Key takeaways:

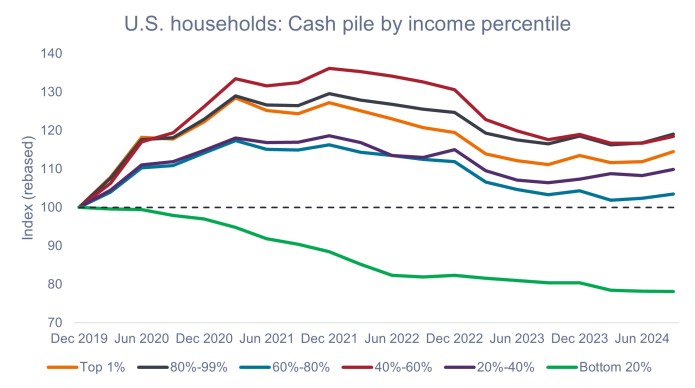

- While the bottom 20% of U.S. households might be more exposed to financial pressures, middle- and upper-income households – which represent a much larger portion of the overall economy – still have more cash on hand than before COVID.

- Middle- and upper-income households have also benefitted from stock portfolios and home values rising to all-time highs, low levels of unemployment, and wages that continue to grow well ahead of their pre-COVID rates.

- On the back of the strong consumer, we consider the risk of recession to be low in the U.S. and believe investors can continue to lean into attractive yields within high-quality consumer credit and securitized fixed income.

Source: JPM US Market Intelligence, Fed Z.1. The ‘consumer cash pile’ is defined as the combination of US households’ checkable deposits, savings deposits, and money market fund holdings. Index is adjusted for inflation using YE19 Consumer Price Index (CPI) as a base level.

In aggregate, the U.S. consumer – the bedrock of the U.S. economy – remains in good financial shape despite inflationary pressures and a softening labor market. Therefore, we believe the outlook for high-quality consumer credit and securitized fixed income remains upbeat. That said, as we witness a growing disparity in the financial strength of different market segments, it is important for investors to employ an active manager who may seek areas of strength and be selective about the types and quality of consumer credit they are exposed to.

– John Kerschner, Head of U.S. Securitized Products

IMPORTANT INFORMATION

Actively managed portfolios may fail to produce the intended results. No investment strategy can ensure a profit or eliminate the risk of loss.

Securitized products, such as mortgage- and asset-backed securities, are more sensitive to interest rate changes, have extension and prepayment risk, and are subject to more credit, valuation and liquidity risk than other fixed-income securities.

Fixed income securities are subject to interest rate, inflation, credit and default risk. The bond market is volatile. As interest rates rise, bond prices usually fall, and vice versa. The return of principal is not guaranteed, and prices may decline if an issuer fails to make timely payments or its credit strength weakens.

Related insights

Past performance is not a guide to future performance. The value of an investment and the income from it can fall as well as rise and you may not get back the amount originally invested.

The information in this article does not qualify as an investment recommendation.

For promotional purposes.

Anything non-factual in nature is an opinion of the author(s), and opinions are meant as an illustration of broader themes, are not an indication of trading intent, and are subject to change at any time due to changes in market or economic conditions. It is not intended to indicate or imply that any illustration/example mentioned is now or was ever held in any portfolio. No forecasts can be guaranteed and there is no guarantee that the information supplied is complete or timely, nor are there any warranties with regard to the results obtained from its us.