Key takeaways:

- Kenya has materially strengthened its external position through FX reserve accumulation and proactive liability management, but persistent deficits, heavy debt servicing and weak revenue mobilisation remain a binding constraint on the credit story.

- International Monetary Fund (IMF) re-engagement remains elusive amid repeated reform slippage, limited political space for taxation and persistent social fragilities.

- Investors should look through near‑term macroeconomic gains and anchor views more on evidence of durable structural reform — particularly on revenue, spending discipline, and institutional follow‑through.

“Kenya’s macro story feels like stepping into a lighter patch of trees: more light, better visibility — but still deep inside the forest.”

On the surface, the picture has improved meaningfully: the balance of payments has adjusted, FX buffers are firmer, and debt rollover risks have eased. Beneath the surface, however, fiscal dynamics remain the binding constraint, with deficits, debt servicing, and revenue mobilisation continuing to weigh on policy flexibility.

On the surface of the canopy: External resilience

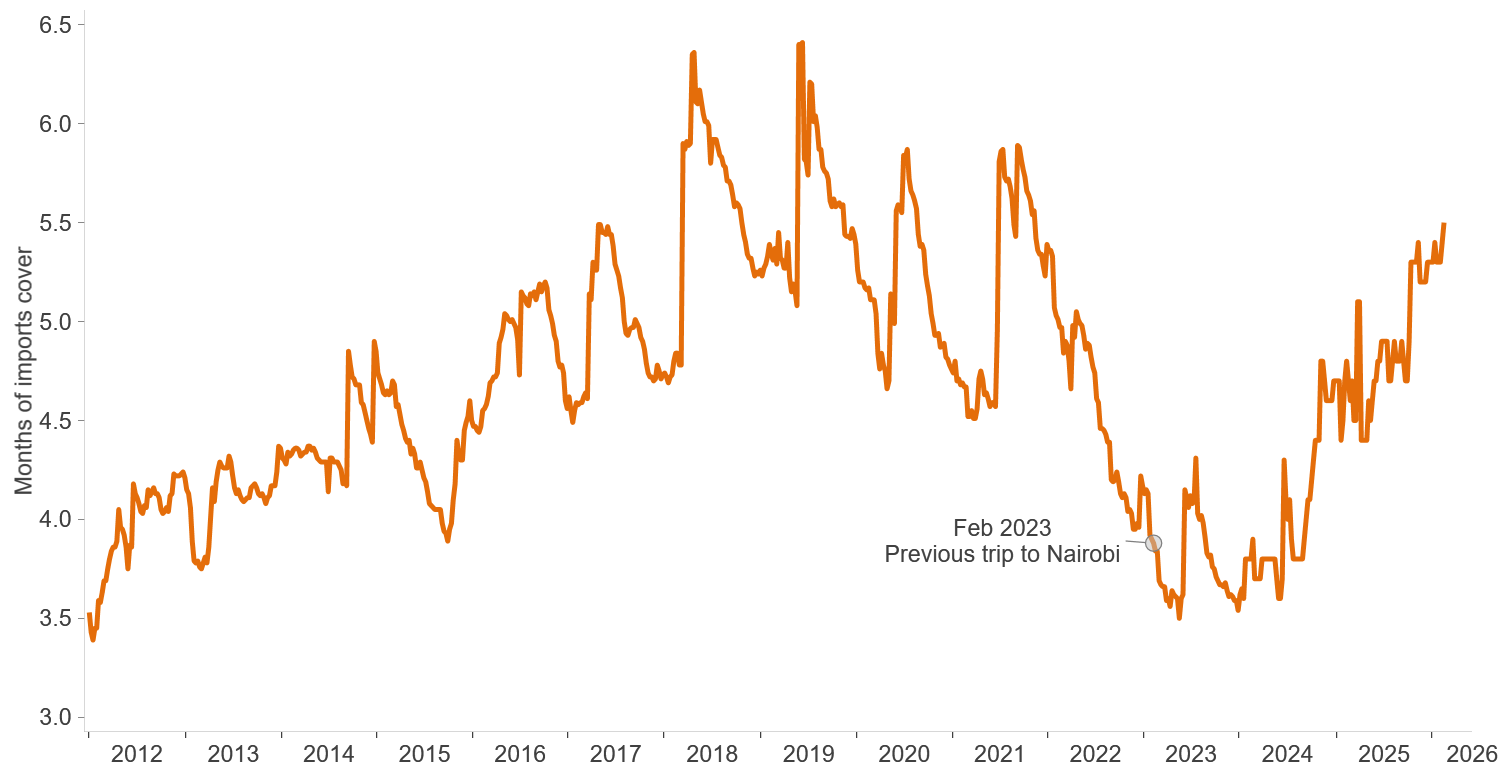

Having just returned from Nairobi, the most striking change since our 2023 trip is how markedly Kenya’s external situation has improved. Back then the country had to deal with a high external debt service (including a massive US$2 billion Eurobond amortisation) amid persistent current account deficits, dwindling FX reserves and uncertain market access.

Traffic in Nairobi, Janus Henderson

This time around Kenya met investors with a brighter landscape – one where its strong external buffers, stable macroeconomic conditions and more manageable external debt allowed it to return to international capital markets and receive credit rating upgrades.1 FX reserves rose to US$12.5 billion (from around US$7 billion as early as mid-2024) on the back of strong exports, remittances and tourism. This was also a deliberate policy of the Central Bank of Kenya (CBK) to build buffers during the ‘good times’ in preparation for any potential external or domestic shocks.

