Chart to Watch: Insatiable demand for compute power rationalises massive capex

Rising AI use cases, token volumes and compute efficiency gains married with falling compute costs are underpinning robust AI demand, driving tech giants to invest at an unprecedented scale. This is reshaping the competitive landscape for AI infrastructure and monetisation, says Portfolio Manager Richard Clode.

We are moving to a world where progress and productivity will be measured in tokens. – Richard Clode

Key takeaways

- AI token demand is growing exponentially, driven by increasingly complex and agentic use cases, even as models become more efficient per task.

- Falling compute costs are increasing overall demand, justifying unprecedented levels of tech giants AI capex.

- Monetising tokens at scale is central to AI return-on-investment, making the ability to price, distribute, and capture usage a key competitive differentiator.

The scale of investment flowing into artificial intelligence reflects a simple reality: demand for compute is accelerating faster than efficiency gains can match. AI usage is growing exponentially even as the cost of computation per task falls – a classic case of Jevons’ Paradox, where falling costs make a resource more attractive, leading to higher demand.

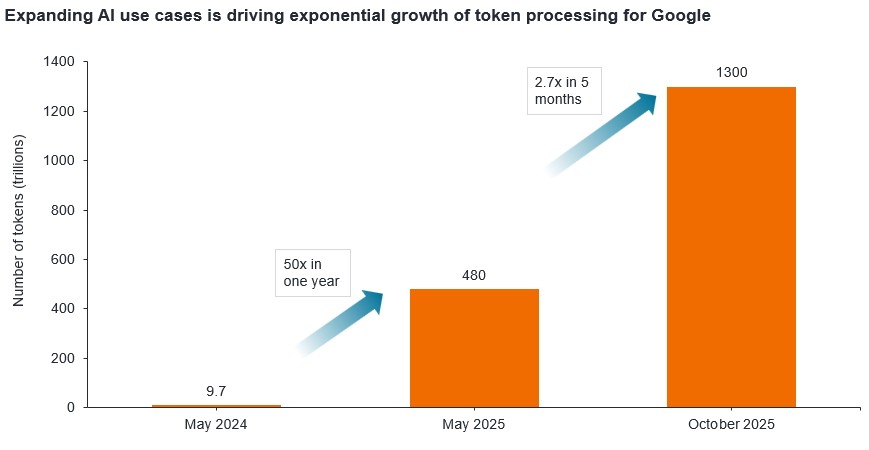

Google’s token growth highlights the scale of AI demand

Tokens are the basic units AI models process when reading, generating, or reasoning with information. More complex and agentic AI use cases, such as autonomous research assistants, coding agents, and multimodal enterprise workflows, dramatically increase token volumes. Google has been the leader in tokens processing; monthly tokens processed jumped from 9.7 trillion in May 2024 to 480 trillion 12 months later. By October 2025 this surged dramatically to 1,300 trillion tokens (most recent data).1

Efficiency improvements remain rapid. Models such as Gemini 3 Flash use fewer tokens per task and significantly less compute, yet total demand continues to rise as AI becomes embedded across productivity, search, and decision‑making workflows.

Token monetisation can assuage AI capex concerns

Meeting insatiable AI demand requires unprecedented capital expenditure (capex). Google has signalled 2026 capex of up to US$185 billion, double that of last 2025,2 Amazon is projecting capex of US$200 billion,3 while Meta is estimating up to US$135 billion.4 NVIDIA suggests that tiered token monetisation can ultimately translate this surge in usage into durable returns, helping to justify the scale of investment.

We believe that the magnitude and duration of AI spend is still underappreciated. Coupled with a rapidly-expanding addressable market for AI, with tech sector valuations now at a five-year low to broader equities,5 active stock pickers like us have ample opportunities to identify future leaders with earnings power that is not yet fully appreciated.

1 Google blog; Q3 earnings call: Remarks from our CEO; 29 October 2025.

2 Alphabet 4Q and fiscal year 2025 results; 4 February 2026.

3 Amazon Q4 2025 results; 5 February 2026.

4 Meta Q4 2025 earnings call; 28 January 2026.

5 Bernstein data as at end February 2026. Tech sector price-to forward earnings (P/E ratio) of circa 22% versus broader equities 5-year average of 36%. Based on MSCI ACWI Information Technology Sector, price-to-forward earnings relative to MSCI ACWI Index from December 1999 to November 2018 pre GICS sector changes in MSCI Global indices, and MSCI ACWI Information Technology + ACWI Communication Services relative to MSCI ACWI Index to current post GICS sector changes in MSCI Global indices. Past performance does not predict future returns.

Agentic AI: Refers to autonomous, goal-driven AI systems that can plan, reason, and take actions to achieve complex objectives with limited human oversight, rather than just generating text or responding to prompts.

Capital expenditure: Money invested to acquire or upgrade fixed assets such as buildings, machinery, equipment, or vehicles in order to maintain or improve operations and foster future growth.

Jevon’s Paradox: A theory suggesting that greater efficiency in the use of any given resource can result in increased demand for that resource. Applying this to technology/AI chips, as technological and efficiency improvements in technology/chips increases, the overall demand for chips actually increases rather than decreases.

Price-to-earnings ratio (P/E): A popular valuation metric that measures share price compared to earnings per share for a stock or stocks in a portfolio.

These are the views of the author at the time of publication and may differ from the views of other individuals/teams at Janus Henderson Investors. References made to individual securities do not constitute a recommendation to buy, sell or hold any security, investment strategy or market sector, and should not be assumed to be profitable. Janus Henderson Investors, its affiliated advisor, or its employees, may have a position in the securities mentioned.

Past performance does not predict future returns. The value of an investment and the income from it can fall as well as rise and you may not get back the amount originally invested.

The information in this article does not qualify as an investment recommendation.

There is no guarantee that past trends will continue, or forecasts will be realised.

Marketing Communication.

Important information

Please read the following important information regarding funds related to this article.

- Shares/Units can lose value rapidly, and typically involve higher risks than bonds or money market instruments. The value of your investment may fall as a result.

- If a Fund has a high exposure to a particular country or geographical region it carries a higher level of risk than a Fund which is more broadly diversified.

- The Fund is focused towards particular industries or investment themes and may be heavily impacted by factors such as changes in government regulation, increased price competition, technological advancements and other adverse events.

- This Fund may have a particularly concentrated portfolio relative to its investment universe or other funds in its sector. An adverse event impacting even a small number of holdings could create significant volatility or losses for the Fund.

- The Fund may use derivatives with the aim of reducing risk or managing the portfolio more efficiently. However this introduces other risks, in particular, that a derivative counterparty may not meet its contractual obligations.

- If the Fund holds assets in currencies other than the base currency of the Fund, or you invest in a share/unit class of a different currency to the Fund (unless hedged, i.e. mitigated by taking an offsetting position in a related security), the value of your investment may be impacted by changes in exchange rates.

- Securities within the Fund could become hard to value or to sell at a desired time and price, especially in extreme market conditions when asset prices may be falling, increasing the risk of investment losses.

- The Fund could lose money if a counterparty with which the Fund trades becomes unwilling or unable to meet its obligations, or as a result of failure or delay in operational processes or the failure of a third party provider.