Key takeaways:

- Declining launch costs and technical progress have made commercial space businesses more economically viable, creating diverse investment opportunities across communications, defense, and infrastructure sectors.

- Space investments offer compelling growth potential, but higher risk profiles and longer development timelines require selective stock picking and patience.

- In our view, three keys to investing in space are identifying companies with demonstrable technical progress and clear commercial plans, diversifying across the value chain, and guarding against execution risk.

2025 has been a landmark year for space companies. Major developments and key announcements across lunar missions, satellite deployments, interplanetary exploration, and national security contracts have pushed space-related investments into the spotlight.

We have also seen a strong push toward increased commercialization and investment in space infrastructure. Major telecom carriers are partnering with space companies to enable cell phone coverage in remote areas, the Department of Defense is accelerating next-generation missile defense programs, and commercial companies are competing to build the next generation of space stations.

For investors, this creates compelling growth opportunities. But in contrast to traditional aerospace, which offers exposure to growth in global air travel and steady demand for aircraft maintenance and parts, the space economy is an emerging category with its own characteristics and risk-return considerations. Companies linked with space encompass a range of activities in orbit and beyond – from launch services and satellites to in-space infrastructure and a growing set of commercial applications.

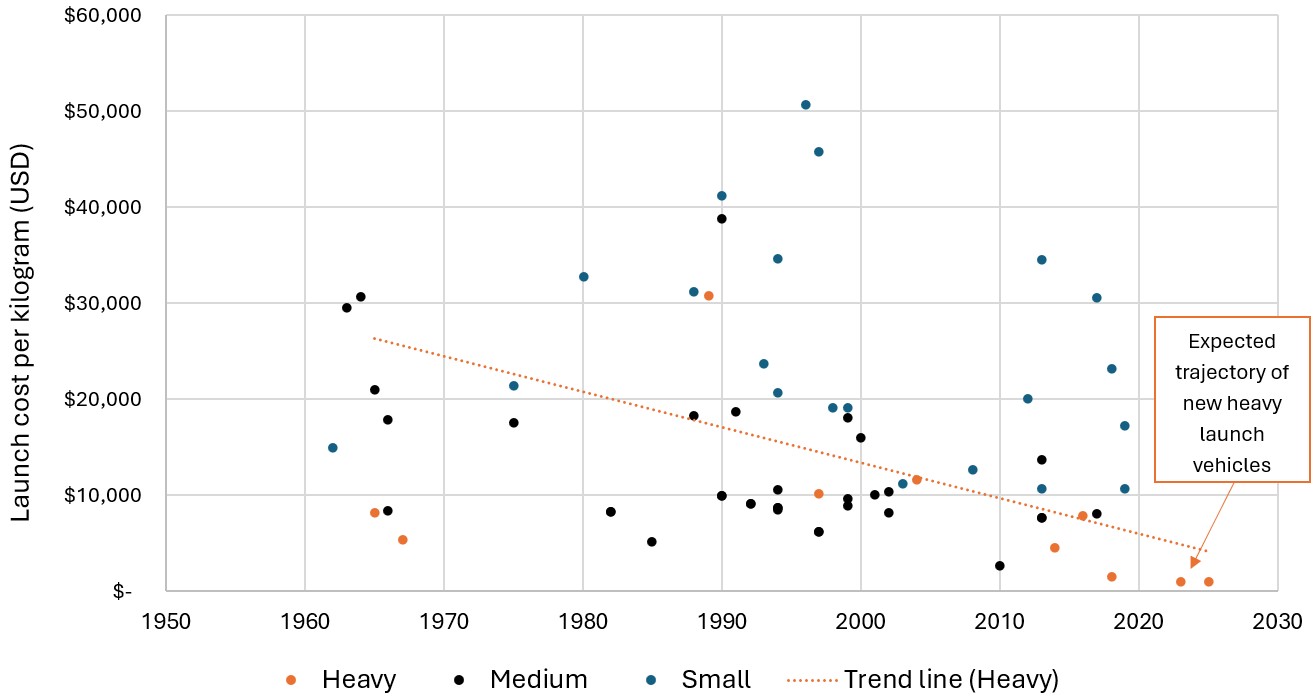

Declining launch costs change the economics

For decades, the space domain belonged almost exclusively to governments as business models were too capital-intensive to make commercial sense. Commercial space investment became more feasible only recently, thanks to a dramatic shift in launch economics.

The cost to launch cargo into orbit has dropped roughly 97% since the mid-2000s. Companies like SpaceX pioneered reusable rockets, while increased competition from launch providers such as Rocket Lab, Blue Origin, and Firefly further transformed the economics. This cost deflation has fundamentally altered what commercial space business could achieve.

The impact extends across the entire value chain. Previous business models that failed in earlier decades are now more feasible, creating investment opportunities across multiple sectors including communications, defense, manufacturing, and services.

