Key takeaways:

- After several years of headwinds, the backdrop for pharma and biotech has turned more constructive, supported by improved policy visibility, renewed M&A activity, and strong market performance.

- Amid a more stable environment, investor focus is shifting back to innovation and emerging treatment paradigms as critical long-term growth drivers.

- With a dense slate of drug launches, clinical readouts, and regulatory decisions unfolding through 2026, we highlight where investors should be looking for the most impactful events likely to influence sector outcomes and differentiation.

Can pharma and biotech stocks build on their recent momentum? After several years of headwinds, sentiment toward these sectors turned more constructive toward the end of last year, supported by greater clarity around policy risks and renewed merger and acquisition (M&A) activity.

Despite concerns about leadership turnover and funding constraints at the Food and Drug Administration (FDA), the agency largely continued to function, with the number of drug approvals in 2025 broadly in line with long‑term averages. And as trade policy and drug‑pricing reforms became better understood, potential impacts were increasingly viewed as manageable, helping fuel a strong rebound in pharma and biotech stocks as the year progressed.

That strong performance has extended into 2026. Alongside the easing of headwinds, the more defensive characteristics of these stocks may be providing further support amid uncertainty around AI-driven disruption that has pressured other pockets of the market. At the same time, AI is widely viewed as an enabler for drug developers, helping accelerate research and development and shorten timelines to market.

