Key takeaways:

- The Iran War has caused a rapid repricing in interest rates due to inflation fears, but a different environment to 2022, particularly a softer labour market, suggests aggressive central bank tightening may not be required.

- Rising yields and modestly wider credit spreads have improved income opportunities, creating more attractive entry points for fixed income investors.

- Higher oil prices may trim global growth modestly given reduced energy sensitivity, but companies will be affected differently, favouring selective and actively managed credit exposure.

The reaction of fixed income markets to the Iran War evolved as the conflict progressed. What started as inflation fears brought on by a steep rise in oil and gas prices morphed into concerns that tighter financial conditions could stymie economic growth. This has manifested itself through a rise in rate expectations, together with a widening – albeit modest – of credit spreads. For investors looking for income, could the repricing of yields offer an opportune time to add fixed income exposure?

Market overshoot?

What has been remarkable has been the speed and quantum of the central bank policy interest rate repricing. Within just six weeks, the market went from expecting two rate cuts of 25 basis points each in the US to none, two rate cuts in the UK to two hikes, and potentially one rate cut for the eurozone to two hikes.1

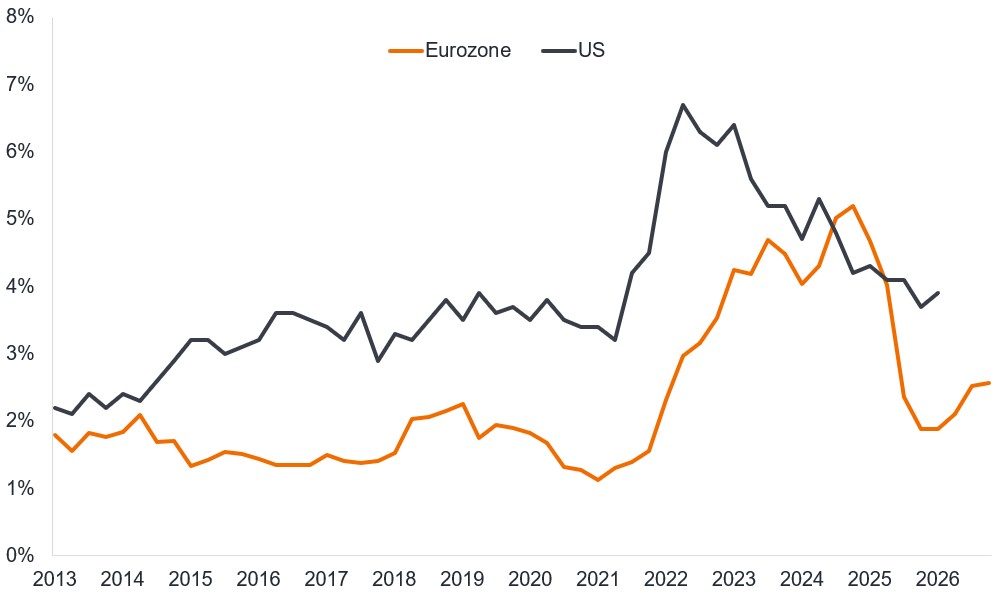

While mindful that central banks need to be ready to act, it is not clear at this juncture that the priced rate hikes will be required. While acknowledging that inflation is likely to be higher than initially expected, there are meaningful differences to a backdrop such as 2022, when a rebound in economies reopening after the Covid lockdowns coincided with higher energy prices due to the Ukraine war. Most notably, the different position of the labour market, which is much more fragile today compared with 2022. Wage expectations so far have been well behaved as have longer-term inflation expectations.

Eurozone and US wage tracker (y-o-y growth)

Source: Eurozone: ECB Wage Tracker (forward-looking wage growth from March 2013 to end December 2026 using wage agreements signed up to end February 2026); US: Atlanta Fed Wage Growth Tracker (change in hourly wage of individuals observed 12 months apart, three month moving average, from March 2013 to March 2026).

