risks, in particular, that a derivative counterparty may not meet its contractual obligations.

- If the Fund holds assets in currencies other than the base currency of the Fund, or you invest in a share/unit class of a different currency to the Fund (unless hedged, i.e. mitigated by taking an offsetting position in a related security), the value of your investment may be impacted by changes in exchange rates.

- When the Fund, or a share/unit class, seeks to mitigate exchange rate movements of a currency relative to the base currency (hedge), the hedging strategy itself may positively or negatively impact the value of the Fund due to differences in short-term interest rates between the currencies.

- Securities within the Fund could become hard to value or to sell at a desired time and price, especially in extreme market conditions when asset prices may be falling, increasing the risk of investment losses.

- Some or all of the ongoing charges may be taken from capital, which may erode capital or reduce potential for capital growth.

- In addition to income, this share class may distribute realised and unrealised capital gains and original capital invested. Fees, charges and expenses are also deducted from capital. Both factors may result in capital erosion and reduced potential for capital growth. Investors should also note that distributions of this nature may be treated (and taxable) as income depending on local tax legislation.

Specific risks

5 minute read

Key takeaways:

- Volatility in interest rate expectations has caused a near-term spike in bond yields as markets have been focused on economic data in the US.

- Several central banks have already started to cut interest rates, however, including the central banks of Switzerland and Sweden and there are growing expectations that the European Central Bank will cut soon.

- Short-dated investment grade corporate bonds are currently offering yields that are not only high historically but are also materially above current inflation.