Inflation: is this the real thing? Is this just fantasy?…

John Pattullo, Co‑Head of Strategic Fixed Income, explains why an expected and predictable cyclical reflation should not be confused with a longer-term structural breakout of inflation.

2 minute read

Key takeaways:

- As we head into the spring and summer of 2021 and escape the pandemic lockdown, we expect to see a rise in both core and headline inflation.

- What could be quite a large cyclical bounce back in ‘revenge’ spending, however, should be distinguished from all the other long‑term structural factors that explain why we live in a low growth and low inflation economy.

- The way central banks might react to this inevitable short‑term, cost‑push inflation will be fascinating and will throw up threats and opportunities for all investors.

As we navigate our way through the COVID‑19 crisis, people have started to worry about inflation once again. A couple of years ago I wrote that the Phillips Curve – a useful gauge for inflationary pressures in an economy and used by central banks in setting policy – has broken (Broken curves: are misguided inflation measures leading to policy mistakes?). Back in June 2020, I wrote So… what about inflation? What follows is an update of our thoughts on inflation as we see it, in the Strategic Fixed Income team.

Visible signs of a ‘bottleneck’ reflation

Nearly ten months into the COVID‑19 crisis, we are moving from the disinflationary demand shock, first stage, towards the cyclical recovery ‘bottleneck’ reflation, second stage. Now, an expected and predictable cyclical reflation should not be confused with a longer term structural breakout of inflation and inflation expectations. This confusion presents opportunities and threats for investors, but headaches for central bankers.

As we head into the spring and summer of 2021 and escape the pandemic lockdown, we expect to see a rise in both core and headline inflation. This is driven by the cyclical rebound in activity; as the economies reflate and people, once again, go outside and start spending and living (yippee!).

We expect this will be more of a cost‑push inflation (bad or tax-like inflation), driven primarily by bottlenecks in production. In a nutshell, the rate of change in demand may, for a short time, outstrip the rate of change in output. Inventory levels are currently low and tight because of the lockdown, and it will take time to rebuild.

Just look at copper or lumber prices. “Dr Copper” is at a 6‑year high (see figure 1) while lumber is in short supply given the strength of the US housing market. Further, if we all start flying again, aviation fuel supply cannot be switched on overnight. When I went to fill my car up for the fourth time this year, the petrol station was desolate, but this can all change very quickly. Consumption patterns will, to some degree, revert back to what they were; fewer exercise bikes and patio heaters and more sun cream and holidays.

Figure 1: Dr Copper is at a 6‑year high

copper, cash, US dollar; cash prices at the end of LME day</small>

</div>

<p>As Simon Ward, our economic adviser, has pointed out, the inventory cycle has bottomed; as has the capital expenditure (capex) cycle, while we are roughly half way in a long running housing cycle. In addition, we obviously have super loose monetary and fiscal policy.</p>

<p>In a reflationary period you would expect commodities to motor, the yield curve to steepen, bond yields to rise, the dollar to weaken and value/cyclical stocks to (at last!) outperform growth. As we often say, “live in growth, but holiday in value”. Well, it’s holiday time but they never last long enough. For this reason we have a lot of fairly short‑dated, ‘yieldy’ corporate bonds (bonds with reasonably high yields) in our funds and have hedged some of the interest rate risk – most unusual for myself and my co-head, Jenna Barnard; since we are, after all, card carrying secular stagnation-ists!</p>

<p>The point being: always distinguish a cyclical trade from a structural one; frankly in all aspects of investing (or even life) but especially in credit selection, as per our ‘sensible income’ mantra and, obviously, in interest rate management.</p>

<h2 class=) Don’t rock with the ‘headline’ swings

Don’t rock with the ‘headline’ swings

The other point on inflation is of course, that the headline number swings around – a lot – due to the oil price. We had a negative oil price in April, so when this drops out of the 12‑month rolling number, ceteris paribus, the price will rise. Do the math! I look forward to CNBC commentators telling us we have a break out of inflation in the summer.

