Key takeaways:

- Recent volatility in AI-related equities has sparked further debate on the technology’s long-term prospects. To gain perspective, we believe investors need to understand the magnitude of the transformation and how it will invariably impact revenue growth and productivity in every corporate sector.

- With the bullishness around AI comes historic CapEx budgets. As hyperscalers aggressively tap debt capital markets, companies across the fixed income spectrum stand to benefit as spending flows through the AI data center supply chain.

- Technological shifts of this magnitude are a fertile environment for active management. In our view, selectivity will be critical to identifying the next wave of winners and capitalizing on the broad spectrum of opportunities that arise as the AI transformation continues in the years ahead.

Over the past 50 years, technology has been dominated by mega-themes, from the dawn of the commercial Internet to the rise of cloud computing, mobile, machine learning, and now artificial intelligence (AI). With any theme of this magnitude, the question inevitably arises of whether it is over- or under-hyped – and in turn, whether the valuations of companies tied to those themes are justified.

Recent volatility in AI-related equities only sharpens this line of enquiry. To gain perspective, we believe investors need to understand the magnitude of the transformation underway and how it will invariably touch every corporate sector, impacting revenue growth, productivity and, in many cases, sending many business models toward obsolescence.

Furthermore, the shadow of AI is no longer just a question for equities investors, as typically conservatively funded mega-cap tech companies are tapping debt capital markets at record levels.

Perhaps the most important thing to consider when weighing valuations for today’s mega-cap tech stocks is that it’s still early days in the AI investment cycle. The technological shifts that have made AI possible occurred over a period of 25 or 30 years, and it’s hard to overstate how important those advancements were in laying the groundwork for the progress we’ve seen in the past three years.

Dispelling the myths of an AI bubble

There are a couple key areas about AI investing that we believe are underappreciated and that serve to dispel many of the concerns around an AI bubble. First, it’s important to understand that the reason AI has been the main driver for the market is because investors are recognizing how profound this technology shift is – not only in terms of the sheer revenue opportunity created by the winners but also the meaningful productivity and margin lift we expect to see globally as AI proliferates into the broader economy.

Second, the focus tends to be on the digital manifestation of AI, which will clearly have a significant impact on many sectors. But we think the physical manifestation of AI will be equally profound. We’re seeing meaningful progress in areas like full-service and autonomous driving, robotics, and other areas that will impact the physical economy.

The tech stocks of the early 2000s looked expensive at the time but ultimately grew earnings much faster than anyone anticipated. We anticipate the same with AI: We fully expect there will be companies that compound earnings and free cash flow materially faster than investors expect. And as the AI buildout cascades from infrastructure companies (enablers) to well-positioned software providers (enhancers), and ultimately into the broader economy, that is the point where forward-looking companies (end users) could reap significant economic benefits.