Central Bank of Kenya usable foreign exchange reserves

Source: Janus Henderson Investors and Macrobond, as at 20 February 2026. Months of import cover, based on 36 months average of imports of goods & non-factor services. Non-factor services are invisible, intangible trade items (excluding investment income and labour compensation) such as transportation, tourism, insurance, and banking, which are not directly attributable to primary factors of production.

On the liability side, last year the government conducted a series of successful liability management operations that moderated its near-term external liquidity pressures. It did so by issuing a series of Eurobonds to repurchase significant amounts of its outstanding 2027 and 2028 debt maturities, using the same template as in early 2024. The terms of its Standard Gauge Railway2 loan with China Exim Bank were also renegotiated by converting US$3.5 billion in Renminbi, extending the maturities to 2040 and lowering the coupons, saving over US$215 million (0.1% of GDP) in annual interest payments.3

Beneath the trees: fiscal constraints

Nairobi city skyline, Janus Henderson

While the external story is improving, the fiscal story remains stubbornly unchanged. Our discussions with policymakers, multilaterals, local banks and other relevant stakeholders revealed a consistent message: Kenya has plenty of options, but it lacks a credible fiscal story.

This was the core reason why the country’s previous IMF programme went astray last year after the government missed several key fiscal and structural reform benchmarks, resulting in over US$850 million being withheld by the IMF. Despite the National Treasury’s indication that negotiations toward a new arrangement will resume, our trip suggested limited prospects for success, as meaningful gaps persist between the two sides that obstruct the path forward, despite a mutual willingness to engage.