A weak dollar also tends to raise the price of imported goods for Americans and is generally reflationary for the world. In addition, with the lockdown, the constituents of the inflation numbers have moved around; namely, second hand car prices and shelter (housing costs) in the US calculation.

In Europe, the inflation outlook is, as ever, more benign and lower than the US, but still at the mercy of base effects. Figure 2 shows the market’s expectations for inflation in the second half of the next decade, in Europe and the US. The levels are still benign in both regions.

Figure 2: Inflation expectations in the US and Europe

Source: Bloomberg, Janus Henderson Investors, as at 15 December 2020

Note: 5-year, 5-year forward inflation swap rates in the US and Europe. A common measure used to look at the market’s future inflation expectations.

We actually think the bounce back could be quite violent. Australia and New Zealand both seem to be bouncing quite hard. The massive growth in the money supply has been well flagged, but until recently has been offset by a collapse in the velocity of circulation1 as the savings ratio has ballooned. In the US, the savings ratio rose to 33.7% in April, but fell back to 13.6% in October (a more normal level is around 8%). There are trillions of dollars of pent‑up spending ready to go.

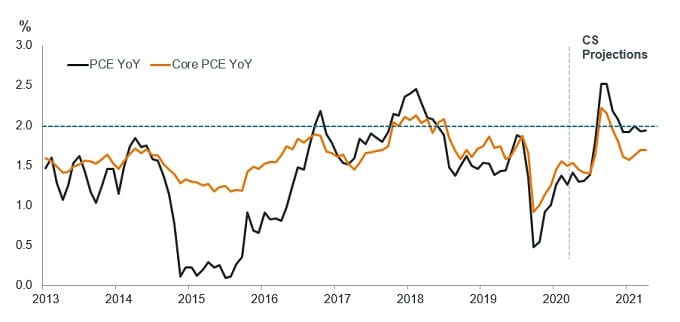

This is where it gets interesting for bond managers, confusing for market commentators and, tough for central bankers. The US Federal Reserve has publicly stated that it will let the economy run hot (Janet Yellen also said this years ago, but failed). By doing so, it hopes to lower the unemployment rate and the output gap with its latest policy innovation of symmetrical inflation targeting. Figure 3 shows the actual personal consumption expenditure (PCE) inflation in the US over the last few years, with forecasts for 2021 by Credit Suisse.

Figure 3: Core and headline PCE inflation in the US – expect volatility ahead

Source: Credit Suisse, Janus Henderson Investors, as at 8 December 2020

We must try to distinguish what could be quite a large cyclical bounce back in ‘revenge’ spending from all the other long‑term structural factors that explain why we live in a low growth and low inflation economy. In other words, some people may confuse short‑term, bottleneck, cost‑push, price volatility, imported inflation, with demand‑pull inflation. The latter being where prices are pulled up permanently due to a lack of goods, services, capital or labour. In a demand‑pull situation, people would demand higher wages due to the scarcity of labour, in order to afford more expensive goods in the shops. The price of capital – interest rates – would or should, then rise to dampen the excess demand, in a classic 1970s upward price spiral.

So… where are we with inflation now?

We continue to think that the demand-pull scenario is highly unlikely, given all the experience we have gained observing growth and inflation dynamics in both Japan and Europe. Further, as I wrote in my previous article in June, there remains the threat of a regime change with the adoption of modern monetary policy (MMT)2-type strategies (though given the recent US election result, we sense this risk has somewhat faded). However, we continue to live in a world of increasing financial repression3, with negative real yields, which will become increasingly challenging for all of us.