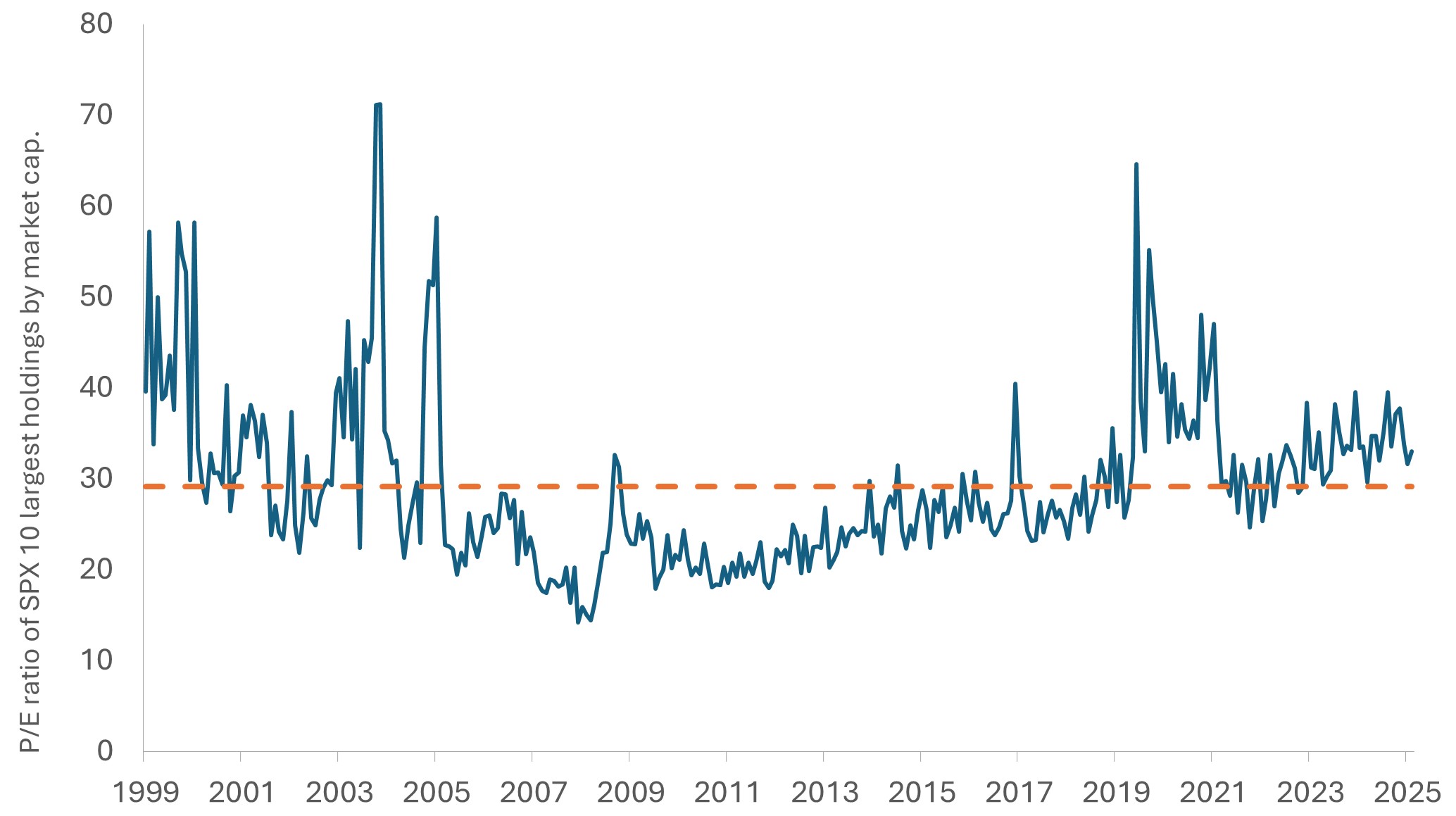

Exhibit 1: Price/earnings ratio of S&P 500’s top decile by market capitalization

At roughly 33 based on expected 2026 earnings, the P/E ratio of the S&P 500’s 10 largest stocks sits well below the frothy levels experienced during the dotcom era – and these megacaps are generating substantial cash off their deployed AI platforms.

Source: Bloomberg, as of 6 February 2026.

Funding the AI boom

With the bullishness around AI comes historic CapEx budgets. Accordingly, many AI hyperscalers have deviated from their script and have aggressively tapped debt capital markets, increasing leverage in the process. This shift has made the AI investment theme just as much of a fixed income play as an equities play.

New issuance varies widely across subsectors. Hyperscalers are tapping into the investment-grade (IG) credit markets for AI financing. This could put pressure on currently tight spreads in IG as that debt is absorbed. The high-yield market appears better positioned, as direct AI debt issuance is less than 1.0% of the Bloomberg US Corporate High Yield Index at present.

Additionally, we think there is significant room for growth in AI-related issuance in securitized credit. For one, commercial mortgage-backed securities (CMBS) are a major focus given the funding required to build new data centers.