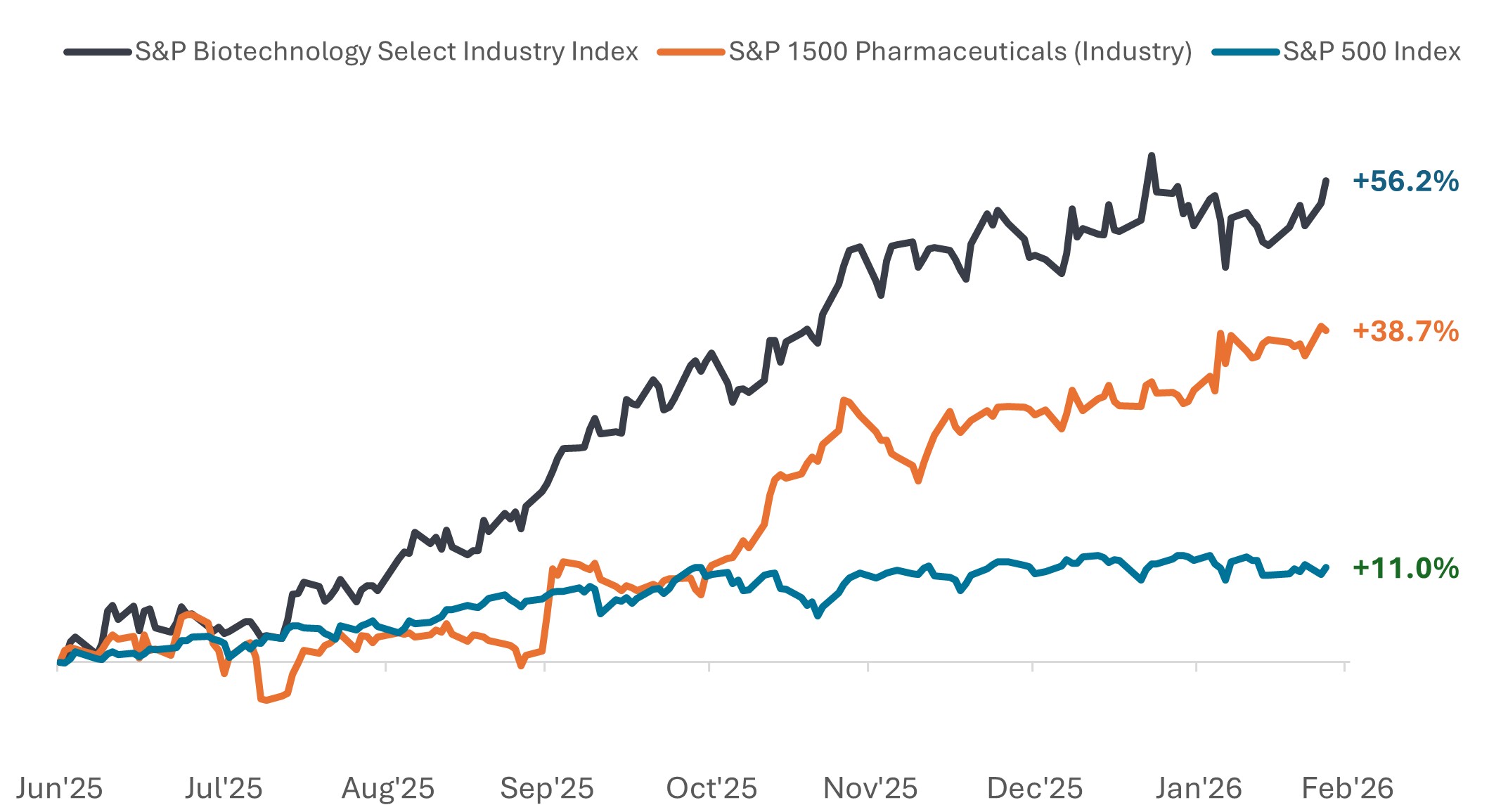

Pharma and biotech have notably outperformed since mid-2025

Price performance from 30 June 2025 to 24 February 2026.

Source: Bloomberg, data from 30 June 2025 to 24 February 2026. The S&P Biotechnology Select Industry Index comprises stocks in the S&P Total Market Index that are classified in the GICS Biotechnology sub-industry. The S&P 1500 Pharmaceuticals (Industry) comprises stocks included in the S&P Composite 1500® that are classified as members of the GICS Pharmaceuticals industry. Past performance does not predict future results.

With a more constructive backdrop, 2026 is full of potential catalysts

The combination of improved visibility and strong market performance has supported a more favorable environment, further bolstered by renewed optimism around strategic dealmaking and a potential reopening of the initial public offering (IPO) market. More importantly, the increasingly constructive backdrop has shifted attention back to what has always driven the sector over the long term: innovation.

On that front, 2026 is shaping up to be a catalyst‑rich year, with a number of highly anticipated drug launches, clinical trial readouts, and regulatory decisions across several major treatment areas. Below, we highlight some of the key events investors will be watching for signals that could shape sector dynamics in the year ahead.

Big pharma: Major treatment paradigms in transition

For the pharmaceutical industry, several high‑profile clinical and regulatory milestones are set to test whether recent innovation can translate into durable growth. New treatment paradigms are also emerging. Upcoming events have the potential to reshape standards of care and influence how investors think about competitive positioning.

Obesity & cardiometabolic treatments: From proof‑of‑concept to scale and competition

After years of clinical and market validation, the obesity market has moved decisively beyond whether GLP-1 therapies work. The focus in 2026 shifts to how these drugs are delivered, how broadly they can be scaled, and how patients and consumers will segment across treatment options. Investors will also be watching how additional payer channels open up, shaping access, affordability, and the long‑term size of the market.

Catalysts to watch:

- Oral GLP‑1s (“year of the pill”): Real‑world uptake of oral formulations – most notably Novo Nordisk’s recently approved oral Wegovy (semaglutide) and the pending FDA decision on Eli Lilly’s orforglipron (expected April 2026) – will test whether pills can meaningfully expand the treated population beyond injectables. Importantly, oral therapies could broaden global reach by simplifying distribution and storage, potentially improving access in markets where injectable cold‑chain logistics are a constraint.

- Next‑generation combinations: Late‑February Phase 3 data showed Novo Nordisk’s experimental shot CagriSema delivered strong weight loss but fell short of Eli Lilly’s high-dose Zepbound in a head-to-head trial. Patients on CagriSema lost 23.0% of body weight over 84 weeks, compared with 25.5% for Zepbound, underscoring the high efficacy bar for GLP-1 combinations.

- Multi‑agonists: Ongoing late‑stage readouts from Eli Lilly’s retatrutide injectable throughout 2026 will help determine whether activating multiple metabolic pathways can push weight‑loss results meaningfully higher without creating side‑effect tradeoffs that limit long‑term use. For investors, the balance between added efficacy and patient tolerability is critical as companies look for the next step beyond today’s GLP‑ Competition is also building, with Amgen’s monthly MariTide, Roche’s CT‑388, and Boehringer’s survodutide advancing in late‑stage trials, alongside a growing wave of amylin‑based therapies entering or approaching Phase 3, led by Novo Nordisk, Eli Lilly, and Roche.

Neuroscience: Moving treatment earlier and broader

Neuroscience is emerging as another area where innovation could meaningfully expand treated populations. Advances in trial design and biomarkers are enabling programs that move earlier in disease progression and test mechanisms beyond legacy approaches.

Catalysts to watch

- Earlier‑intervention Alzheimer’s trials: Investor attention is increasingly focused on studies evaluating treatment at earlier stages, before symptoms become apparent but when biological signs of Alzheimer’s are already present. Eli Lilly’s TRAILBLAZER‑ALZ 3 trial (TB3) of donanemab in biomarker‑defined, preclinical Alzheimer’s disease is widely viewed as a potential category‑shaping program. While full results are not expected until 2027 and interim disclosure in 2026 is uncertain, any update could influence sentiment around earlier intervention and long‑term market expansion opportunities.

