Key takeaways:

- The conference struck a constructive but cautious tone for securitised markets. Demand remains firm and collateral performance broadly supportive, but higher-for-longer rates, inflation pressure, geopolitical uncertainty and tighter valuations are raising the onus on discipline.

- As valuations tighten, dispersion matters more. Opportunities remain in Australian residential mortgage-backed securities (RMBS), data-centre finance and improving CLO platforms, but outcomes will depend increasingly on issuer quality, collateral resilience, underwriting discipline and careful bottom-up selection.

- We use issuer and CLO manager engagement to aid underwriting, prioritising asset quality, sponsor strength, portfolio composition, CLO manager alignment, risk-management discipline and resilience under stressed market conditions, rather than simply reaching for yield.

Cautious but constructive

Arriving in sunny Barcelona in June, the Global asset-backed securities (ABS) conference had a palpable energy, drawing thousands of participants from across the globe to take the pulse of the securitisation market. But the mood did not quite match the brightness of the setting – cautious, yet still constructive, as investors continued their search for opportunity in a world of tighter fixed income valuations.

ABS resilience ran like a steady thread through the discussions, with demand firm, issuance strong and collateral performance broadly supportive. Nevertheless, geopolitical uncertainty, higher-for-longer rates, inflation pressure and the risk of a consumer slowdown cast a shadow over sentiment, underscoring the need for discipline rather than a simple search for yield.

Regulation around securitisation was seen as edging in the right direction, particularly around securitisation reform and potential insurance demand from Solvency II capital charge changes, but few expected it to deepen the market materially in the near term.

Private credit was perceived to be on an upward growth path, particularly asset-based finance, but recent headlines have brought sharper focus to underwriting discipline, transparency and asset-level verification. Concerns around double-pledging prompted discussion of audits and even blockchain-based registration of claims as potential safeguards against the practice. One investor noted that double-pledging was not evident in public securities[1].

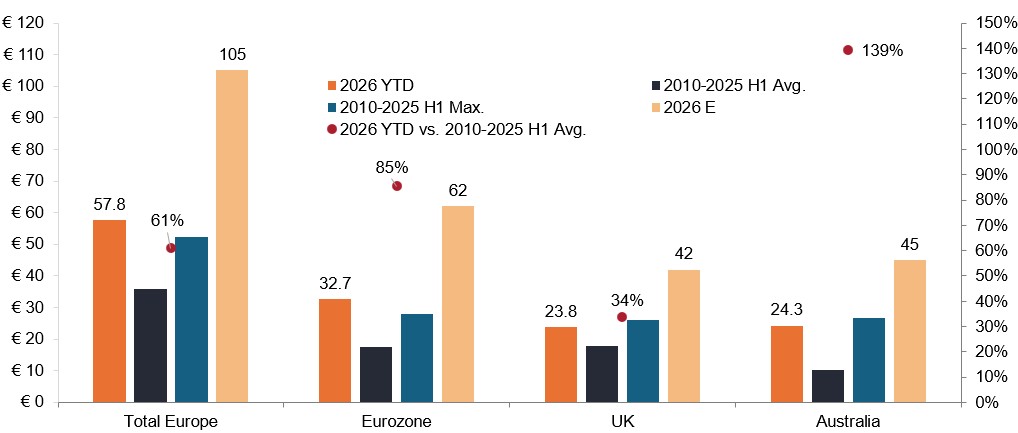

The opportunity set for European securitised investors is expanding, as seen by a post-crisis record expected in supply this year. As shown below, €105bn of distributed European ABS issuance is expected in 2026 and €45bn of supply in Australia (Figure 1).

Figure 1: A post-crisis record in issuance is expected in 2026

Source: JP Morgan, as at 8 June 2026. There is no guarantee that past trends will continue, or forecasts will be realised.

Against the more intricate backdrop, the conference’s sector discussions helped illuminate where investors are still finding opportunities: the revival of European Commercial Mortgage Backed Securities (CMBS) and proliferation of data centre finance, the dispersion in collateralised loan obligations (CLOs), and the diversification appeal of Australian ABS. Here, we delve deeper into these through wider discussions and issuer engagement, which helps to enlighten our fundamental research.

A deep dive down under in Australia

In Australia, our conversations spanned the breadth of the securitisation market, bringing together primary issuer insight and secondary trading perspectives across the capital structure. This included non‑bank issuers across RMBS, auto, SME/asset finance and consumer ABS, alongside major trading desks, shedding light on liquidity, flows and investor demand.