Within CMBS, geography is a key consideration: A large percentage of data centers are concentrated in specific areas, so it’s important to ensure the real estate backing the deal is in one of the geographical “nodes” that are known for data center buildouts and have sufficient access to the power grid. While there are concerns around data center development given the burden they place on the grid, the market appears to be pricing in that risk, and we are seeing attractive CMBS spreads at relatively short maturities. Furthermore, shorter time horizons associated with projects funded by CMBS, in our view, should provide greater visibility in issuers’ ability to meet their obligations.

On that front, CapEx trends show data center growth is here for the foreseeable future. To put the power demand of AI chips and application in perspective, some estimates suggest that three New York City’s worth of power will be needed to sustain the grid by 2030.

As some of the AI hyperscalers want to own data centers, we may also see more private deals. But ultimately, companies will be seeking the lowest cost of capital and looking to diversify the channels through which capital is obtained. We expect the massive CapEx programs of investment-grade hyperscalers to benefit companies across the entire fixed income spectrum as spending flows through the AI data center supply chain.

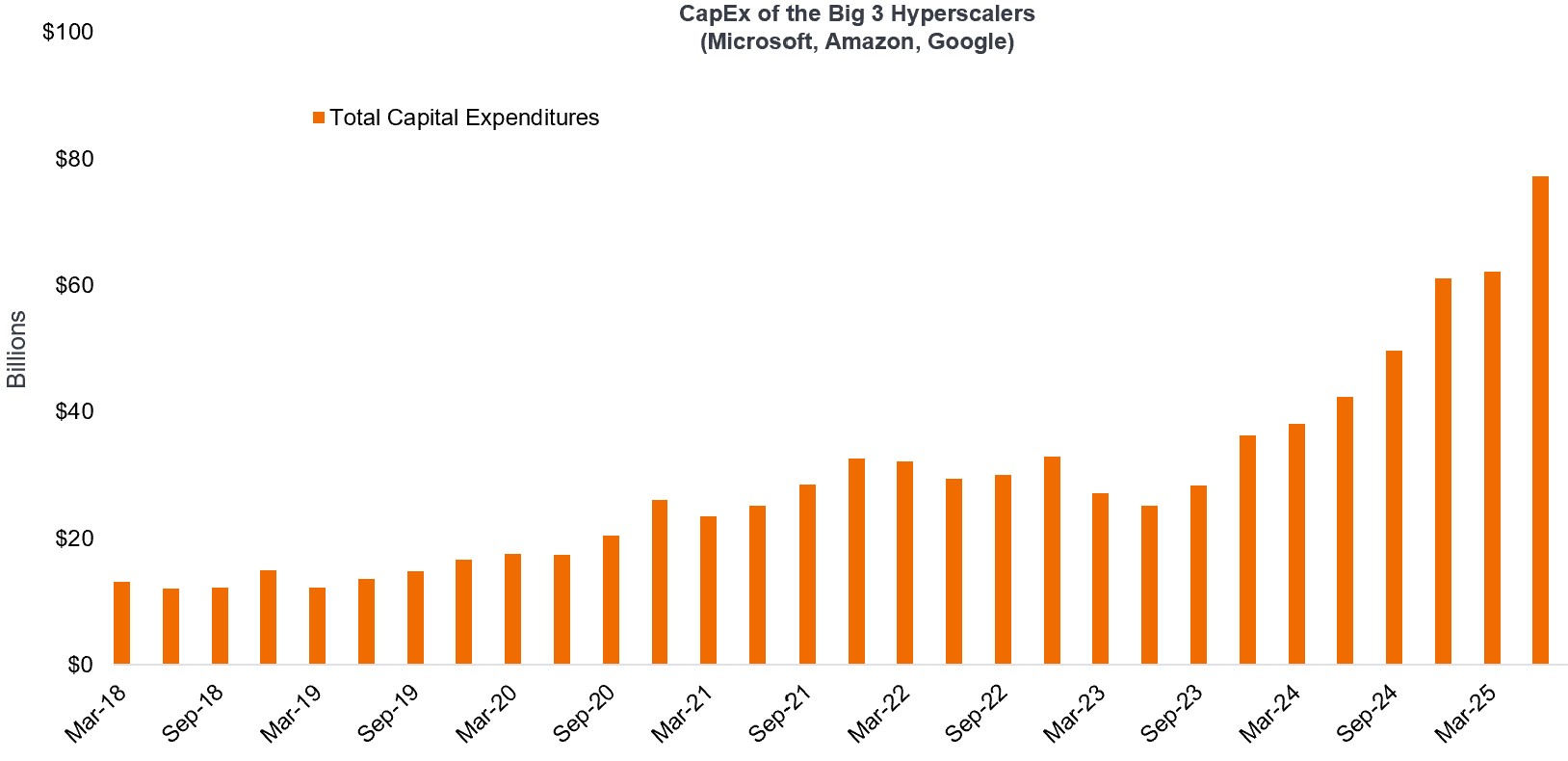

CapEx of the big three hyperscalers (Microsoft, Amazon, Google)

Capex trends suggest data center growth is here to stay.

Source: Dell’Oro, JP Morgan estimates. CSP capex by: Microsoft, Google, Amazon.

Utility companies are also issuing debt for the AI buildout as power demand continues to create a bottleneck. We view this as a compelling opportunity, because traditionally low-growth utilities businesses are turning into high-growth businesses as power demand from AI continues to increase.

From rising tides to the imperative of selectivity

From both an equity and debt perspective, one of the biggest concerns around AI is obsolescence, especially since it has advanced so quickly. Remember, we are only a few years removed from the launch of ChatGPT, and today the AI agent is being used daily across the globe.

While AI applications like ChatGPT may feel like they became ubiquitous overnight, recall that laying the foundation to make these technologies possible took decades. Likewise, the work of continuing to build out the AI training infrastructure will be ongoing for many years. And the time horizon for end users to not only implement but reap benefits from AI is longer still. Meanwhile, the inference stage of this technology is on the verge of exploding given the move to an agentic world.