Higher yields

The upward shift in rate expectations has seen yields rise globally. In the US, the rise in yields is reflected across the economy, with mortgage rates climbing and financial conditions tightening. In part, this could help stay the hand of the US Federal Reserve (Fed), which has a dual mandate (price stability and full employment). The Fed may, therefore, look through any short-term inflation caused by higher oil prices and keep rates on hold to help the consumer.

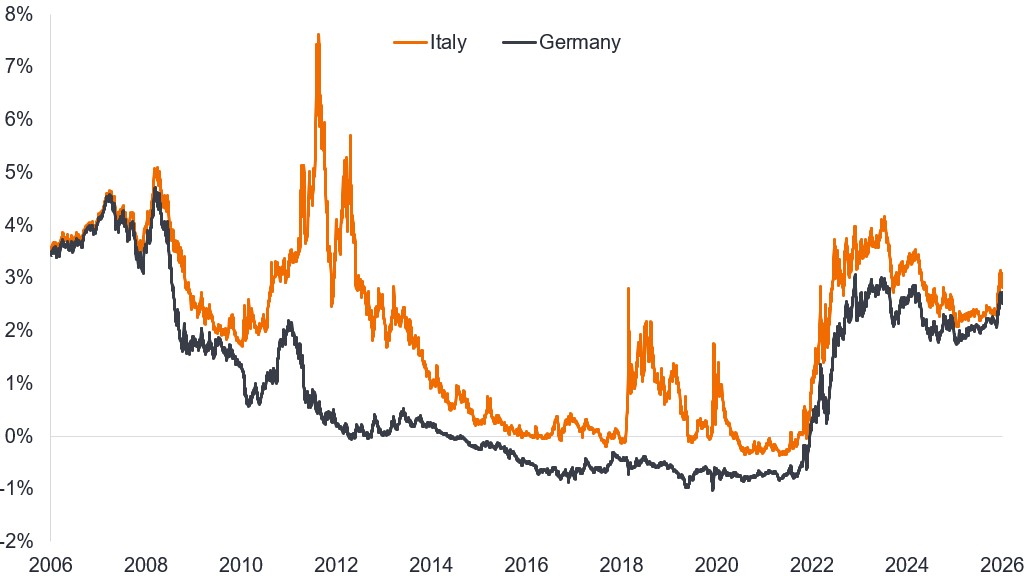

For the European Central Bank (ECB), which is more constrained by its inflation-targeting mandate, the risk of higher rates is more prevalent, but this would appear to already be reflected in the rise in yields across government bonds. Looking at three-year Italian and German government bonds, yields have climbed about 0.6% since the Iran War started on 28 February 2026.

Yields on 3-year government bonds

Source: Bloomberg, yield on generic 3-year Italian government bond and 3-year German government bond, 10 April 2006 to 10 April 2026. Yields may vary overtime and are not guaranteed.

What is notable is how closely Italian yields have been tracking German yields recently. Italian government bond yields were 23 basis points (0.23%) higher than German yields at the outbreak of the Iran war. By 10 April that had climbed to 32 basis points (0.32%). Concerns that once weighed on Italian debt have faded as fiscal discipline has seen Italy’s annual government deficit decline from more than 7% of gross domestic product (GDP) in 2023 to 3.1% in 2025, a shade above the eurozone target of 3%.2 This makes Italian debt a less volatile asset class than it has been for more than a decade.

Spread sensitivity

Coupled with the rate moves globally, there has been a modest widening of spreads across both physical corporate bonds and credit default swaps (CDS) since the Iran war started. The former reflects investors demanding more in terms of yield compensation for taking on the credit risk of investing in corporate bonds, while the latter reflects a higher cost to insure against default risk. The moves have been orderly, however, as markets continue to price in a short conflict rather than a protracted war. For example, credit spreads on investment grade shorter-dated 1-3 year BBB rated Euro corporate bonds have widened by 5 basis points, while on BB-B rated Euro high yield bonds, they have widened by 24 basis points.3 There had also been some widening prior to the war on concerns around artificial intelligence (AI) displacement, private credit worries, and volatility around tariffs, which may explain why credit markets have been relatively sanguine to date.