Our base case is for Australian securitised credit performance to soften from very strong levels, although this is not yet evident in realised data. Issuers attributed expected deterioration to the cumulative impact of rate rises, inflationary pressure and slower housing turnover, even as arrears and losses remain stable and, in some recent vintages, are improving.

Easing fuel concerns

At the same time, issuer-level engagement provided reassurance on a number of key concerns. In particular, exposure to diesel‑intensive segments – a potential vulnerability within commercial and SME lending – appears more manageable than initially feared.

Originators highlighted several mitigating factors. Borrowers in these segments retain some ability to pass through higher fuel costs, while fuel supply dynamics are supported by international flows (from the US via Singapore) and available reserves. In addition, one issuer noted continued strength in secondary market values for light commercial vehicle collateral, supporting recovery assumptions.

More broadly, issuers reported no observable deterioration in performance from diesel‑exposed sectors to date. Instead, they emphasised the importance of portfolio asset mix, with a shift away from diesel, noting that exposures are typically granular and not uniformly sensitive to fuel‑cost pressures.

Pockets of value

Finally, despite strong performance, we observe pockets of attractive value. Senior RMBS appears relatively cheap, with scope for spread tightening, in our view, as technicals remain supportive and credit fundamentals hold. Trading desk feedback highlighted strong liquidity in senior tranches, alongside improving but still more limited depth in mezzanine, suggesting valuation dispersion across the capital structure may present selective opportunities.

CMBS and data centres: an evolving opportunity

Securitised markets are broadening, both in terms of issuance and underlying collateral. In CMBS, conversations pointed to a revived supply backdrop, with expectations for increased issuance and a wider mix of collateral types across Europe. While sponsor concentration remains a focus, the market is beginning to diversify, which we see as important for market depth and liquidity.

Data centres – which can be structured as CMBS or ABS – increasingly merit treatment as a distinct asset class, where an investment grade profile at better spreads than comparable corporate credit can be found. Across meetings, we observed consistent institutionalisation of the sector, with issuers focused on hyperscale,[1] investment-grade tenants, long-dated leases (10-15 years) alongside pre-leasing and built‑to‑suit assets, helping to reinforce the stability of contracted cash flows. Such contract structures pass through a significant portion of operating costs to tenants. Stability in the face of a rapidly-evolving theme such as AI is an appealing way to access this structural trend.

Discussions consistently highlighted strong demand dynamics, particularly from public cloud providers, alongside emerging AI use cases. This demand backdrop is driving expansion across Europe, although constraints around power availability, labour, and regulatory frameworks remain.

Overall, we see a market in early-stage growth: issuance is increasing, structures are evolving, and investor opportunity is widening. Meetings with multiple issuers helped us deploy useful early-stage benchmarking across operators, highlighting the importance of underwriting discipline. After all, we believe data centres exhibit highly idiosyncratic risk, with outcomes dependent on tenant quality, power availability, location, and asset design. Both CMBS and data centres require a highly selective, bottom-up approach, where identifying asset quality and sponsor strength remains critical.

CLO: dispersion brings opportunity

We came away from Barcelona with a consistent message: the market backdrop feels increasingly late-cycle. Technicals remain supportive, but abundant capital is competing for limited loan supply, keeping valuations tight. At the same time, caution is building for corporates in general. Higher-for-longer rates are tightening financial conditions, and several conversations pointed to the risk that an eventual correction in credit more broadly could potentially be triggered by AI‑driven dislocation.

Against this environment, CLO manager dispersion is becoming more pronounced. We observed a divide between those adopting proactive, trading-oriented risk management – dynamically trimming exposure and reallocating risk – and those maintaining a more static, conviction-led approach, holding through volatility if fundamentals remain intact. This distinction is likely to be a key driver of outcomes in a downturn.

We met with several managers who do not currently form part of our investible universe to assess whether they should be included. Our screening framework focuses on several core parameters:

- Platform strength and alignment, including capital backing, stability of the franchise and equity participation

- Depth and experience of the investment team, alongside evidence of continuity and decision-making discipline

- Robustness of underwriting, including the use of systematic scoring, relative value frameworks and ongoing monitoring

- Portfolio construction and risk management, particularly the approach to tail risk, trading flexibility and drawdown control

- Operational infrastructure and data capability, including the integration of technology and analytical tools

- ESG integration, both in underwriting and portfolio-level implementation

On this basis, we see selective opportunities emerging among improving CLO managers offering compelling spreads with credible structures. However, we remain patient where track records are still developing, and cautious on strategies where a more static approach to tail risk could lead to greater drawdowns in stressed environments given our conservative bias.

Footnotes

[1] Source: Bank of America Global Research, 15 June 2026.

[2] Large, single‑tenant (or highly concentrated) assets