Key takeaways:

- Obesity-related health issues could cost up to 3–5% of global GDP by 2060, highlighting the urgent need for systemic change.

- The push for cleaner labels and ingredient transparency is driving innovation across multiple industries, beyond just food.

- Companies are shifting strategies, including M&A activity and product reformulations, to align with health-conscious consumer preferences and regulatory changes.

The rapid rise in GLP-1 weight loss drug adoption and heightened awareness of ultra-processed foods are redefining the discussion around consumer choices. Governments worldwide are waking up to the immense economic strain that obesity and chronic diseases place on healthcare systems. Social media and new technologies are empowering consumers with real-time product information and personalized feedback. Meanwhile, companies and investors are grappling with the impact of consumer-led disruption on strategy and capital allocation. Over the past two years, our Consumer and ESG Research teams have been monitoring the acceleration of these trends – and the conversation this time feels different.

The conscious consumer: trends, drivers and why this time feels different

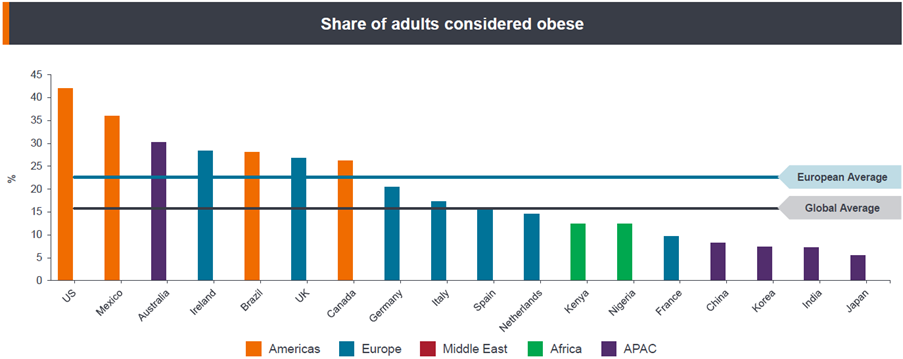

The global obesity crisis has reached a tipping point. Globally, the obesity rate has more than doubled since 1990 and over half of the world’s adult population is projected to be overweight or obese by 2050.1 In economic terms, obesity-related health issues are expected to cost up to 3–5% of global GDP by 2060, with links to more than 200 medical complications, including type 2 diabetes, cardiovascular conditions, and cancer.2.3 The US and UK bear the highest burden, with over 40% of US adults and 30% of UK adults classified as obese, costing their respective healthcare systems more than US$173 billion4 and £11.4 billion5 annually. When factoring in lost productivity, reduced quality of life, and other indirect societal costs, the total could exceed £74.3 billion/year in the UK and $1.4 trillion/year in the US.

Exhibit 1: Scale of the obesity crisis

Source: Janus Henderson research, WHO as at 8 December 2025.

