Key takeaways:

- The eruption of hostilities in the Middle East sent global crude prices higher as the market priced in considerable uncertainty.

- Even if the region’s energy assets remain online, any reduction in shipping activity through the Strait of Hormuz could lead to sustained higher energy prices.

- Perhaps reflecting an otherwise soft energy market, crude oil futures have yet to signal a continual rise in energy prices over mid- to longer-term horizons.

The initiation of a potentially sustained joint U.S.-Israeli air campaign against Iran has again forced investors to focus on how regional conflict – especially with respect to the Strait of Hormuz, a critical energy transportation bottleneck – can impact global energy markets.

Above all, we are monitoring any signs of disruption in oil production and/or exports. While both Brent and West Texas Intermediate benchmarks rose on news of hostilities, prices are well beneath their initial spike, with Brent trading at roughly $78/barrel on the afternoon of March 2, 2026. Importantly, crude futures curves are not indicating the likelihood of constricted supply pushing up oil prices over longer horizons.

Should energy infrastructure both in Iran and across the Middle East not be targeted, we believe the market could again reflect what has largely been a relatively soft environment for global crude prices. But as with any geopolitical conflict, the situation remains highly unpredictable and merits extremely close monitoring.

What’s different this time

After an initial reaction, the market shrugged off last June’s air campaign against Iran’s nuclear infrastructure. The current episode is considerably different given the degree of escalation, the U.S.’s much higher level of involvement, fatalities within key Iranian leadership, and – perhaps most surprisingly – Iran’s retaliation against multiple Gulf countries.

The joint U.S.-Israeli offensive has targeted Iran’s leadership and defense capabilities. Meanwhile, Iran’s response has focused not only on U.S. military assets in the region but also civilian targets. Thus far, the region’s energy infrastructure has been spared. Even without direct attacks, however, global energy markets could be disrupted should Iran attempt to limit – or cut off – shipments through the Strait of Hormuz.