- Next-generation delivery technologies: Newer amyloid programs are focused on improving how treatments reach the brain to enhance safety and patient convenience. Brain‑shuttle technologies, including programs in development from Roche and private companies such as Korsana, aim to deliver higher drug exposure while potentially reducing side‑effect risk and enabling less frequent and subcutaneous dosing. If successful, these advances could address key limitations of earlier therapies and support broader adoption.

- Symptom‑focused programs: Several late‑stage programs are targeting neuropsychiatric symptoms such as psychosis and agitation, where unmet need remains high and clinical endpoints are more straightforward. In Alzheimer’s psychosis, Bristol Myers Squibb is expected to report multiple ADEPT readouts for Cobenfy in the second half of 2026, while Acadia and Alkermes anticipate mid‑ to late‑2026 data from Phase 2/3 programs. In agitation, Axsome is also awaiting a potential FDA decision for AXS‑05 in mid‑ For investors, these programs stand out because clearer symptom improvement can translate more directly into clinical adoption and commercial uptake if approved.

- Mechanistic diversification: Beyond treatments that target amyloid plaques, investors are increasingly watching programs aimed at other underlying drivers of neurodegeneration, including tau pathology, inflammation, and synaptic function, which are linked to how brain cells communicate and deteriorate over time. Readouts from programs at Biogen, Eisai, Acumen, and ProMIS Neurosciences through 2026 will help inform whether these alternative approaches can complement first‑generation therapies or extend benefits to a broader group of patients.

Biotech: Breadth of catalysts on the horizon

In biotech, 2026 features a diverse set of catalysts, with a dense slate of data readouts and regulatory decisions across liver disease, renal conditions, oncology, and a range of rare disease and specialty indications. Together, these events could drive meaningful dispersion as pipelines advance.

Catalysts to watch:

- Liver / MASH pivotal data: One of the most closely watched biotech events in 2026 is Inventiva’s Phase 3 NATiV3 trial of lanifibranor for metabolic dysfunction–associated steatohepatitis (MASH), a serious form of fatty liver disease linked to obesity and diabetes that currently has limited treatment options. With topline results expected in the second half of the year, the readout carries heightened importance given the mixed history of prior late‑stage programs for this field. A positive outcome could help rebuild confidence in oral therapies that target multiple disease pathways in a space where commercial expectations remain cautious.

- Renal regulatory milestones: Several high‑visibility FDA decisions are expected in kidney disease in 2026, led by Travere Therapeutics’ FILSPARI, which is seeking a label expansion into focal segmental glomerulosclerosis (FSGS), a rare and progressive disorder that can lead to kidney failure and currently has limited treatment options. The FDA extended its decision date to April, making this one of the most closely watched renal regulatory events of the year. A positive decision would represent a meaningful clinical advance in a small but commercially important rare‑disease market.

- Oncology moving toward biology‑driven programs: In cancer care, innovation is increasingly shifting toward treatments tailored to the underlying biology of a tumor, with the goal of better matching drugs to the patients most likely to benefit. Several high‑profile readouts in 2026 will test whether this approach can deliver meaningful differentiation. Notably, Roche’s giradestrant data in first‑line metastatic breast cancer, expected in late March or early April, will serve as an important read‑through for Olema’s palazestrant (with Phase 3 OPERA‑01 data expected in the second half of the year) and AstraZeneca’s camizestrant in the SERENA‑4 Other influential readouts include Ideaya’s darovasertib‑plus‑crizotinib combination in metastatic uveal melanoma, with Phase 2/3 data anticipated in late March, and Revolution Medicines’ Phase 3 study in second‑line pancreatic cancer, with results expected in the first half of 2026. Together, these readouts will help clarify whether more targeted approaches can deliver meaningful differentiation in competitive settings.

Implications for investors

With the policy overhangs of early 2025 now in the rearview, performance across pharma and biotech in 2026 will likely be driven increasingly by fundamentals: execution, clinical milestones, and pipeline advancement.

Against a backdrop of major drug launches, data readouts, and regulatory decisions, investors have ample reason to stay engaged as the year progresses. For those focused on the long term, separating durable innovation from near‑term noise will be key.

S&P 500® Index reflects U.S. large-cap equity performance and represents broad U.S. equity market performance.

S&P Biotechnology Select Industry Index comprises stocks in the S&P Total Market Index that are classified in the GICS® Biotechnology sub-industry.

S&P 1500 Pharmaceuticals (Industry) comprises stocks included in the S&P Composite 1500® that are classified as members of the GICS® Pharmaceuticals industry.