Figure 1: Launch costs by year based on payload size

Launch costs to low Earth orbit have dropped.

Source: CSIS Aerospace Security Project (2022), Our World in Data, JHI estimates. Cost to launch one kilogram of payload mass to low Earth orbit as part of a dedicated launch. This data is adjusted for inflation.

Three emerging growth drivers

Satellite communications

Companies are developing and launching low-orbit satellites to provide mobile phone coverage in areas without terrestrial cell networks, using new technology that works with unmodified smartphones. Major carriers plan to offer satellite coverage options to customers traveling beyond traditional coverage areas.

Earlier attempts at satellite communications proved excessively expensive: One company in the 1990s spent $7 billion building its network before going bankrupt. Current systems can achieve better capabilities for approximately $2 billion. While still substantial that cost is far more feasible, especially given a potential market of 3 billion subscribers through partnerships with 50 mobile carriers globally.

These developments also raise questions about the broader wireless and telecom infrastructure landscape. If satellite-based services that connect directly to phones (called Direct-to-Cell) become strong enough, it is possible they could compete with traditional wireless networks, especially in rural areas. While Direct-to-Cell service products may face limitations indoors or in dense urban areas, they could limit the opportunity for tower companies to extend traditional coverage into hard-to-reach places.

Defense and national security

Space has become increasingly important for national security. The rise of hypersonic missiles – which travel five times the speed of sound while maneuvering – requires new space-based defense systems.

In the U.S., the Next Generation Interceptor Program includes companies developing guidance systems that help defense missiles track and intercept maneuverable threats, addressing a critical gap in current capabilities.

Military planners also worry about satellite vulnerabilities such as GPS jamming creating demand for resilient communication systems and GPS alternatives.

Importantly, Congress has shown bipartisan support for space initiatives, partly driven by competition with China’s space program, providing relatively stable funding for defense-related ventures.

Future infrastructure

The next decade is poised to be the most active in space since the Apollo program. This includes replacement of the International Space Station in the 2030s, with commercial companies developing alternatives and NASA expected to award contracts next year. These projects represent significant capital commitments but have identifiable revenue streams through government contracts and commercial research.

Also, NASA’s Artemis program plans to return humans to the moon, with the first mission scheduled for February 2026. While exploration programs are primarily government funded without immediate commercial returns, they drive technology development and create opportunities for suppliers and service providers.

Can the company execute? The importance of deep research

While the thematic drivers are powerful, we believe success in the space sector requires deep research and a selective approach focused on companies with sustainable advantages and executable plans.

Execution risk looms large: Space programs are notoriously complex, and companies routinely face technical hurdles that push projects behind schedule and over budget. Technical risk is inherent to operating in space, bringing constant danger of launch anomalies or satellite malfunctions. Additionally, a significant portion of the current revenue stream, particularly in defense and exploration, is tied to government budgets, introducing political and budgetary risk.

When evaluating companies, we think research should extend beyond financial models and valuation analysis. It is important to get to know the management team and understand their incentives and track record for execution, pressing them on potential failure points and challenging business model assumptions.

To that end, we try to build a complete picture by speaking with experts, customers, and partners throughout the value chain, leveraging collaborative research that brings together different analytical perspectives. Our team’s industrial and communications sector expertise is valuable for understanding cross-disciplinary technologies. We also conduct on-the-ground verification whenever possible, visiting manufacturing sites and operational facilities to gain context that financial statements alone cannot provide.

Taylor Portman (right) visits NASA’s Houston facility with ex-astronaut Tim Kopra, exploring the Russian module mockup of the ISS.

Looking ahead

The space economy has reached an inflection point where it is transitioning from a governmental endeavor to a commercially viable frontier. We expect the opportunity set to grow if launch and component costs continue to fall. Private capital remains active across many parts of the ecosystem, and we expect more companies to reach public markets if financing conditions permit.

Going forward, we are monitoring program execution, satellite scale and interoperability, government funding cycles, and how companies demonstrate a path to profitability. We favor opportunities where technical progress aligns with a clear commercial path, while guarding against execution and geopolitical risks.

Aerospace and defense industries can be significantly affected by changes in the economy, fuel prices, labor relations, and government regulation and spending.

These are the views of the author at the time of publication and may differ from the views of other individuals/teams at Janus Henderson Investors. References made to individual securities do not constitute a recommendation to buy, sell or hold any security, investment strategy or market sector, and should not be assumed to be profitable. Janus Henderson Investors, its affiliated advisor, or its employees, may have a position in the securities mentioned.

Past performance does not predict future returns. The value of an investment and the income from it can fall as well as rise and you may not get back the amount originally invested.

The information in this article does not qualify as an investment recommendation.

There is no guarantee that past trends will continue, or forecasts will be realised.

Marketing Communication.