Importantly, the rising tide will not lift all boats forever. If we look across the spectrum, there are AI infrastructure companies that are clear winners and continue to separate themselves; these stocks, based on our projected cash flows, are not expensive when one considers they are leading the technology transformation. Likewise, there are companies in the enhancer space that have developed competencies over many years and that are navigating the AI infrastructure more efficiently than their competitors.

At the same time, many areas will face significant disruption. For example, we recently wrote about the (understandable) investor angst around the future of software as a service (SaaS) companies, noting that the next generation of software winners will likely be those that embrace AI not as a feature but as the foundation of their operating models.It’s also worth noting that some tech stocks are trading at 50 times revenues due largely to the “AI halo” effect, even though they have limited revenues or products and services that may not even be deployed until 2030.

As we’ve said many times before, AI disruption will not be linear. While the direction of travel over the next decade is clear, what happens over a year or two is not. Technological shifts of this magnitude are a fertile environment for active management. In our view, selectivity will be critical to identifying the next wave of winners and capitalizing on the broad spectrum of opportunities that arise as the AI transformation continues in the years ahead.

IMPORTANT INFORMATION

Actively managed portfolios may fail to produce the intended results. No investment strategy can ensure a profit or eliminate the risk of loss.

Artificial intelligence (“AI”) focused companies, including those that develop or utilize AI technologies, may face rapid product obsolescence, intense competition, and increased regulatory scrutiny. These companies often rely heavily on intellectual property, invest significantly in research and development, and depend on maintaining and growing consumer demand. Their securities may be more volatile than those of companies offering more established technologies and may be affected by risks tied to the use of AI in business operations, including legal liability or reputational harm.

Fixed income securities are subject to interest rate, inflation, credit and default risk. The bond market is volatile. As interest rates rise, bond prices usually fall, and vice versa. The return of principal is not guaranteed, and prices may decline if an issuer fails to make timely payments or its credit strength weakens.

