Key takeaways:

- Inflation came in softer than expected in April, with the most important takeaway being the significant reduction in core services excluding housing (aka, supercore inflation), which fell to 2.8% from 4.8% a year ago.

- Despite the win on inflation, market uncertainty and interest-rate volatility may remain elevated until May or June’s inflation report, when we’re likely to see the full impact of tariff policies on inflation.

- With yields continuing to hover near their highest levels since 2007, we believe bond investors should see rangebound yields as an opportunity to continue reinvesting at attractive levels.

The numbers

Like March’s reading, inflation came in softer than expected in April, given the 0.2% month-over-month (MoM) rise in both headline (+0.221%) and core (+0.237%) inflation. This brings the headline Consumer Price Index (CPI) year-over-year (YoY) number to 2.33%, down materially from 3.35% a year ago. Core CPI was up comparatively more than headline, at +2.78% YoY, but was also down materially from 3.62% a year ago.

In our view, the most important takeaway from April’s report was the big reduction in core services excluding housing (aka, supercore inflation) to 2.8%, a significant drop from 4.8% a year ago.

What it means for the bond market

Unfortunately, given the overarching tariff situation, this was probably one of the least important CPI prints since the inflation spike of 2022.

Market participants are more concerned with the expected uptick in inflation due to the tariffs announced on Liberation Day, which will likely not show up until May or June’s numbers are released. The market will wait with bated breath for those readings before determining where we stand on tariff-induced price increases. We think market uncertainty – coupled with interest rate volatility – may remain elevated in the interim.

We expect that bond prices and yields are likely to stay rangebound (as they have been so far in 2025) until we get more clarity on the fluid tariff situation and the Fed’s reaction to anticipated higher inflation in coming months.