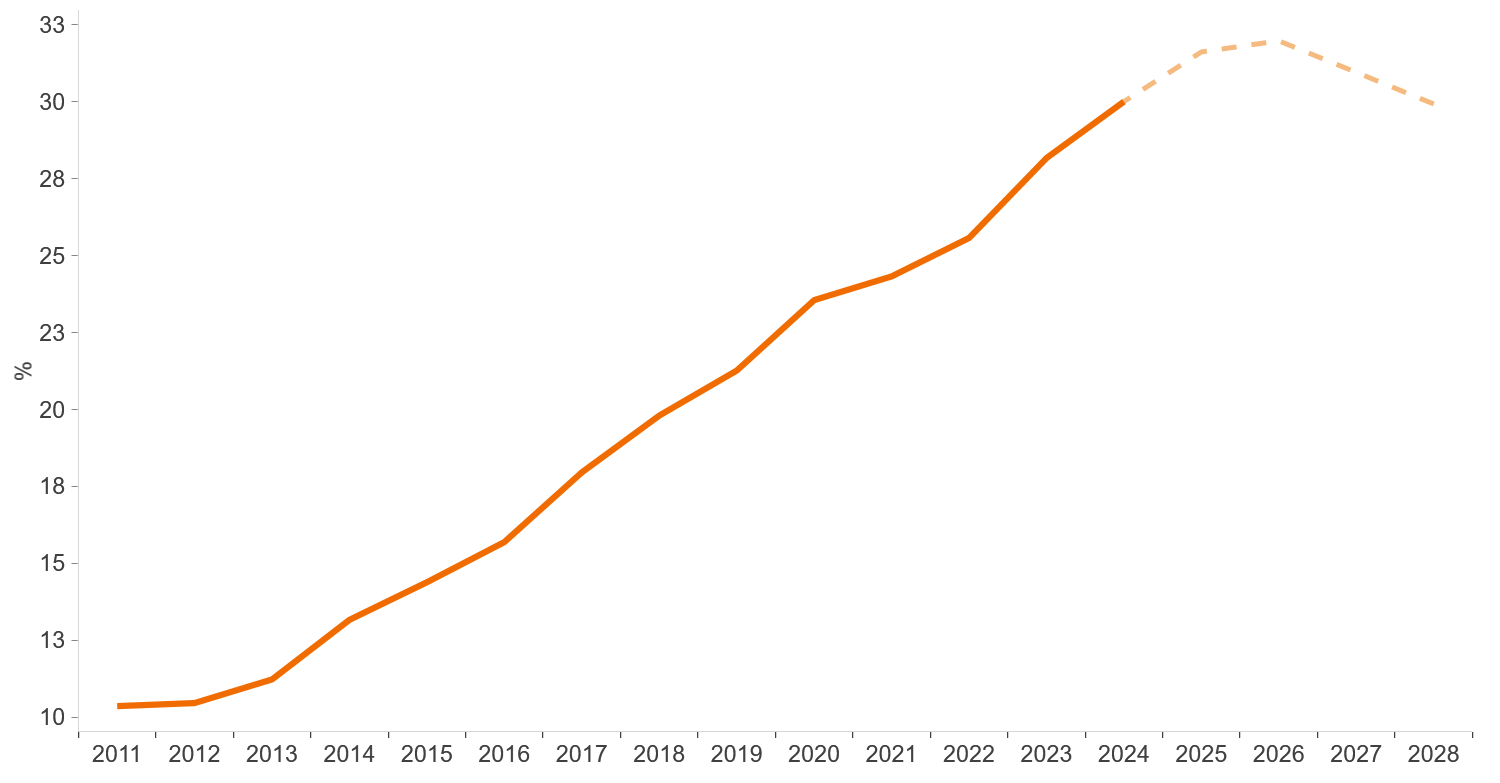

Unfortunately, Kenya’s fiscal slippages have become the norm. While for the 2025 fiscal year4 the deficit turned out worse than initially projected, for the current fiscal year (2026), the most recent estimate of the deficit is 6% of GDP, a significant miss relative to the original 4.7% of GDP target. Recent social unrest5 has reminded policymakers just how narrow Kenya’s political room for manoeuvre on taxation really is, leaving spending cuts as the blunt instrument of choice to rein in deficits. With interest payments consuming about a third of government revenues (as shown by the interest to revenue ratio), fiscal rigidity all but guarantees that development and social spending would take the hit – an outcome that may balance the books today but undermines the case for a durable fiscal consolidation tomorrow.

Debt interest-to-revenue ratio

Source: Janus Henderson Investors, Macrobond, as at 20 February 2026. There is no guarantee that past trends will continue, or forecasts will be realised.

Temporary shelters for the rainy season

In the face of these constraints, policymakers had to come up with innovative solutions that raised concerns of their own. They increased the use of securitisations6 and Public Private Partnership‑like structures to fund infrastructure and other projects. While politically attractive, these instruments blur the line between on‑ and off‑balance‑sheet liabilities. Both the IMF and World Bank are clear that in their view these are still in effect public debt — and that their expansion weakens fiscal transparency and complicates programme design.

Privatisation has provided the government with another way to plug funding gaps, but the harder question is no longer whether to sell, but what to do with the cash once it arrives. Offloading profitable, dividend‑paying assets such as partly state-owned Safaricom and the Kenya Pipeline Company only makes sense if the proceeds are invested at a higher return or used to retire expensive debt and not used to finance current expenditure.

