Key takeaways:

- Diminished global geopolitical risks lowered yields, while broad markets monitor AI developments.

- The RBA remain vigilant on sticky core inflation, with Trimmed Mean at 3.6%yoy being too high.

- We see the peak in the RBA cash rate at 4.60% later this year before easing H2 2027.

- Economic Focus: Budget season

Market review

The Reserve Bank of Australia (RBA) kept interest rates on hold at 4.35%, in an anticipated pause. The three‑month Bank Bill Swap Rates (BBSW) rose 1 basis point (bp) to 4.46%, while six‑month BBSW fell 2bps to 4.80%. Government bond yields moved lower across the curve as market’s focussed on the downside of the cycle in coming years. The three‑year Commonwealth bond yield fell 11bps to 4.36%, while the 10‑year yield declined 11bps to 4.72%. Market‑based inflation expectations eased, with 10‑year inflation‑linked yields falling 10bps to 2.28%.

The RBA have been the G10 leader in this upcycle, responding to inflation embedded in place prior to the oil shock. Other central banks have followed. The US Federal Reserve (Fed) has been a laggard, despite the strength in the US economy. Markets are now re-pricing the Fed outlook, along with the commencement of its new Chair, Warsh. Global inflation is sticky, and while oil prices are allowing headline rates to moderate, core levels remain high. Locally, trimmed mean inflation was higher than expected in May, at 3.6%yoy and the RBA remain focussed on these risks.

Locally, GDP remained at 2.5%yoy, driven by continued artificial intelligence (AI) related capital investment. We expect this investment cycle continues, despite its import heavy nature, to propel domestic demand and maintain an overall positive growth momentum. The household sector may be subdued, with moderating house prices and declining real wages, but current levels of spending have remained resilient. The labour market also remains solid, with unemployment at 4.4%.

Market outlook

We continue to see one last RBA hike, to 4.60% Our high case is one where inflation remains elevated and the RBA are forced to raise interest rates more than expected into 2027. Our low case reflects a weaker economic outcome, particularly if supply constraints and rising costs act as a tax to subdue growth. We hold no tilt at present, viewing the risk profile as broadly distributed. We hold a small, long duration position and continue to take advantage of opportunities in volatile markets.