High oil prices raise costs for most businesses and depress real incomes, potentially slowing the economy. The sensitivity of economies to oil price shocks has diminished, however, since the 1960/70s. Bank of America (BofA) estimates that a 10% rise in the oil price shrinks US growth by around 5 basis points (bps) or 0.05%. The Eurozone is more sensitive, with a 10% rise in oil prices shaving 10bps (or 0.1%) off Eurozone growth. Oil prices have risen about 50-60% since the war started, so BofA cut its forecast for global growth in 2026 from 3.5% to 3.1%.4 Moderate economic growth should still allow earnings to grow in 2026.

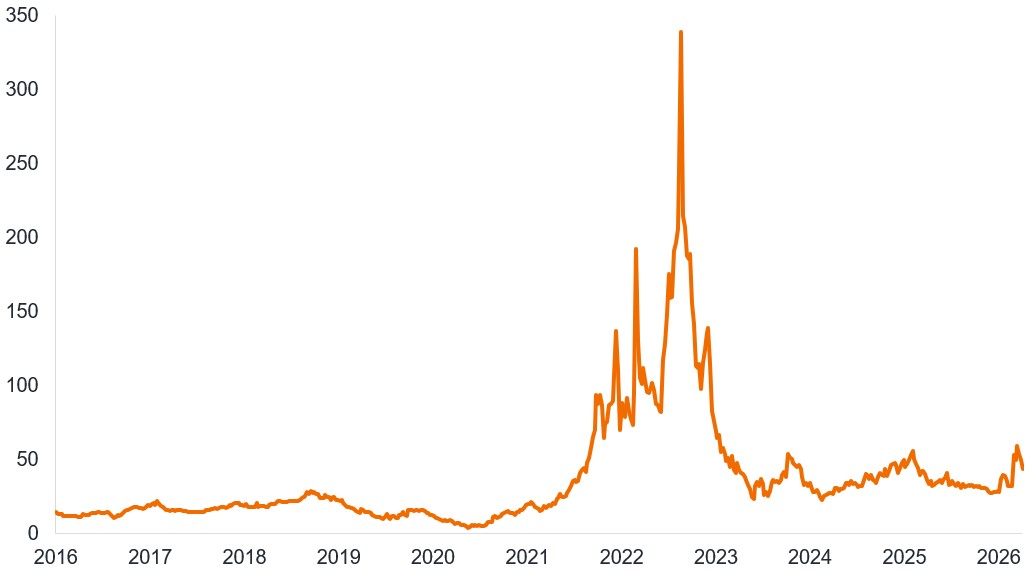

There is, however, likely to be a redirection of cash flows, with sectors such as energy gaining at the expense of sectors where oil and gas are a large input cost or consumption is more discretionary. While mindful that the reduction in maritime traffic through the Strait of Hormuz is likely to have an adverse impact on chemicals, plastics and fertilizers for several quarters, the supply disruption to European energy markets today is less severe than that of 2022 as reflected in European gas prices. It is important that the disruption is put into context.

European gas prices are far below 2022 levels (€/MWh)

Source: Bloomberg, ICE Endex Dutch Natural Gas Futures Contract, Euros per megawatt hour, 1 January 2016 to 10 April 2026.

Conclusion

In our view, spread entry points on credit default swaps have cheapened more on technical/macroeconomic reasons rather than company-specific factors. This creates opportunities for active managers to select credits that appear fundamentally strong and avoid those that are more exposed to downside risks. Together with the rise in front-end bond yields, this has led to an arguably more attractive income profile available today than was possible back in February. We are not convinced that all the rate hikes priced in by the market will take place, which means that investors prepared to invest now may be able to take advantage of elevated yields.

1Source: Bloomberg, world interest rate projections, as at 27 February 2026 and 10 April 2026.

2Source: Bloomberg, Istituto Nazionale di Statistica, General government net borrowing in 2022 and 2025, 2 March 2026.

3Source: Bloomberg, ICE BofA 1-3 Year BBB Euro Corporate Index, ICE BofA BB-B Euro High Yield Index, option-adjusted spreads over government bonds, 27 February 2026 to 10 April 2026.