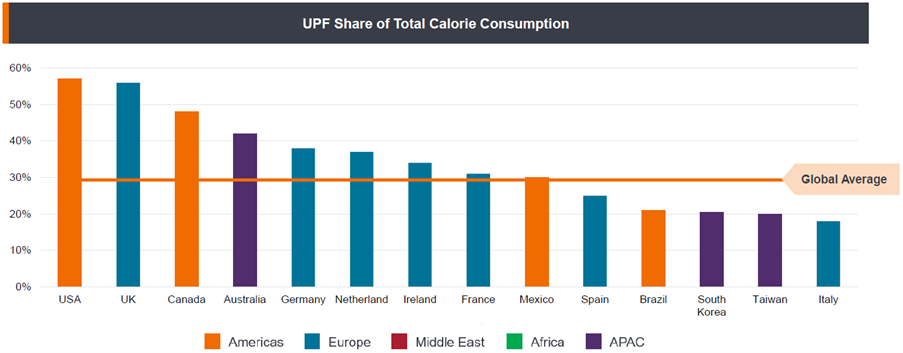

The food industry is increasingly being held accountable for engineering products that are hyper-palatable and addictive, contributing to rising rates of obesity and chronic illness. Ultra-processed foods (UPFs) – often high in sugar, salt, and synthetic additives – are designed to stimulate overconsumption and are aggressively marketed, especially to children. Public health experts argue that this business model prioritizes profit over wellbeing, with mounting evidence linking UPFs to excessive calorie intake, poor health outcomes, and broader dietary harm.6 While debates remain around the exact definition of the term, the prevalence cannot be ignored – UPFs account for more than half of the average daily calorie intake in both the US and UK (see Exhibit 2).

Exhibit 2: Ultra-processed foods are prevalent

Source: BMJ, Barclays Research, 2023.

The surge in publicity and rapid uptake of GLP‑1 medicines – best known today under brands such as Wegovy and Zepbound – has sharpened public focus on obesity as a systemic health challenge, not simply a matter of willpower, and accelerated debate over the food environment itself. These drugs show meaningful cardiometabolic benefits, in part by slowing gastric emptying and dampening reward-driven eating, leading to lower total daily calorie intake and reported changes in consumption habits. With less than 1% of people living with obesity globally treated with branded GLP-1s today, these drugs still have significant growth potential, especially as oral versions are introduced and the industry addresses concerns around affordability, long‑term use and equitable access.

At the same time, technologies are changing how consumers access food and health related information, enabling more informed purchasing decisions in real time. Mobile apps that let consumers scan product barcodes and instantly generate health ratings and nutritional details are gaining increasing traction. Large retailers are rolling out platforms to track shopping habits and provide personalized feedback, nudging consumers toward healthier choices. Social media is also empowering a new generation of conscious consumers and accelerating the shift in demand, with brands partnering with influencers and celebrities and tailoring messaging to match audience aspirations.

Against this backdrop, policy momentum has moved from debate to design, with more structural responses than we have seen before. In the UK, the government announced a new Healthy Food Standard in June 2025 requiring large retailers/manufacturers to make the average shopping basket healthier, with mandatory sales reporting planned. Regulators are also moving to restrict advertising for high in fat, salt and sugar (HFSS) foods from January 2026. In the US, the Make America Healthy Again (MAHA) initiative under Health Secretary Robert F. Kennedy Jr. has put UPFs and obesity at the centre of federal action – politically polarising, but material for food and ingredient companies. Beyond rhetoric, the FDA has opened workstreams that directly affect the ingredients value chain, including reforms to the Generally Recognised as Safe (GRAS) framework, reviews of food chemicals (e.g., phthalates, titanium dioxide), and approvals for natural colours.

Taken together, this convergence – public health, economics, science, policy, consumer pressure, and the digital revolution – is pushing the food sector toward health & wellness-oriented formulations and greater ingredient transparency. For investors, the shift creates both a regulatory overhang for highly exposed portfolios and a market share opportunity for companies that reformulate, improve transparency, and realign propositions to new consumer habits.

Is this a perfect storm forcing businesses to change?

Therefore, the overarching question is: will the growing adoption of weight loss drugs, together with supportive government policy and shifting consumer narratives, create a “perfect storm” for the food and beverage industry?