Monthly focus – Budget season

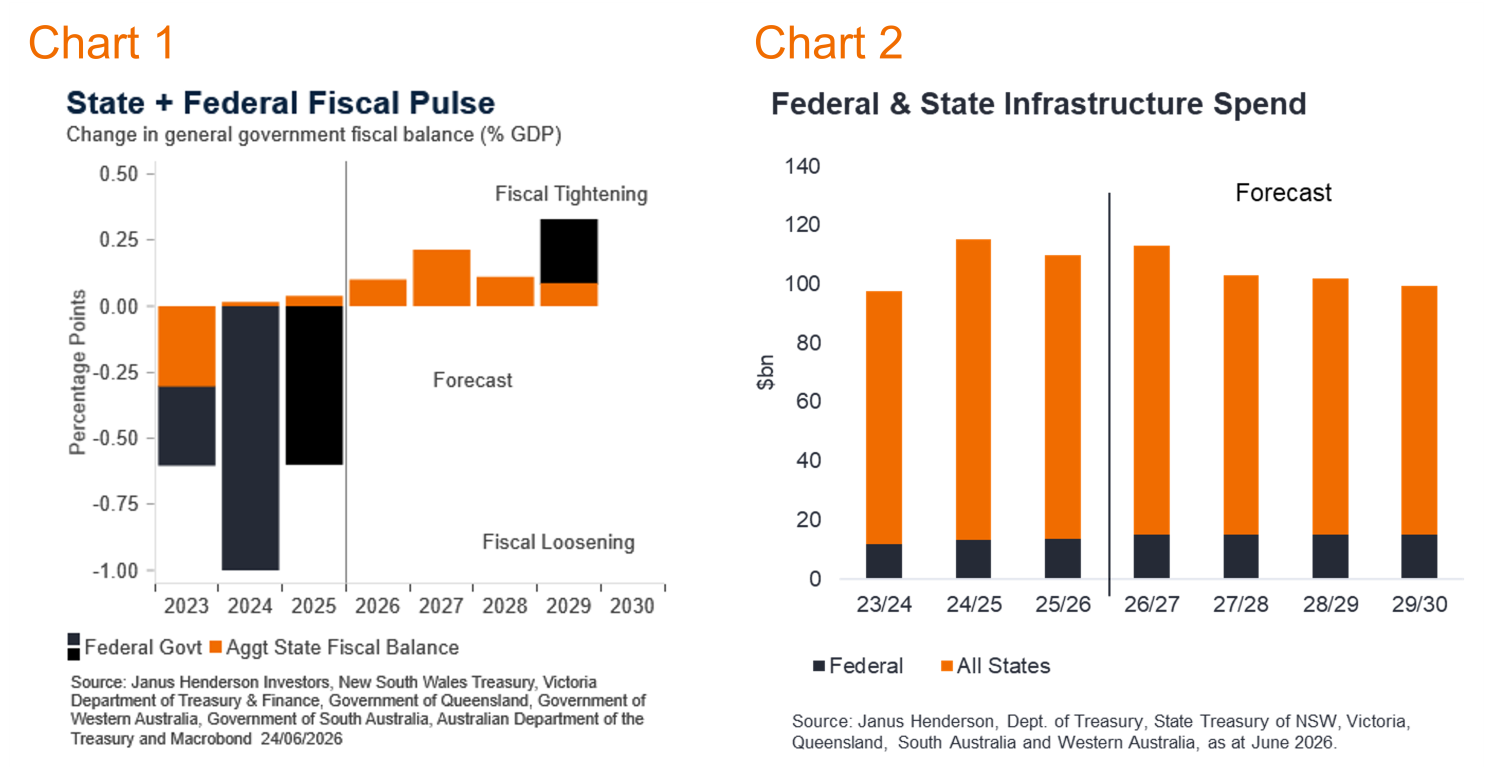

Australia’s budget season has concluded, bringing with it fundamental tax changes and robust debate. Stepping out of the weeds of individual policies, we examine the top-down fiscal influence on the economy as forecast by the Federal, and State, Governments. Amid the significant policy changes, the aggregate influences on the fiscal pulse, and capital expenditure, are relatively mild. This feeds into our outlook for the Australian economy, where the AI supercycle takes over from Government led demand.

We split the macroeconomic impact between the fiscal pulse, or the change in the headline cash balance for the general government as a percentage of GDP, and infrastructure spending plans. The first being more cyclical and expenditure based, while the second is structural and investment in nature.

The Federal Government fiscal pulse is relatively neutral, despite the changes to the health and tax policies. The significant policy changes are only anticipated to have aggregate fiscal impacts in the out years, leaving the near-term forecast fiscal pulse near zero. This comes after three years of fiscal loosening, supporting broad economic growth.

State Governments continue to pare back spending from the pandemic years, particularly Victoria, attempting to return to surpluses, and stabilise debt levels. To mixed success. For the 2026/27 fiscal year, New South Wales and Queensland expect continued general government cash deficits, but the other States report improving surpluses. Compared to their mid-year updates, the tightening pulse was a little less than forecast, but an aggregate tightening pulse nonetheless. This leaves Government consumption contribution to GDP lower than in prior years. Combined with the subdued consumer, the overall consumption contributions are expected to be particularly subdued in the coming year.

This leaves the investment side of the economy doing the economic growth heavy lifting. We have previously discussed our strong AI supercycle capital expenditure outlook, which steps into the modest decline in Government infrastructure spending. The fiscal updates suggest that there will be a little more government infrastructure spending in the 2026/27 fiscal year than previously planned, before a decline, at still high levels. Federal Government plans are relatively steady across the forward years. Within the States, Victoria’s significant infrastructure program continues to wind down, New South Wales remains strong with small moderations, while Queensland ramps up further into the out years, amid the looming Olympics. These plans imply a modest positive contribution from Government capital expenditure this year, to add to the strong private plans. In the following years, Government investment starts to detract from aggregate growth.

In the washup of the proposed plans, net government debt is forecast to rise over the forward estimates. Federal Government net debt is forecast to be 22% of GDP in 2030, below the pandemic peaks but historically elevated. State net debt is also expected to rise over the forward years and nearly doubles the aggregate General Government net debt as a percent of GDP. However, in a global context, the International Monetary Fund show that the combined General Government net debt is at the lower end of G10 economy levels and debt remains relatively well contained compared to our peers. This is why Australia is one of the few G10 sovereigns to have retained its AAA debt rating. Would we wish for debt repair? Certainly. But can Australia manage the levels we have and continue to be an attractive sovereign investment environment? Definitely. This year’s budget season did not change that view.

Views as at 1 July 2026.

All opinions and estimates in this information are subject to change without notice and are the views of the author at the time of publication. Janus Henderson is not under any obligation to update this information to the extent that it is or becomes out of date or incorrect. The information herein shall not in any way constitute advice or an invitation to invest. It is solely for information purposes and subject to change without notice. This information does not purport to be a comprehensive statement or description of any markets or securities referred to within. Any references to individual securities do not constitute a securities recommendation. Past performance is not indicative of future performance. The value of an investment and the income from it can fall as well as rise and you may not get back the amount originally invested.

Whilst Janus Henderson believe that the information is correct at the date of publication, no warranty or representation is given to this effect and no responsibility can be accepted by Janus Henderson to any end users for any action taken on the basis of this information.