Meaningful fiscal consolidation requires something Kenya currently lacks: the trust of its citizens. Across our meetings, the same message surfaced repeatedly and clearly – that the social contract is broken, and that corruption and elite capture7 carry tangible economic costs, from weak tax compliance to subdued foreign direct investment (FDI) inflows. Without progress on restoring trust, any serious attempt at austerity risks triggering renewed unrest, leaving the government caught between fiscal imperatives and social limits, a dilemma exacerbated by the proximity of general elections August next year.

Narrow paths and fallen branches: funding frictions

In principle, Kenya retains access to a range of external financing sources beyond the IMF and international capital markets. The authorities continue to highlight strong relationships with multilaterals such as the World Bank and the African Development Bank Group, as well as with key bilateral partners including the US, China and the United Arab Emirates. That said, while such support tended to materialise in the past, this time we encountered growing scepticism around the execution of recent financing initiatives, exemplified by the US$750 million8 World Bank DPO (Development Policy Operation), which remains stalled due to unmet prior actions and questions over the country’s overall macroeconomic adequacy in the absence of an IMF programme. The delay in securing the DPO also casts a shadow over Kenya’s proposed US$500m Sustainability-Linked Bond, which was intended to garner support from other institutional donors. On a more constructive note, authorities expect the US$1 billion debt-for-food swap9 to be executed by June, and an additional US$1 billion remains available from the US$1.5 billion UAE facility agreed last year.

Kenyatta International Convention Centre (KICC), Janus Henderson

Fortunately, Kenya’s deep local market remains one of its key credit strengths. Banks, pension funds, insurers, and asset managers provide a stable bid for government securities, insulating the sovereign from the volatility that afflicts more externally dependent African peers. Domestic institutions also hold a significant share of Kenya’s Eurobond stock, underscoring the depth of local savings. However, this strength comes with trade‑offs. Heavy reliance on domestic borrowing raises debt‑service costs and risks crowding out private‑sector credit over time. Banks are increasingly skewed toward short‑dated instruments, reflecting both liquidity preferences and uncertainty around fiscal policy. While this mitigates duration risk for the financial system, it leaves the sovereign exposed to rollover risk if deficits remain elevated.

Lighter, but still in the forest

Nairobi’s skyline, Janus Henderson

Kenya’s recent economic progress is real — but it is also easy to misread. Falling inflation, a stable growth pattern, and rising external buffers have brought more light and clearer visibility, and in the short term that has delivered tangible results. But the terrain beyond that light has not fundamentally changed. Beneath the surface, long‑standing fiscal constraints and political incentives continue to pull the economy back toward familiar fault lines.

The risk for investors is not that Kenya is sliding backward, but that recent successes are mistaken for having cleared the forest rather than merely reached a lighter patch of trees. For investors, this argues for a disciplined, fundamentally‑aware approach: recognising Kenya’s strengths relative to EM peers, while remaining cautious about extrapolating short‑term gains into a durable fiscal turnaround.

1Moody’s was the latest CRA (credit rating agency) to upgrade Kenya from CCC+ to B- right on the day of our trip to Nairobi. This followed the S&P upgrade (from B- to B) in August 2025/

2The Standard Gauge Railway is Kenya’s single largest infrastructure programme. Once completed it will link the country’s port of Mombasa to neighbouring landlocked Uganda. The first section (Mombasa-Nairobi) was opened in 2017 with financing from China Exim Bank and built by China Road and Bridge Corporation, and a subsequent second section (Nairobi-Naivasha) was opened in 2019. Since then, Kenya has explored various financing options for the remaining section to the Ugandan border town of Malaba, including the latest proposal of securitising 90% of the annual Railway Development Levy.

3Bloomberg, ‘Kenya snags $215 million saving after Chinese loan currency swap’, 07 October 2025.

4The fiscal year in Kenya runs from 1st July to 30th June.