4Source: BofA Global Research, Global Economic Viewpoint, 7 April 2026.

Fixed income securities are subject to interest rate, inflation, credit and default risk. The bond market is volatile. As interest rates rise, bond prices usually fall, and vice versa. The return of principal is not guaranteed, and prices may decline if an issuer fails to make timely payments or its credit strength weakens.

High-yield or “junk” bonds involve a greater risk of default and price volatility and can experience sudden and sharp price swings.

Derivatives can be more volatile and sensitive to economic or market changes than other investments, which could result in losses exceeding the original investment and magnified by leverage.

Basis point (bp): Equals 1/100 of a percentage point, 1bp = 0.01%, 100bps = 1%.

Cash flow: The movement of cash from one party to another.

Corporate bond: A bond issued by a company. Bonds offer a return to investors in the form of periodic payments and the eventual return of the original money invested at issue on the maturity date.

Credit Default Swaps (CDS): Derivatives that enable an investor to swap or offset their credit risk (the risk that a borrower defaults on meeting its repayment obligations). It allows the transfer of credit risk from one counterparty to another. Buyers of CDS pay a premium to sellers of CDS who are obliged to make the buyer whole again if the bond defaults. If the bond does not default, the CDS has collected the premium without having to pay out.

Credit rating: An independent assessment of the creditworthiness of a borrower by a recognised agency such as S&P Global Ratings, Moody’s or Fitch. Standardised scores such as “AAA” (a high credit rating) or “B” (a low credit rating) are used, although other agencies may present their ratings in different formats. BB, B and CCC are high yield ratings in declining order of creditworthiness.

Credit spread: The difference in yield between securities with similar maturity but different credit quality. It often refers to the difference in yield between a corporate bond and government bond of similar maturity. Widening spreads generally indicate deteriorating creditworthiness of corporate borrowers, and narrowing indicate improving.

Creditworthiness: A measure of a borrower’s ability and willingness to repay their debts. A company with high creditworthiness is seen as safer to lend to while low creditworthiness signals higher risk.

Default: The failure of a debtor (such as a bond issuer) to pay interest or to return an original amount loaned when due.

Derivative: A financial instrument for which the price is derived from one or more underlying assets such as shares, bonds, commodities, or currencies. It is a contract between two or more parties which allows investors to take advantage of price movements in the asset(s).

Fundamentals: The underlying financial and operational factors, such as profitability, cash flow and management quality, that indicate a company’s ability to meet its financial obligations.

High yield bond: Also known as a sub-investment grade bond, or ‘junk’ bond. These bonds usually carry a higher risk of the issuer defaulting on their payments, so they are typically issued with a higher interest rate (coupon) to compensate for the additional risk.

Investment grade bond: A bond typically issued by governments or companies perceived to have a relatively low risk of defaulting on their payments, reflected in the higher rating given to them by credit ratings agencies.

Maturity: The maturity date of a bond is the date when the principal investment (and any final coupon) is paid to investors. For a CDS, the maturity date is the last date of the contract’s term.

Megawatt-hour (MWh): A megawatt-hour is a representation of energy (1,000,000 watts) delivered over a period of one hour. For context, a single MWh of energy could run two 60-watt lightbulbs for approximately one year.

Yield: The level of income on a security over a set period, typically expressed as a percentage rate. For a bond, at its most simple, this is calculated as the coupon payment divided by the current bond price.

Volatility: A measure of risk using the dispersion of returns for a given investment. The rate and extent at which the price of a portfolio, security or index moves up and down.

These are the views of the author at the time of publication and may differ from the views of other individuals/teams at Janus Henderson Investors. References made to individual securities do not constitute a recommendation to buy, sell or hold any security, investment strategy or market sector, and should not be assumed to be profitable. Janus Henderson Investors, its affiliated advisor, or its employees, may have a position in the securities mentioned.

Past performance does not predict future returns. The value of an investment and the income from it can fall as well as rise and you may not get back the amount originally invested.

The information in this article does not qualify as an investment recommendation.

There is no guarantee that past trends will continue, or forecasts will be realised.

Marketing Communication.