Securitized products, such as mortgage-backed securities and asset-backed securities, are more sensitive to interest rate changes, have extension and prepayment risk, and are subject to more credit, valuation and liquidity risk than other fixed-income securities.

Technology industries can be significantly affected by obsolescence of existing technology, short product cycles, falling prices and profits, competition from new market entrants, and general economic conditions. A concentrated investment in a single industry could be more volatile than the performance of less concentrated investments and the market as a whole.

The Bloomberg US Corporate High Yield Bond Index measures the USD-denominated, high yield, fixed-rate corporate bond market.

Investment-grade securities: A security typically issued by governments or companies perceived to have a relatively low risk of defaulting on their payments. The higher quality of these bonds is reflected in their higher credit ratings when compared with bonds thought to have a higher risk of default, such as high-yield bonds.

Queste sono le opinioni dell'autore al momento della pubblicazione e possono differire da quelle di altri individui/team di Janus Henderson Investors. I riferimenti a singoli titoli non costituiscono una raccomandazione all'acquisto, alla vendita o alla detenzione di un titolo, di una strategia d'investimento o di un settore di mercato e non devono essere considerati redditizi. Janus Henderson Investors, le sue affiliate o i suoi dipendenti possono avere un’esposizione nei titoli citati.

Le performance passate non sono indicative dei rendimenti futuri. Tutti i dati dei rendimenti includono sia il reddito che le plusvalenze o le eventuali perdite ma sono al lordo dei costi delle commissioni dovuti al momento dell'emissione.

Le informazioni contenute in questo articolo non devono essere intese come una guida all'investimento.

Non vi è alcuna garanzia che le tendenze passate continuino o che le previsioni si realizzino.

Comunicazione di Marketing.

Important information

Please read the following important information regarding funds related to this article.

- Gli emittenti di obbligazioni (o di strumenti del mercato monetario) potrebbero non essere più in grado di pagare gli interessi o rimborsare il capitale, ovvero potrebbero non intendere più farlo. In tal caso, o qualora il mercato ritenga che ciò sia possibile, il valore dell'obbligazione scenderebbe.

- L’aumento (o la diminuzione) dei tassi d’interesse può influire in modo diverso su titoli diversi. Nello specifico, i valori delle obbligazioni si riducono di norma con l'aumentare dei tassi d'interesse. Questo rischio risulta di norma più significativo quando la scadenza di un investimento obbligazionario è a più lungo termine.

- Il Fondo investe in obbligazioni ad alto rendimento (non investment grade) che, sebbene offrano di norma un interesse superiore a quelle investment grade, sono più speculative e più sensibili a variazioni sfavorevoli delle condizioni di mercato.

- Alcune obbligazioni (obbligazioni callable) consentono ai loro emittenti il diritto di rimborsare anticipatamente il capitale o di estendere la scadenza. Gli emittenti possono esercitare tali diritti laddove li ritengano vantaggiosi e, di conseguenza, il valore del Fondo può esserne influenzato.

- Un Fondo che presenta un’esposizione elevata a un determinato paese o regione geografica comporta un livello maggiore di rischio rispetto a un Fondo più diversificato.

- Il Fondo potrebbe usare derivati al fine di conseguire il suo obiettivo d'investimento. Ciò potrebbe determinare una "leva", che potrebbe amplificare i risultati dell'investimento, e le perdite o i guadagni per il Fondo potrebbero superare il costo del derivato. I derivati comportano rischi aggiuntivi, in particolare il rischio che la controparte del derivato non adempia ai suoi obblighi contrattuali.

- Se il Fondo, o una sua classe di azioni con copertura, intende attenuare le fluttuazioni del tasso di cambio tra una valuta e la valuta di base, la stessa strategia di copertura potrebbe generare un effetto positivo o negativo sul valore del Fondo, a causa delle differenze di tasso d’interesse a breve termine tra le due valute.