IMPORTANT INFORMATION

Diversification neither assures a profit nor eliminates the risk of experiencing investment losses.

Equity securities are subject to risks including market risk. Returns will fluctuate in response to issuer, political and economic developments.

Health care industries are subject to government regulation and reimbursement rates, as well as government approval of products and services, which could have a significant effect on price and availability, and can be significantly affected by rapid obsolescence and patent expirations.

Initial Public Offerings (IPOs) are highly speculative investments and may be subject to lower liquidity and greater volatility. Special risks associated with IPOs include limited operating history, unseasoned trading, high turnover and non-repeatable performance.

These are the views of the author at the time of publication and may differ from the views of other individuals/teams at Janus Henderson Investors. References made to individual securities do not constitute a recommendation to buy, sell or hold any security, investment strategy or market sector, and should not be assumed to be profitable. Janus Henderson Investors, its affiliated advisor, or its employees, may have a position in the securities mentioned.

Past performance does not predict future returns. The value of an investment and the income from it can fall as well as rise and you may not get back the amount originally invested.

The information in this article does not qualify as an investment recommendation.

There is no guarantee that past trends will continue, or forecasts will be realised.

Marketing Communication.

Important information

Please read the following important information regarding funds related to this article.

- Shares/Units can lose value rapidly, and typically involve higher risks than bonds or money market instruments. The value of your investment may fall as a result.

- Shares of small and mid-size companies can be more volatile than shares of larger companies, and at times it may be difficult to value or to sell shares at desired times and prices, increasing the risk of losses.

- If a Fund has a high exposure to a particular country or geographical region it carries a higher level of risk than a Fund which is more broadly diversified.

- The Fund is focused towards particular industries or investment themes and may be heavily impacted by factors such as changes in government regulation, increased price competition, technological advancements and other adverse events.

- The Fund may use derivatives to help achieve its investment objective. This can result in leverage (higher levels of debt), which can magnify an investment outcome. Gains or losses to the Fund may therefore be greater than the cost of the derivative. Derivatives also introduce other risks, in particular, that a derivative counterparty may not meet its contractual obligations.

- If the Fund holds assets in currencies other than the base currency of the Fund, or you invest in a share/unit class of a different currency to the Fund (unless hedged, i.e. mitigated by taking an offsetting position in a related security), the value of your investment may be impacted by changes in exchange rates.

- When the Fund, or a share/unit class, seeks to mitigate exchange rate movements of a currency relative to the base currency (hedge), the hedging strategy itself may positively or negatively impact the value of the Fund due to differences in short-term interest rates between the currencies.

- Securities within the Fund could become hard to value or to sell at a desired time and price, especially in extreme market conditions when asset prices may be falling, increasing the risk of investment losses.

- The Fund could lose money if a counterparty with which the Fund trades becomes unwilling or unable to meet its obligations, or as a result of failure or delay in operational processes or the failure of a third party provider.

Specific risks

- Shares/Units can lose value rapidly, and typically involve higher risks than bonds or money market instruments. The value of your investment may fall as a result.

- Shares of small and mid-size companies can be more volatile than shares of larger companies, and at times it may be difficult to value or to sell shares at desired times and prices, increasing the risk of losses.

- If a Fund has a high exposure to a particular country or geographical region it carries a higher level of risk than a Fund which is more broadly diversified.

- The Fund is focused towards particular industries or investment themes and may be heavily impacted by factors such as changes in government regulation, increased price competition, technological advancements and other adverse events.

- The Fund may use derivatives to help achieve its investment objective. This can result in leverage (higher levels of debt), which can magnify an investment outcome. Gains or losses to the Fund may therefore be greater than the cost of the derivative. Derivatives also introduce other risks, in particular, that a derivative counterparty may not meet its contractual obligations.

- If the Fund holds assets in currencies other than the base currency of the Fund, or you invest in a share/unit class of a different currency to the Fund (unless hedged, i.e. mitigated by taking an offsetting position in a related security), the value of your investment may be impacted by changes in exchange rates.

- When the Fund, or a share/unit class, seeks to mitigate exchange rate movements of a currency relative to the base currency (hedge), the hedging strategy itself may positively or negatively impact the value of the Fund due to differences in short-term interest rates between the currencies.

- Securities within the Fund could become hard to value or to sell at a desired time and price, especially in extreme market conditions when asset prices may be falling, increasing the risk of investment losses.

- The Fund may incur a higher level of transaction costs as a result of investing in less actively traded or less developed markets compared to a fund that invests in more active/developed markets.

- The Fund could lose money if a counterparty with which the Fund trades becomes unwilling or unable to meet its obligations, or as a result of failure or delay in operational processes or the failure of a third party provider.