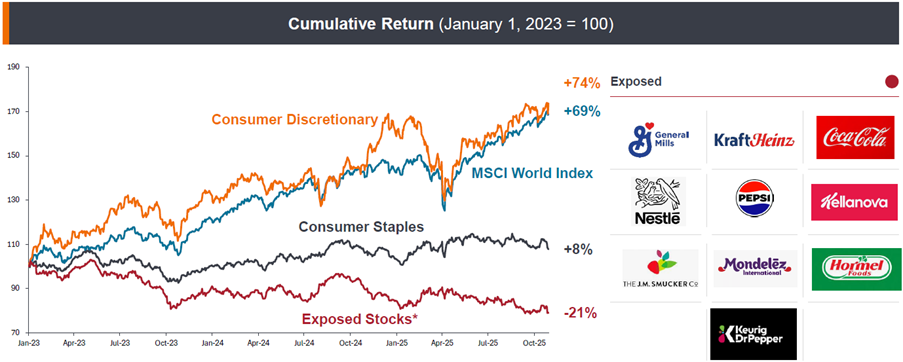

Although companies have been cautious about acknowledging any impact from changing consumer habits, snacking companies and junk food brands have come under pressure, with notable drops in share price and signs of softer demand. General Mills, Campbell’s Company, PepsiCo, and Mondelez have all reported slowdowns in snacking, alongside year-on-year sales declines and downward forecast revisions. Campbell’s CEO noted that consumers are cooking more at home and becoming “increasingly intentional about their discretionary snack purchases”. Similarly, PepsiCo highlighted a shift toward more ‘value conscious shopping behaviours – especially in the savoury snack category’. These observations are emblematic of a wider trend: legacy snack brands are losing relevance as consumers prioritize health, transparency, and nutrient density.

Exhibit 3: Financial materiality – stocks are reflecting these trends

Source: Bloomberg, Janus Henderson research as at December 2025. Past performance does not predict future returns.

Note: Exposed stocks represent an equally weighted basket of exposed companies within the consumer stables sector. References made to individual securities do not constitute a recommendation to buy, sell or hold any security, investment strategy or market sector, and should not be assumed to be profitable. Janus Henderson Investors, its affiliated advisor, or its employees, may have a position in the securities mentioned. Use of third-party names, marks or logos is purely for illustrative purposes and does not imply any association between any third-party and Janus Henderson Investors, nor any endorsement or recommendation by or of any third party. Unless stated otherwise, trademarks are the exclusive property of their respective owners.

Businesses are also gradually shifting tone and making strategic pivots – from downplaying these trends to embracing the new landscape as an opportunity. This is evident in merger and acquisition (M&A) activities, with companies acquiring healthier brands. For example, Coca-Cola acquired Fairlife, its fastest-growing US brand, while Danone purchased Kate Farms, expanding into plant-based medical nutrition, its fastest-growing segment. Other companies, including Ferrero, Hershey, Nestle, and Unilever, have also expanded their health, wellness, and nutrition portfolios by targeting candidates in the clean-label and better-for-you sectors.

Dialogue across the consumer landscape: reformulation, transparency, and private‑label innovation

Across our engagements with UK and EU supermarkets and ingredients players, a consistent theme is proactive, policy‑aware reformulation and cleaner labels. Retailers (e.g., M&S, Sainsbury’s, Tesco, Waitrose) are quietly reformulating in the background – removing preservatives from bread and taking nitrates out of meat – while also launching health‑led ranges (gut health, brain food, plant diversity) and clearer front‑of‑pack cues such as Sainsbury’s “Healthy Choice” and Waitrose’s “30 Plants a Week”, with Tesco developing “Gut Sense.”

This is partly driven by regulatory scrutiny and a desire not to be caught on the back foot if rules evolve, and partly by changing consumer behaviour: companies tell us shoppers want more transparency about what’s in their food, and we are seeing investment in technologies (QR codes, better nutritional labelling) to improve ingredient traceability.

The cleaner‑label trend is accelerating. With ~65% of preservatives still synthetic7, ingredients specialists such as Novonesis – and broader biosolutions providers of cultures, enzymes, and probiotics – see a clear opportunity to substitute toward more natural alternatives.

Supermarkets have been at the forefront of monitoring and shaping these shifts, adapting assortments quickly to meet demand – including convenient, nutritious ready meals and food‑to‑go options that are winning share from eating out, particularly among Gen Z and hybrid workers.

At the same time, we are seeing significant private‑label innovation: new own‑brand ranges, formats that help consumers cook from scratch, and deeper collaboration with suppliers on reformulation – all of which support shorter, more transparent ingredient lists and health‑aligned claims.