- I titoli del Fondo potrebbero diventare difficili da valutare o da vendere al prezzo e con le tempistiche desiderati, specie in condizioni di mercato estreme con il prezzo delle attività in calo, aumentando il rischio di perdite sull'investimento.

- Il Fondo può sostenere un livello di costi di operazione più elevato per effetto dell’investimento su mercati caratterizzati da una minore attività di contrattazione o meno sviluppati rispetto a un fondo che investa su mercati più attivi/sviluppati.

- Le spese correnti possono essere prelevate, in tutto o in parte, dal capitale, il che potrebbe erodere il capitale o ridurne il potenziale di crescita.

- Il Fondo potrebbe perdere denaro se una controparte con la quale il Fondo effettua scambi non fosse più intenzionata ad adempiere ai propri obblighi, o a causa di un errore o di un ritardo nei processi operativi o di una negligenza di un fornitore terzo.

- Oltre al reddito, questa classe di azioni può distribuire plusvalenze di capitale realizzate e non realizzate e il capitale inizialmente investito. Sono dedotti dal capitale anche commissioni, oneri e spese. Entrambi i fattori possono comportare l’erosione del capitale e un potenziale ridotto di crescita del medesimo. Si richiama l’attenzione degli investitori anche sul fatto che le distribuzioni di tale natura possono essere trattate (e quindi imponibili) come reddito, secondo la legislazione fiscale locale.

Specific risks

- Le Azioni/Quote possono perdere valore rapidamente e di norma implicano rischi più elevati rispetto alle obbligazioni o agli strumenti del mercato monetario. Di conseguenza il valore del proprio investimento potrebbe diminuire.

- Le azioni di società a piccola e media capitalizzazione possono presentare una maggiore volatilità rispetto a quelle di società più ampie e talvolta può essere difficile valutare o vendere tali azioni al momento e al prezzo desiderati, il che aumenta il rischio di perdite.

- Un Fondo che presenta un’esposizione elevata a un determinato paese o regione geografica comporta un livello maggiore di rischio rispetto a un Fondo più diversificato.

- Il Fondo si concentra su determinati settori o temi d’investimento e potrebbe risentire pesantemente di fattori quali eventuali variazioni ai regolamenti governativi, una maggiore competizione nei prezzi, progressi tecnologici ed altri eventi negativi.

- Questo Fondo può avere un portafoglio particolarmente concentrato rispetto al suo universo d’investimento o altri fondi del settore. Un evento sfavorevole riguardante anche un numero ridotto di partecipazioni potrebbe creare una notevole volatilità o perdite per il Fondo.

- Il Fondo potrebbe usare derivati al fine di conseguire il suo obiettivo d'investimento. Ciò potrebbe determinare una "leva", che potrebbe amplificare i risultati dell'investimento, e le perdite o i guadagni per il Fondo potrebbero superare il costo del derivato. I derivati comportano rischi aggiuntivi, in particolare il rischio che la controparte del derivato non adempia ai suoi obblighi contrattuali.

- Qualora il Fondo detenga attività in valute diverse da quella di base del Fondo o l'investitore detenga azioni o quote in un'altra valuta (a meno che non siano "coperte"), il valore dell'investimento potrebbe subire le oscillazioni del tasso di cambio.

- Se il Fondo, o una sua classe di azioni con copertura, intende attenuare le fluttuazioni del tasso di cambio tra una valuta e la valuta di base, la stessa strategia di copertura potrebbe generare un effetto positivo o negativo sul valore del Fondo, a causa delle differenze di tasso d’interesse a breve termine tra le due valute.

- I titoli del Fondo potrebbero diventare difficili da valutare o da vendere al prezzo e con le tempistiche desiderati, specie in condizioni di mercato estreme con il prezzo delle attività in calo, aumentando il rischio di perdite sull'investimento.

- Il Fondo potrebbe perdere denaro se una controparte con la quale il Fondo effettua scambi non fosse più intenzionata ad adempiere ai propri obblighi, o a causa di un errore o di un ritardo nei processi operativi o di una negligenza di un fornitore terzo.