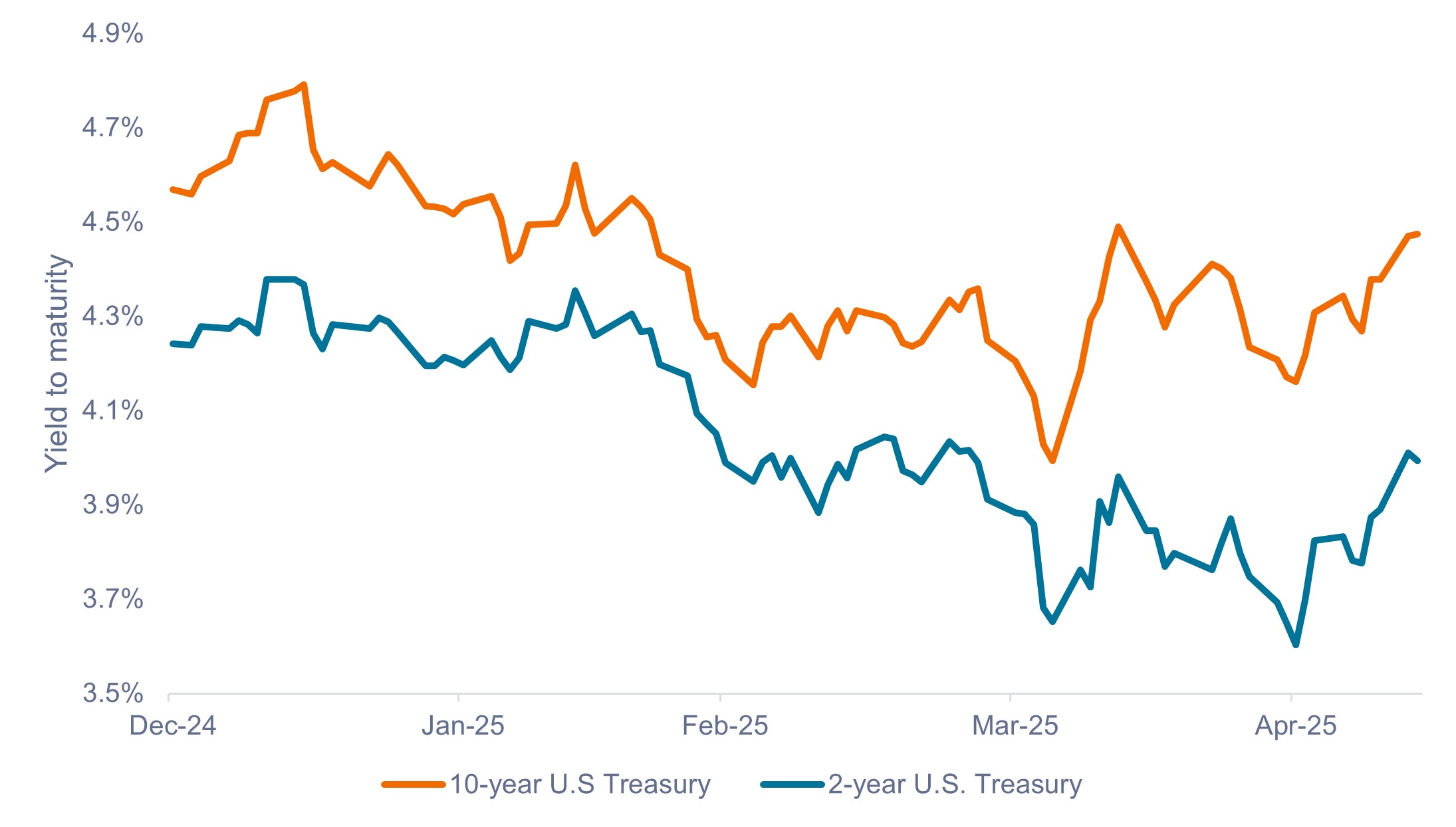

Exhibit 1: Yields on U.S. Treasuries (Jan 2025 – May 2025)

Treasury yields likely to remain rangebound until the full impacts of tariff policy become clear.

Source: Bloomberg, as of 13 May 2025. Past performance does not predict future returns.

What it means for the Fed

In our view, April’s benign inflation numbers mean that the Fed will probably be on hold for the foreseeable future, as inflation has continued to fall and unemployment has held steady thus far.

As of 13 May 2025, the market is pricing in only an 8% and 41% chance of a cut at the Fed’s June and July meetings, respectively. Notably, the market was pricing in nearly a 100% chance of a cut by July at the end of April.

What it means for investors

Rangebound bond yields may be anathema to investors hoping for rapid bond price appreciation due to a drop in yields, but we think it is important not to miss the forest for the trees.

Coupon, or interest income, has historically been the most significant contributor to total returns on fixed income, and we anticipate that trend will continue in the current environment. Consequently, current starting yields have historically been a highly reliable predictor of 5-year forward returns on fixed income.1

With interest rates remaining around their highest levels since 2007, we believe investors should view rangebound yields as an opportunity to continue reinvesting at attractive yields – something they likely wouldn’t be able to do if yields fell sharply.

IMPORTANT INFORMATION

Fixed income securities are subject to interest rate, inflation, credit and default risk. The bond market is volatile. As interest rates rise, bond prices usually fall, and vice versa. The return of principal is not guaranteed, and prices may decline if an issuer fails to make timely payments or its credit strength weakens.

1 Between 1976 and 2023, there was a correlation of 0.94 between the yield to worst on the Bloomberg U.S. Aggregate Bond Index (U.S. Agg) and its 5-year forward return.

The Bloomberg US Aggregate Bond Index, is a broad base, market capitalization-weighted bond market index representing intermediate term investment grade bonds traded in the United States.

The Consumer Price Index (CPI) is a measure of the average change over time in the prices paid by urban consumers for a basket of consumer goods and services. It’s a key economic indicator used to track inflation, which is the general increase in the cost of goods and services in an economy.

Correlation refers to the relationship between the price movements of different assets within a portfolio or between different asset classes. It’s a statistical measure that quantifies how much the returns of two assets tend to move together, either positively, negatively, or not at all. A perfect positive correlation means that the correlation coefficient is exactly 1. This implies that as one security moves, either up or down, the other security moves in lockstep, in the same direction. A perfect negative correlation means that two assets move in opposite directions, while a zero correlation implies no linear relationship at all.

Range-bound yields refer to a situation where the yields on bonds (or other interest-bearing securities) are fluctuating within a defined upper and lower limit. This indicates that the market is not trending significantly higher or lower, but rather oscillating between those price levels.

Volatility measures risk using the dispersion of returns for a given investment.

Yield to worst (YTW) is a measure of the lowest possible yield an investor can expect to receive on a bond, assuming the bond doesn’t default. It’s calculated by considering all potential call dates and the yield to maturity, and is particularly relevant for callable bonds where the issuer can redeem the bond before maturity.