Collectively, this retail‑ingredients dialogue is translating into strong momentum in health‑oriented lines (e.g., protein snacks and sports nutrition) and more resilient, agile product offerings that can pivot as consumer preferences and policy landscapes evolve.

Transforming the food landscape: a path forward

As the obesity crisis reaches unprecedented levels, the intersection of public health initiatives, consumer demand, and corporate strategy is reshaping the food landscape. The adoption of GLP-1 weight loss drugs and increased awareness of ultra-processed foods signal a pivotal moment for the industry.

For investors, this suggests a greater focus on product mix resilience, R&D velocity, and supplier collaboration. Companies that embrace transparency, reformulate products, and pivot towards health-focused offerings may gain market share and consumer trust. This evolving dynamic presents both challenges and opportunities, driving a collective movement among governments, industries, and consumers toward a healthier and more sustainable future.

In seeking to drive returns for our clients, it’s critical that we understand this intersection of evolving consumer preference, obesity & health economics, ultra processed food exposure, GLP-1 adoption, and accelerating policy pressure. This is a core part of the fundamental analytical effort as we seek to generate alpha. These forces are reshaping demand, product mix, regulation, and cost structures across consumer staples and discretionary sectors, creating clear winners and losers. Investors that fail to identify which companies can reformulate, adapt portfolios, and align with health-conscious consumption will risk being exposed to structural earnings erosion and sustained underperformance versus the benchmark, while those positioned on the right side of these shifts can capture durable relative returns.

– Research Analyst Gregory Kuczynski

1Okunogbe A, Nugent R, Spencer G, et al. Economic impacts of overweight and obesity: current and future estimates for eight countries. BMJ Global Health 2021;6:e006351. doi:10.1136/ bmjgh-2021-006351.

2The Economy, ‘The Global Obesity Epidemic: A Growing Crisis with Economic and Health Implications’, 18 March 2025.

3Biology Insights, ‘The Global Obesity Crisis: Causes, Impacts, and Solutions’, 27 July 2025.

4Centers for Disease Control and Prevention (CDC)

5UK Government, Office for Life Sciences, ‘Obesity Healthcare Goals’, 16 December 2025.

6Regulating the Food Industry: An Aspirational Agenda’, American Journal of Public Health 112, 853_858, https://doi.org/10.2105/AJPH.2022.306844.

7Chauhan, Kanika et al., Heliyon, Volume 10, Issue 16, e35815.

Clean labelling: A movement towards using fewer artificial additives in food products, focusing on simple, recognizable ingredients to meet consumer demand for transparency and healthfulness.

Chronic diseases: Long-term medical conditions, such as type 2 diabetes, cardiovascular diseases, and cancer, often exacerbated by obesity and poor dietary habits.

Financial materiality: The significance of financial impacts on a company due to external factors, such as changes in consumer preferences or regulatory shifts.

Food and Drug Administration (FDA): A US federal agency responsible for protecting public health by ensuring the safety and efficacy of food, drugs, and other consumer products.

GLP-1 Weight Loss Drugs: Medications, such as Wegovy, Ozempic, and Mounjaro, that mimic the glucagon-like peptide-1 hormone to aid in weight loss by regulating appetite and blood sugar levels.

Healthy Food Standard: A proposed regulation requiring food retailers and manufacturers to improve the nutritional quality of their offerings, often through reformulation and better labelling.

Ingredient transparency: The practice of clearly disclosing all components used in a product, aimed at providing consumers with comprehensive information about what they are consuming.

Ingredient transparency: The practice of clearly disclosing all components used in a product, aimed at providing consumers with comprehensive information about what they are consuming.

Obesity crisis: A global health issue characterized by an increasing prevalence of overweight and obesity, leading to serious health complications and economic burdens.

Ultra-Processed Foods (UPFs): Foods that have been significantly altered from their original form through the addition of substances like sugars, fats, preservatives, and artificial additives to enhance flavour and shelf life.