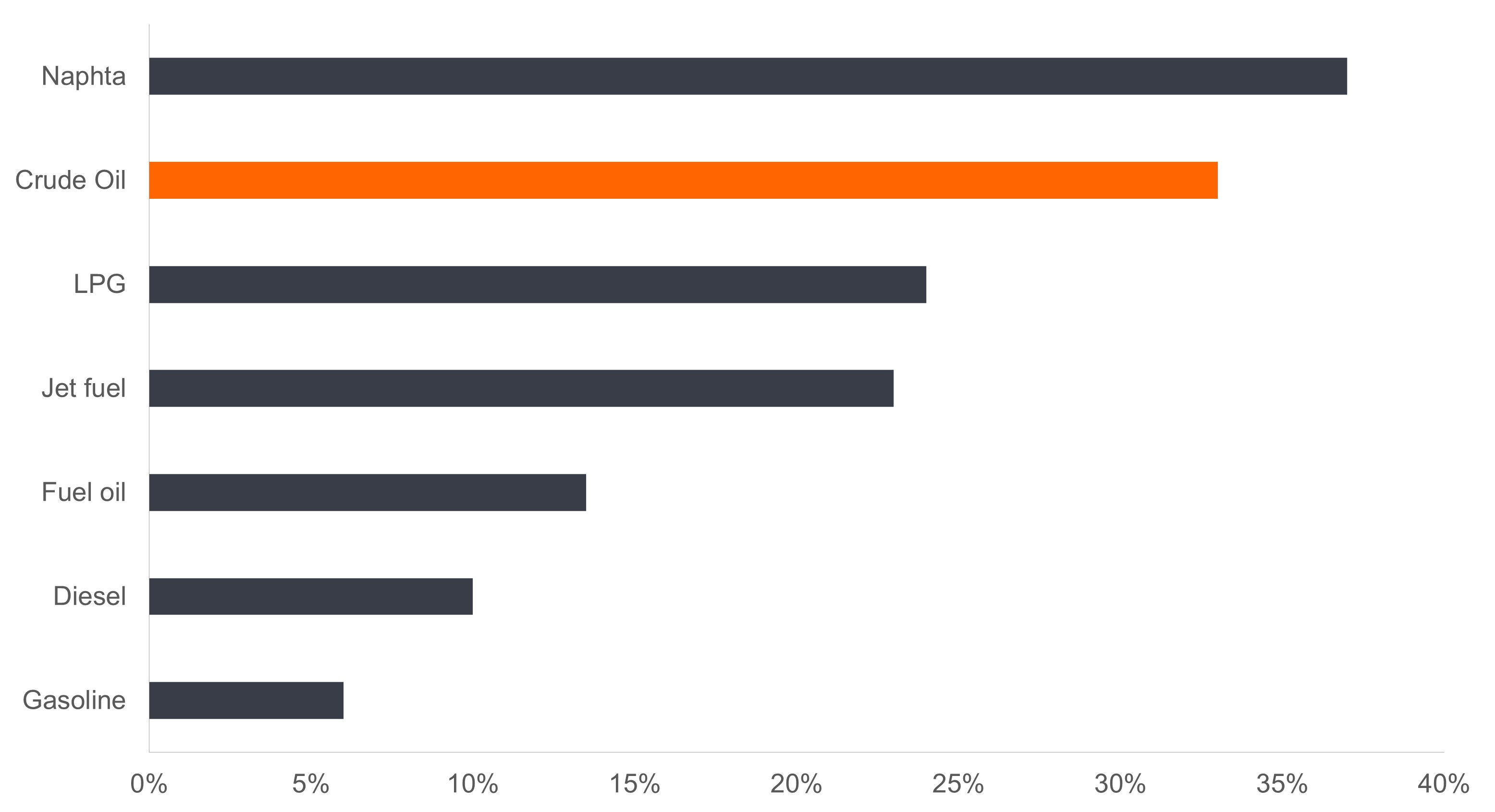

Share of global seaborne volumes transported through Strait of Hormuz in 2025

The roughly 30% of global crude – and different shares for other energy products – transported by sea that traverses the Strait of Hormuz represents a significant pinch point for the world’s energy market.

Source: Bloomberg, Janus Henderson Investors.

Up-to-date satellite data indicates that the volume of ships has slowed through the Strait. This, however, is not due to any attacks but rather the inability of many vessels to procure insurance given the volatile backdrop.

We believe access to the Strait of Hormuz is perhaps one of the best indicators for investors to watch in the coming days and weeks. Even if production and refining infrastructure remain intact, effective closure of the Strait could constrict global supply, as more than 25% of global seaborne oil trade and roughly 20% of global oil and petroleum product consumption must navigate this relatively narrow passage. And as intimated, it’s not only crude: A considerable volume of oil condensates and natural gas, mainly from Qatar, is exported from the region, with Asia being a top destination.

Rebalancing?

Even prior to this weekend’s escalation, OPEC+ had already signalled it would increase global supply perhaps as early as next month. In light of the conflict, this consortium of producers has announced an April supply increase of 206 thousand barrels per day, well above the 137 thousand daily barrels previously considered. Of course, should the Strait of Hormuz be closed, this increase would fail to reach global consumers.

Barring material disruptions within either production or transport, we believe global crude prices will likely continue to reflect what we consider to be relatively soft market dynamics. In 2024, the most actively traded Brent crude contracts averaged roughly $73 per barrel. In 2025, they averaged just under $66. Price declines would have likely been even more pronounced had it not been for China stockpiling crude. Any sustained price increase could not only curtail this activity but also entice China into being net sellers, thus dampening any market reaction to supply disruptions.

What to watch

In contrast to earlier attacks on Iranian assets, where the country’s response was both fairly limited and well telegraphed, the degree of this escalation makes the situation highly unpredictable. An attack on the oil infrastructure of the U.S.’s Gulf allies cannot be ruled out and would likely be met with a reciprocal assault on Iranian energy assets. The damage to global production under this remote but not unimaginable scenario could tilt the balance in global oil markets toward undersupply. Yet as stated, forward-looking futures prices are currently far from pricing in such an outcome.

Vigilantly positioned

Disruption in energy markets invariably reverberates across the global economy. We believe investors must acknowledge the headline risk but also not lose sight of maintaining a long-term view when allocating across a range of assets.

As the energy market finds itself in the middle of these developments, we believe investors should prioritize defensive positions such as large-cap integrated exploration and production companies, as well as midstream players. Many of these companies have a diversified set of assets that extend across geographies and products, thus dampening their exposure to the region and to global crude. Other energy companies operate in segments far removed from the Middle East or provide products and services that are highly regionalized and have company-specific catalysts that are less dependent on global hydrocarbon prices.

IMPORTANT INFORMATION

Commodities (such as oil, metals and agricultural products) and commodity-linked securities are subject to greater volatility and risk and may not be appropriate for all investors. Commodities are speculative and may be affected by factors including market movements, economic and political developments, supply and demand disruptions, weather, disease and embargoes.

Energy industries can be significantly affected by fluctuations in energy prices and supply and demand of fuels, conservation, the success of exploration projects, and tax and other government regulations.

BRENT – A blended crude stream oil sourced from the North Sea, known for its consistent quality and global trading price, which serves as a reference or “marker” for pricing a number of other crude streams.

Futures contracts are securities that enable market participants to buy or sell at asset at a specific future date at a price set by the market. Often these prices can signal future supply and demand of the underlying asset.

The Organization of the Petroleum Exporting Countries (OPEC+) is an organization enabling the co-operation of leading oil-producing and oil-dependent countries in order to collectively influence the global oil market and maximize profit.

West Texas Intermediate (WTI) is a high-quality North American crude oil and one of the three main global benchmarks of oil pricing. It is the second-most-traded oil benchmark, behind Brent crude, and is traded on the New York Mercantile Exchange.

A yield curve plots the yields (interest rate) of bonds with equal credit quality but differing maturity dates. Typically bonds with longer maturities have higher yields.

These are the views of the author at the time of publication and may differ from the views of other individuals/teams at Janus Henderson Investors. References made to individual securities do not constitute a recommendation to buy, sell or hold any security, investment strategy or market sector, and should not be assumed to be profitable. Janus Henderson Investors, its affiliated advisor, or its employees, may have a position in the securities mentioned.

Past performance does not predict future returns. The value of an investment and the income from it can fall as well as rise and you may not get back the amount originally invested.

The information in this article does not qualify as an investment recommendation.

There is no guarantee that past trends will continue, or forecasts will be realised.

Marketing Communication.