Queste sono le opinioni dell'autore al momento della pubblicazione e possono differire da quelle di altri individui/team di Janus Henderson Investors. I riferimenti a singoli titoli non costituiscono una raccomandazione all'acquisto, alla vendita o alla detenzione di un titolo, di una strategia d'investimento o di un settore di mercato e non devono essere considerati redditizi. Janus Henderson Investors, le sue affiliate o i suoi dipendenti possono avere un’esposizione nei titoli citati.

Le performance passate non sono indicative dei rendimenti futuri. Tutti i dati dei rendimenti includono sia il reddito che le plusvalenze o le eventuali perdite ma sono al lordo dei costi delle commissioni dovuti al momento dell'emissione.

Le informazioni contenute in questo articolo non devono essere intese come una guida all'investimento.

Non vi è alcuna garanzia che le tendenze passate continuino o che le previsioni si realizzino.

Comunicazione di Marketing.

Important information

Please read the following important information regarding funds related to this article.

- Gli emittenti di obbligazioni (o di strumenti del mercato monetario) potrebbero non essere più in grado di pagare gli interessi o rimborsare il capitale, ovvero potrebbero non intendere più farlo. In tal caso, o qualora il mercato ritenga che ciò sia possibile, il valore dell'obbligazione scenderebbe.

- L’aumento (o la diminuzione) dei tassi d’interesse può influire in modo diverso su titoli diversi. Nello specifico, i valori delle obbligazioni si riducono di norma con l'aumentare dei tassi d'interesse. Questo rischio risulta di norma più significativo quando la scadenza di un investimento obbligazionario è a più lungo termine.

- Il Fondo investe in obbligazioni ad alto rendimento (non investment grade) che, sebbene offrano di norma un interesse superiore a quelle investment grade, sono più speculative e più sensibili a variazioni sfavorevoli delle condizioni di mercato.

- Alcune obbligazioni (obbligazioni callable) consentono ai loro emittenti il diritto di rimborsare anticipatamente il capitale o di estendere la scadenza. Gli emittenti possono esercitare tali diritti laddove li ritengano vantaggiosi e, di conseguenza, il valore del Fondo può esserne influenzato.

- Un Fondo che presenta un’esposizione elevata a un determinato paese o regione geografica comporta un livello maggiore di rischio rispetto a un Fondo più diversificato.

- Il Fondo potrebbe usare derivati al fine di conseguire il suo obiettivo d'investimento. Ciò potrebbe determinare una "leva", che potrebbe amplificare i risultati dell'investimento, e le perdite o i guadagni per il Fondo potrebbero superare il costo del derivato. I derivati comportano rischi aggiuntivi, in particolare il rischio che la controparte del derivato non adempia ai suoi obblighi contrattuali.

- Se il Fondo, o una sua classe di azioni con copertura, intende attenuare le fluttuazioni del tasso di cambio tra una valuta e la valuta di base, la stessa strategia di copertura potrebbe generare un effetto positivo o negativo sul valore del Fondo, a causa delle differenze di tasso d’interesse a breve termine tra le due valute.

- I titoli del Fondo potrebbero diventare difficili da valutare o da vendere al prezzo e con le tempistiche desiderati, specie in condizioni di mercato estreme con il prezzo delle attività in calo, aumentando il rischio di perdite sull'investimento.

- Il Fondo può sostenere un livello di costi di operazione più elevato per effetto dell’investimento su mercati caratterizzati da una minore attività di contrattazione o meno sviluppati rispetto a un fondo che investa su mercati più attivi/sviluppati.

- Le spese correnti possono essere prelevate, in tutto o in parte, dal capitale, il che potrebbe erodere il capitale o ridurne il potenziale di crescita.

- Il Fondo potrebbe perdere denaro se una controparte con la quale il Fondo effettua scambi non fosse più intenzionata ad adempiere ai propri obblighi, o a causa di un errore o di un ritardo nei processi operativi o di una negligenza di un fornitore terzo.

- Oltre al reddito, questa classe di azioni può distribuire plusvalenze di capitale realizzate e non realizzate e il capitale inizialmente investito. Sono dedotti dal capitale anche commissioni, oneri e spese. Entrambi i fattori possono comportare l’erosione del capitale e un potenziale ridotto di crescita del medesimo. Si richiama l’attenzione degli investitori anche sul fatto che le distribuzioni di tale natura possono essere trattate (e quindi imponibili) come reddito, secondo la legislazione fiscale locale.