52024 saw nationwide protests against the 2024 Finance Bill, which escalated into the storming of parliament and a violent security response that left at least several dozen people dead and hundreds injured, ultimately forcing the government to withdraw the bill. Next year saw renewed protests driven primarily by concerns over governance and cost‑of‑living pressures.

6One example is the Talanta Sports City stadium, funded via a US$345m infrastructure Asset-backed Securities (ABS) listed on the local market in July 2025. The ABS is secured by future inflows derived from betting and gaming taxes. The government recently announced plans to securitise 90% of the Railway Levy to fund the extension of the SGR from Naivasha to Kisumu.

7Elite capture is a term used in economics, development, and governance to describe a situation where a small, powerful group (‘elites’) disproportionately influence or control public resources, policies, or institutions for their own benefit, rather than for the broader population.

8World Bank, ‘Infrastructure Modernization for South Africa Development Policy Loan’, 9 June 2025.

9Kenya and the U.S. International Development Finance Corporation have agreed to a US$1 billion debt-for-food swap, during Kenyan President William Ruto’s visit to Washington in December 2025. This would allow Kenya to replace costly existing debt with lower-cost financing on condition it channelled the savings towards programmes to boost food security.

IMPORTANT INFORMATION

Emerging market investments have historically been subject to significant gains and/or losses. As such, returns may be subject to volatility.

Sovereign: Typically refers to debt issued by a national government. Sovereign bonds are backed by the country’s creditworthiness and ability to repay.

Sovereign debt securities are subject to the additional risk that, under some political, diplomatic, social or economic circumstances, some developing countries that issue lower quality debt securities may be unable or unwilling to make principal or interest payments as they come due.

Securitized products, such as mortgage-backed securities and asset-backed securities, are more sensitive to interest rate changes, have extension and prepayment risk, and are subject to more credit, valuation and liquidity risk than other fixed-income securities.

The balance of payments is a systematic record of all economic transactions between a country’s residents and the rest of the world over a specific period, typically a quarter or a year. It tracks the inflow and outflow of money, including trade in goods/services, investment income, and financial transfers.

Coupon: A regular interest payment that is paid on a bond described as a percentage of the face value of an investment. For example, if a bond has a face value of £100 and a 5% annual coupon, the bond will pay £5 a year in interest.

Credit rating: An independent assessment of the creditworthiness of a borrower by a recognised agency such as Standard & Poors, Moody’s, or Fitch. Standardised scores such as ‘AAA’ (a high credit rating) or ‘B’ (a low credit rating) are used, although other agencies may present their ratings in different formats.

Current account deficit: Where the value of goods and services that is imported by a country exceeds the value of the goods and services that it exports.

Debt servicing is the cash required to cover the repayment of interest and principal on outstanding debts (loans, bonds, leases) over a specific period, such as monthly or annually.

Duration risk is the sensitivity of a bond’s price to changes in interest rates, measuring how much a bond’s value will rise or fall when rates change. Generally, if interest rates rise, bond prices fall, with higher-duration bonds experiencing steeper price drops. It is typically expressed in years.

Economic cost is the total value of resources used to produce a good or service, comprising both explicit (accounting) costs (direct monetary payments) and implicit (opportunity) costs (the value of the next best alternative forgone). It represents the true cost of a decision, often used for assessing profitability.

A Eurobond is an international debt instrument issued by a government or corporation in a currency foreign to the country where it is issued. These bonds are typically underwritten by an international syndicate and sold in multiple countries, allowing borrowers to access capital in diverse markets. Despite the name, they are not necessarily denominated in Euro currency or limited to Europe.

Eurobond amortisation simply means paying back the principal on a Eurobond as it comes due.

Extending debt maturity involves renegotiating loan terms to push repayment dates further into the future, providing companies with breathing room to manage liquidity, avoid default, and avoid immediate, costly asset liquidation. It is a form of debt restructuring or “amend and extend” transaction, often involving higher interest rates or fees to compensate lenders for longer risk exposure.

An external position refers to the total stock of financial assets and liabilities an economic entity (bank, company, or country) holds against non-residents at a specific point in time. It is used to measure international investment positions (IIP), foreign exposure, and balance of payments, comprising direct investment, portfolio investment, and loans.