Thus, we remain long of credit risk and short of government/interest rate risk. The way central banks might react to the inevitable ‘bad’, cost‑push inflation, will be fascinating and will throw up threats and opportunities for all investors. We remain flexible in our thinking and in the meantime stick to our core sensible income strategy while being wary of a cyclical reflationary surge, but only for a while…

Keep an eye on the equity rotation trade, commodity prices, the US dollar (the ultimate tell) and inflation expectations to see how long this trade lasts. Remember, try not to confuse a shorter‑term cyclical reflationary impulse with a continued disinflationary structural backdrop.

We would like to thank all our clients for their continued support and hope for a less eventful 2021! Merry Christmas!

1Velocity of circulation (of money): the frequency at which one unit of currency is used to buy goods and services within a given time period. In other words, it is the number of times one dollar is spent to buy goods and services per unit of time.

2Modern Monetary Theory (MMT): an unorthodox approach to economic management, which in simple terms argues that countries that issue their own currencies can ‘never run out of money’ the way people or businesses can.

3Financial repression: in simple terms, using regulations and policies to force down interest rates below the rate of inflation; also known as a stealth tax that rewards debtors but punishes savers.

These are the views of the author at the time of publication and may differ from the views of other individuals/teams at Janus Henderson Investors. References made to individual securities do not constitute a recommendation to buy, sell or hold any security, investment strategy or market sector, and should not be assumed to be profitable. Janus Henderson Investors, its affiliated advisor, or its employees, may have a position in the securities mentioned.

Past performance does not predict future returns. The value of an investment and the income from it can fall as well as rise and you may not get back the amount originally invested.

The information in this article does not qualify as an investment recommendation.

Marketing Communication.

Important information

Please read the following important information regarding funds related to this article.

- An issuer of a bond (or money market instrument) may become unable or unwilling to pay interest or repay capital to the Fund. If this happens or the market perceives this may happen, the value of the bond will fall.

- When interest rates rise (or fall), the prices of different securities will be affected differently. In particular, bond values generally fall when interest rates rise (or are expected to rise). This risk is typically greater the longer the maturity of a bond investment.

- The Fund invests in high yield (non-investment grade) bonds and while these generally offer higher rates of interest than investment grade bonds, they are more speculative and more sensitive to adverse changes in market conditions.

- Some bonds (callable bonds) allow their issuers the right to repay capital early or to extend the maturity. Issuers may exercise these rights when favourable to them and as a result the value of the Fund may be impacted.

- If a Fund has a high exposure to a particular country or geographical region it carries a higher level of risk than a Fund which is more broadly diversified.

- The Fund may use derivatives to help achieve its investment objective. This can result in leverage (higher levels of debt), which can magnify an investment outcome. Gains or losses to the Fund may therefore be greater than the cost of the derivative. Derivatives also introduce other risks, in particular, that a derivative counterparty may not meet its contractual obligations.

- When the Fund, or a share/unit class, seeks to mitigate exchange rate movements of a currency relative to the base currency (hedge), the hedging strategy itself may positively or negatively impact the value of the Fund due to differences in short-term interest rates between the currencies.

- Securities within the Fund could become hard to value or to sell at a desired time and price, especially in extreme market conditions when asset prices may be falling, increasing the risk of investment losses.

- Some or all of the ongoing charges may be taken from capital, which may erode capital or reduce potential for capital growth.

- CoCos can fall sharply in value if the financial strength of an issuer weakens and a predetermined trigger event causes the bonds to be converted into shares/units of the issuer or to be partly or wholly written off.

- The Fund could lose money if a counterparty with which the Fund trades becomes unwilling or unable to meet its obligations, or as a result of failure or delay in operational processes or the failure of a third party provider.

Specific risks

2 minute read

Key takeaways:

- As we head into the spring and summer of 2021 and escape the pandemic lockdown, we expect to see a rise in both core and headline inflation.

- What could be quite a large cyclical bounce back in ‘revenge’ spending, however, should be distinguished from all the other long‑term structural factors that explain why we live in a low growth and low inflation economy.

- The way central banks might react to this inevitable short‑term, cost‑push inflation will be fascinating and will throw up threats and opportunities for all investors.