Fiscal consolidation is a government policy strategy designed to reduce budget deficits and public debt accumulation through, for example, spending cuts or tax increases. It involves discretionary, long-term actions to improve structural fiscal balances and strengthen public finances. The goal is to lower the debt-to-GDP ratio to enhance economic stability.

A fiscal deficit is the shortfall that occurs when a government’s total expenditures exceed its total revenue (excluding borrowing) in a financial year. It indicates that the government is spending beyond its means, requiring it to borrow from domestic or foreign sources to cover the difference.

Fiscal policy: Describes government policy relating to setting tax rates and spending levels. Fiscal policy is separate from monetary policy, which is typically set by a central bank. Fiscal austerity refers to raising taxes and/or cutting spending in an attempt to reduce government debt. Fiscal expansion (or ‘stimulus’) refers to an increase in government spending and/or a reduction in taxes.

Foreign Direct Investment (FDI) is a cross-border investment where an investor from one economy establishes a lasting interest and significant management influence (typically 10% or more voting power) in an enterprise located in another country. It involves long-term commitment, such as building factories, acquiring companies, or reinvesting profits, rather than just purchasing stocks.

FX reserve accumulation is the process by which a country’s central bank or monetary authority increases its holdings of foreign currency-denominated assets—such as foreign banknotes, bonds, and gold—to manage exchange rates, stabilize the economy, or provide self-insurance against financial crises. It is driven by trade surpluses or capital inflows and acts as a buffer against external shocks.

Interest payments are the periodic costs paid by a borrower to a lender for the use of borrowed money (the principal). These payments are distinct from repaying the original loan amount and are typically calculated as a percentage of the outstanding debt over a specific period.

Liability management operations (LMOs) are strategic financial techniques used by companies and banks to actively restructure, manage, or reduce outstanding debt obligations. These exercises aim to optimize capital structure, improve liquidity, reduce interest costs, and avoid distress by modifying bond terms or buying back debt. Liquidity:

On-balance sheet liabilities are direct, recorded obligations (debts, accounts payable) appearing on a company’s balance sheet, impacting leverage and financial ratios directly.

Off-balance sheet liabilities are potential or indirect obligations (leases, guarantees, joint ventures) not recorded on the balance sheet but disclosed in notes, used to manage risk or hide leverage.

Rollover risk (or refinancing risk) is the possibility that a borrower cannot refinance or replace maturing debt with new debt under favourable terms, or at all. It often arises when short-term debt must be paid off with new, costlier debt during unfavourable market conditions, such as high interest rates, liquidity squeezes, or a decline in investor confidence.

Short-dated securities are those due for early payment or redemption.

Sovereign fundamentals are the core economic, financial, and political metrics determining a government’s creditworthiness and capacity to meet its debt obligations. They evaluate a country’s ability to pay, primarily focusing on GDP growth, fiscal balance (debt-to-GDP ratio), tax revenue, inflation, political stability, and foreign currency reserves. Structural reform:

Sustainability-linked bonds (SLBs) are general-purpose, forward-looking debt instruments that tie financial or structural characteristics—such as coupon rates—to the issuer’s achievement of predefined Sustainability/ESG objectives. Unlike green bonds, proceeds are not ring-fenced for specific projects. If targets (SPTs) are missed, a penalty (e.g., a coupon step-up) usually applies.

Volatility: The rate and extent at which the price of a portfolio, security, or index, moves up and down. If the price swings up and down with large movements, it has high volatility. If the price moves more slowly and to a lesser extent, it has lower volatility. The higher the volatility, the higher the risk of the investment.

These are the views of the author at the time of publication and may differ from the views of other individuals/teams at Janus Henderson Investors. References made to individual securities do not constitute a recommendation to buy, sell or hold any security, investment strategy or market sector, and should not be assumed to be profitable. Janus Henderson Investors, its affiliated advisor, or its employees, may have a position in the securities mentioned.

Past performance does not predict future returns. The value of an investment and the income from it can fall as well as rise and you may not get back the amount originally invested.

The information in this article does not qualify as an investment recommendation.

There is no guarantee that past trends will continue, or forecasts will be realised.

Marketing Communication.